Author: Zach Pandl, Grayscale Research Director

Translation: Deep Tide TechFlow

Deep Tide Overview: Grayscale Research Director Zach Pandl pointed out that Ethereum's current staking reward model faces two structural issues: L2 diversion leads to a decrease in token destruction and an increase in net issuance; the staking threshold approaches zero, potentially locking almost all ETH into staking. The community is discussing setting a limit curve for staking rewards, and Grayscale believes this is beneficial for ETH prices in the long term.

The Ethereum community is considering modifying the network's staking reward model, with the core idea being to only incentivize staking up to a certain ratio, and beyond that, no additional rewards will be given. If implemented, the nominal returns for stakers would decrease. However, Grayscale believes this is a good thing for ETH prices in the long term for two reasons: one is to control ETH inflation, and the other is to strengthen the narrative of ETH as a store of value asset.

This reform discussion is driven by two overlapping issues.

Weakened token destruction, rising net issuance

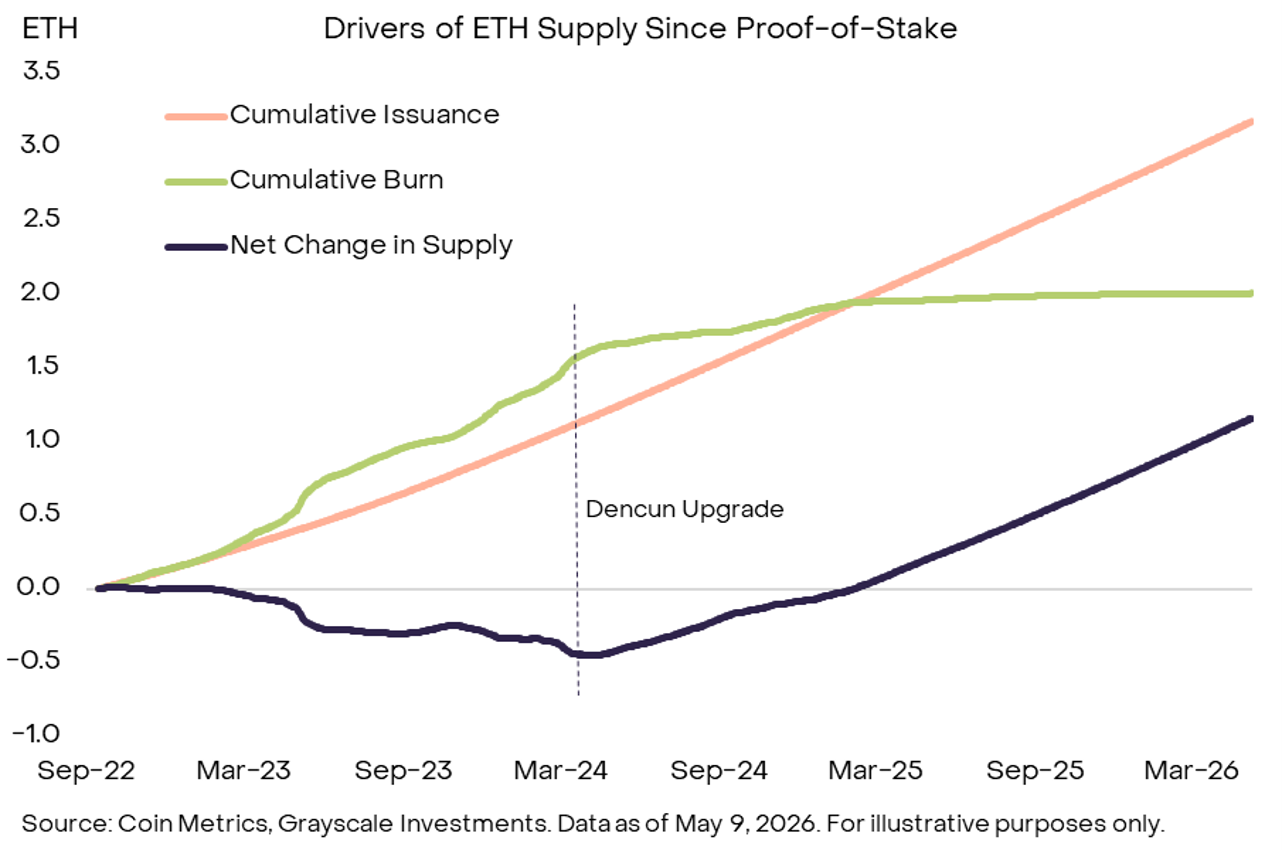

The supply of ETH is determined by the difference between new issuance and token destruction. Currently, Ethereum L1 destroys all base transaction fees, and higher fees mean more ETH is burned, suppressing supply growth.

Changes over the past few years have disrupted this balance. An increasing amount of activity has migrated to L2 networks, leading to a decline in L1 transaction fees and token destruction, while net issuance has begun to rise.

Figure Caption: Exhibit 1 - Drivers of ETH supply changes since PoS. Following the Dencun upgrade, the cumulative destruction amount (green line) has flattened, while the cumulative issuance amount (orange line) continues to rise, leading to a shift in ETH net supply change (dark line) from negative to positive. Source: Coin Metrics, Grayscale Investments, data as of May 9, 2026

Compounding the issue, Ethereum L1 is now actively choosing to expand capacity to combat competition from high-throughput chains like Solana. Pandl bluntly stated that L1 transaction fees are likely to remain low for the foreseeable future, token destruction will continue to decline, and net supply growth will further expand.

The friction cost of staking is almost zero

When staking was first introduced on Ethereum, users could not withdraw assets, and staked ETH was locked, resulting in poor liquidity and a risk premium. Now that withdrawals have opened, liquidity has significantly improved, and the risk premium has evaporated.

More critically, liquid staking tokens (LSTs), exchange-traded products (ETPs), and corporate ETH treasuries have also joined the staking ranks. The marginal cost of staking ETH is now close to zero. As long as the network continues to provide marginal returns to stakers, almost all ETH could eventually be staked.

Staking is a necessary condition for the normal operation of the Ethereum protocol, but an excessively high staking ratio may be counterproductive.

There are two risks. First, unnecessary dilution. An increase in net issuance without a substantial enhancement in network security is like a country overspending on national defense without helping national security. Second, the concentration of staking activities led by a few institutions poses a centralized tail risk. This possibility exists due to the network effects of service providers.

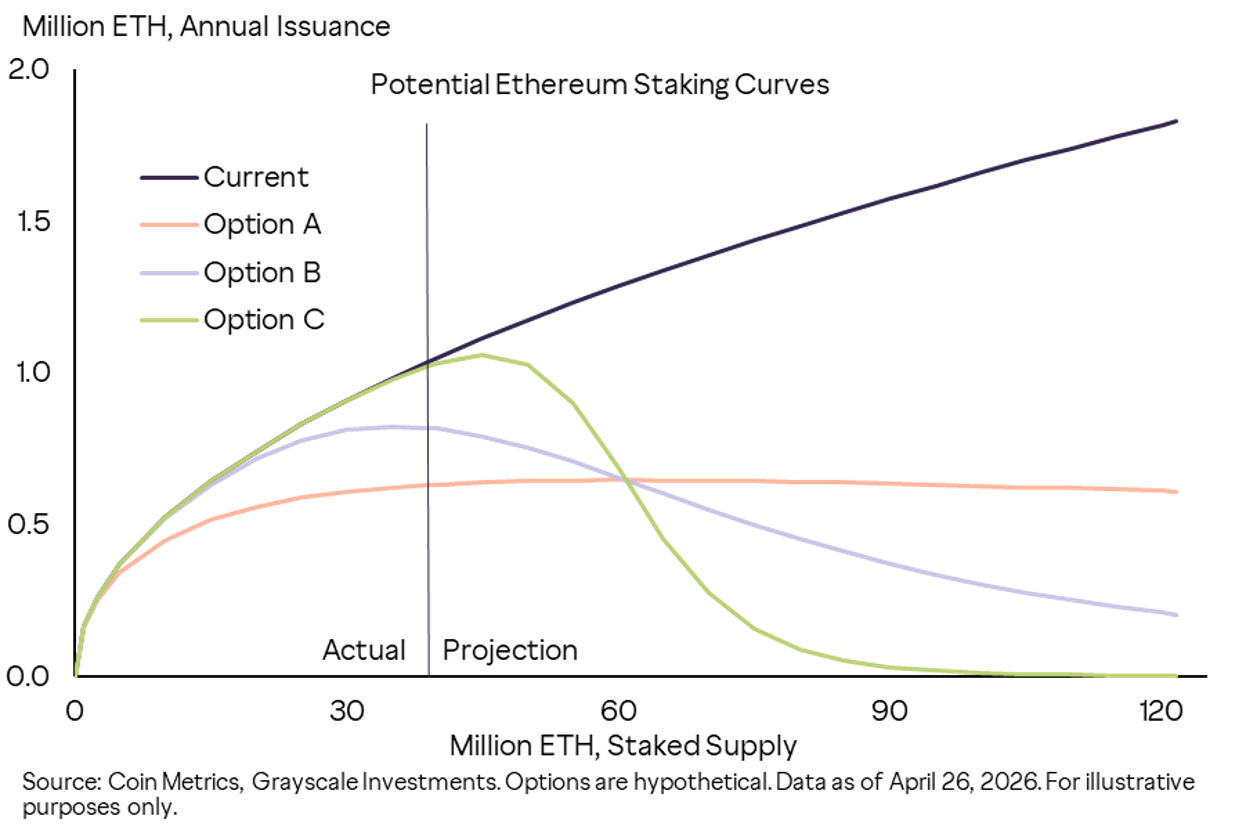

Setting a limit curve for staking rewards

One solution is to shift to a reward model that only incentivizes staking to a certain level.

Figure Caption: Exhibit 2 - Alternative staking reward curves that Ethereum might consider. In the current model (dark line), annual issuance grows linearly with the staking amount; Options A/B/C set caps or inflection points at different staking levels, flattening or even decreasing issuance once staking ratios exceed certain thresholds. Source: Coin Metrics, Grayscale Investments, data as of April 26, 2026, options are hypothetical scenarios

Grayscale believes this change would be beneficial for the long-term market value of ETH. ETH is a commodity with functional use, not a financial claim like stocks and bonds, and should not be priced solely based on cash flow. Updating the staking reward model would reduce supply growth and enhance the scarcity of ETH. For commodities, production cuts are favorable for prices, and the logic for ETH is the same.

Lowering network tail risks and controlling long-term inflation could also enhance the demand for unstaked ETH as a digital value storage asset.

Another perspective that is easily overlooked: the impact of ETH price fluctuations on investment returns far outweighs staking yields. The current annualized staking yield of approximately 3% is roughly equivalent to the price volatility of ETH in a day (with a past 360-day annualized volatility of about 60%, translating to a daily volatility of about 3%).

Conclusion: Ethereum may modify its staking reward model to control long-term supply growth and reduce certain tail risks. If implemented, Grayscale believes this would be a positive development for ETH prices.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。