Author: Bryan Vong, Foresight Ventures

Between September 2025 and March 2026, every major player in the global payment field made significant moves. OpenAI and Stripe jointly released the Agentic Commerce Protocol (ACP). Google launched the Universal Commerce Protocol (UCP). Within a week, Visa and Mastercard respectively released their Agent payment frameworks. In the following two months, the Coinbase x402 protocol processed over 15 million transactions on the Base chain. In March 2026, Stripe and Tempo jointly released the Machine Payments Protocol (MPP).

The intense actions of these technology giants and financial institutions are no coincidence, but rather a collective response from the payment industry to the same challenge: when AI agents become the most active consumers on the internet, the existing payment infrastructure can fundamentally no longer meet their operational needs.

Every design in traditional payment systems is based on the premise of "human operation": relying on browser interfaces, manually filling out forms, clicking "confirm payment", and verifying identities through verification codes. The operational logic of Agents is entirely different: they require machine-readable standard interfaces, millisecond-level authorization responses, and infrastructure adapted for high-frequency micro-settlements.

This infrastructure battle will not be dominated by a single protocol; rather, it is forming a clear dual-layer architecture. The intention layer defines "who is the merchant and how to facilitate transactions," while the settlement layer defines "how funds actually flow." The two layers are independent of each other and evolve separately, but both are indispensable. The absence of either layer means that the commercial closed loop of the Agent economy cannot be realized.

Part One: Intention Orchestration Layer

The intention orchestration layer is responsible for transforming the trading intentions of the Agent into executable full processes: discovering products or services, adding them to the cart, and triggering payment. This layer has currently formed two distinctly different tracks.

1.1 Agent Shopping for Humans

The core contradiction of this track is not payment, but access. Traditional e-commerce platforms are designed for human users, and Agents are unable to parse visual pages or click interactive elements. To enable Agents to complete purchases on behalf of humans, merchants must provide machine-readable standardized interfaces.

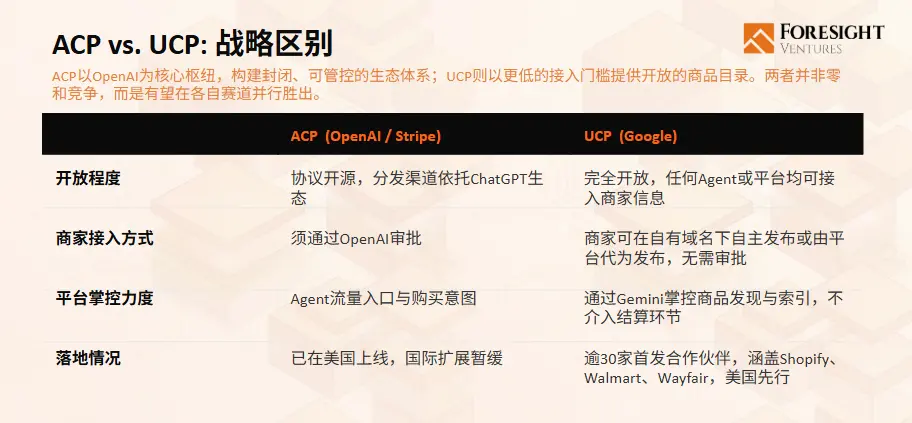

ACP (Agentic Commerce Protocol): AI Shopping Experience in a Closed Ecosystem

ACP was jointly released by OpenAI and Stripe in September 2025. Its core mechanism is delegated payment: when users confirm a purchase, they grant payment authority to the Agent, which completes the transaction through a payment credential that complies with the Delegated Payment Spec, while the merchant retains Merchant of Record status. Currently, Stripe's SPT is the first and only implementation of this system.

ChatGPT Instant Checkout was launched in September 2025 but was shut down in March 2026 due to a low conversion rate. OpenAI has shifted its strategic focus to product discovery, meaning after displaying products, ChatGPT redirects users to the merchant's native site to complete the transaction. The ACP protocol itself remains in a streamlined form, supporting exclusive ChatGPT applications for several large retailers, which must apply for access, with OpenAI controlling the display.

UCP (Universal Commerce Protocol): Long-Term Strategy for Open Standards

UCP was personally announced by Google CEO Sundar Pichai at the NRF Retail Industry Annual Conference in January 2026, having gained over 30 partners including mainstream platforms such as Shopify, Stripe, Visa, Mastercard, Walmart, and Wayfair. The core mechanism of UCP is the merchant capability declaration: merchants publish a UCP configuration file in JSON format under their own domain, declaring their supported transfer and payment capabilities, which AI can directly read. Through this, Google aims to make Gemini the core discovery layer for Agent shopping.

The core difference lies in Google's deliberate avoidance of the role of intermediary. It does not need to own the transaction itself but needs to control the upstream aspect of product discovery. ACP and UCP are not in competition but represent two different market propositions: the former exchanges a closed ecosystem for an extreme user experience and control, while the latter exchanges open standards for greater scalability and interoperability.

1.2 Transactions Between Agents

If track A addresses how Agents can complete shopping for humans, track B seeks to address a more fundamental issue: when both parties in a transaction are Agents and no human merchant is involved, where does trust come from? There is a lack of credibility endorsement between Agents, and consumer protection regulations are inapplicable. The core contradiction lies in how to ensure the reliability of value exchange in a zero-trust environment.

ERC-8183 + ERC-8004: Onchain Trustless Task Contracts

ERC-8183 was jointly launched by the Ethereum Foundation's dAI team and Virtuals Protocol in March 2026. Each job consists of three parties: Client (the delegator), Provider (the service provider), and Evaluator (the evaluator), with funds held in a smart contract until task acceptance is completed. Transaction parties do not need mutual trust, only trust in the contract itself. ERC-8004 is a supporting identity protocol, where each Agent accumulates a reputation score based on historical transactions after registration onchain. Currently, approximately 24,000 Agents have been registered across the network.

Virtuals Protocol's Butler is the largest promoter of this system, breaking down complex tasks and assigning them to specialized Agents for execution. This model aims to promote this tri-party contract mechanism as an open standard, but widespread developer adoption will still take time.

The structural differences between the two tracks directly affect the choice of settlement layer protocols: transactions on track A are naturally connected to fiat channels, while transactions on track B naturally rely on stablecoin channels.

Part Two: Settlement Layer

If the intention orchestration layer determines "what to trade," then the settlement layer addresses the question of "how to ensure funds arrive reliably." Currently, there are five protocols competing in this area, each with different design philosophies and applicable scenarios.

2.1 Delegated Payment / SPT (Stripe)

- Core idea: Expand upon the existing card payment ecosystem rather than rebuild it.

- Operating method: Once a user authorizes an Agent, Stripe generates a shared payment token (SPT) saved by the agent. When a transaction occurs, the agent presents this time-sensitive token with an amount cap to the merchant. The payment is then settled through Stripe's standard card payment channel. In the background, Stripe has established connections with Visa's "AI-Ready" and Mastercard's "Agentic Token." Therefore, regardless of which card organization processes the transaction, the merchant faces a unified SPT interface.

- Applicable scenario: Very suitable for standard retail and large transactions, especially for Agent-to-Agent payments requiring consumer protection mechanisms like credit card chargebacks.

- Main limitation: Its architecture relies on traditional card networks and is not suitable for high-frequency, micro-payment scenarios (e.g., below 1 cent).

2.2 Visa Intelligent Commerce and Mastercard Agentic Token

- Core idea: Upgrade tokenization technology of traditional card organizations to adapt to Agent transactions.

- Operating method: Use a dynamically encrypted payment token instead of actual card numbers. Each token is bound to metadata such as the Agent's identity, spending limits, validity period, and merchant scope. Settlement of funds is still conducted through existing card networks.

- Current development: Mastercard completed the world's first fully identifiable Agent transaction in collaboration with the Commonwealth Bank of Australia in September 2025. Visa has also completed initial deployments in Europe through its "AI Ready" initiative.

- Main limitation: The inherent minimum fee structure of card networks creates a strict limitation, making it difficult to support future potential mass low-value payments below 1 dollar.

2.3 x402 (Coinbase)

- Core idea: Return to the underlying internet protocol, using the rarely used "402 Payment Required" HTTP status code for native payment integration.

- Operating method: When an Agent requests a paid resource, the server returns a 402 response along with payment parameters. After signing authorization, a settlement node within the protocol completes the atomic exchange on the blockchain (usually using USDC), taking about two seconds. The whole process does not require account registration, API keys, or identity verification.

- Data and current status: By the end of 2025, this protocol had processed over 100 million transactions across multiple blockchains. However, some analysis pointed out that a significant portion of this volume consisted of internal testing and loop trading within the protocol. Its architecture can be designed for small-value payments without minimum fee constraints, but the current challenge lies in improving the adoption density and transaction quality in real business scenarios.

2.4 Nanopayments (Circle)

- Core idea: As an enhanced solution for x402, specifically optimizing the economic model for extremely high-frequency and low-value payment scenarios.

- Operating method: It also triggers an HTTP 402 response but adopts a batch processing architecture at the settlement layer: the payer first deposits USDC into the Circle gateway, and subsequent payments are authorized through offchain signatures and settled onchain in batches regularly. This action greatly reduces gas cost to negligible levels, supporting payments as low as one millionth of a dollar.

- Main limitation: Both parties in the transaction must pre-open an account and deposit money in Circle's gateway, making it somewhat a semi-closed system, incapable of real-time atomic fund transfers. This protocol has initiated a test network as of March 2026.

2.5 MPP (Tempo + Stripe)

- Core idea: Build a unified, pluggable multichannel payment framework while applying to become the "official solution" for HTTP 402.

- Core innovation: It allows developers to integrate multiple payment channels within the same protocol framework, enabling Agents to select as needed during transactions:

- Tempo stablecoin channel: supports per-transaction onchain settlements or offchain session batch settlements.

- Stripe fiat channel: completes card payments through shared payment tokens.

- Direct card organization channel: directly utilizes smart tokens from Visa/Mastercard.

- Bitcoin Lightning Network: integrated through Lightspark.

- Key feature: MPP introduces the concept of "payment sessions," similar to OAuth authorization, allowing Agents to conduct seamless, continuous real-time payments within a session after a single pre-authorization and recharge, without needing to put each transaction onchain.

- Strategic significance: Stripe plays a dual role here—both as a co-developer of the protocol and as one of the payment options offered within the protocol. This means that whether the market ultimately favors the open HTTP 402 system or traditional fiat channels, Stripe can ensure its core payment business is embedded in the future ecosystem.

Part Three: Current Status, Challenges, and Opportunities

3.1 Current Status and Challenges

In the past six months, the relevant core protocols have all gone live, but the commercialization process has generally lagged. In the settlement layer, x402 transaction volume is leading, but the true daily commercial transaction value is around $28,000; in the orchestration layer, ACP's core product was shut down due to low conversion rates. New protocols like ERC-8183 and MPP face a common condition of narrative outpacing implementation. This signifies a key phase: the protocol architecture has basically been completed, but large-scale commercial application has not yet been initiated.

The current core challenge is the fragmentation of the intention orchestration layer. Merchants must deal with multiple independent standards, SDKs, and compliance processes simultaneously, leading to high integration costs and unclear expectations. History shows that fragmented markets ultimately give rise to unified integration layers, but this time may be different: platforms that control traffic entry (such as OpenAI, Google, and Microsoft) have a strong motivation to build and maintain their own closed ecosystems, rather than promote open integration. This logic is taking place synchronously in global markets, and the eventual pattern is likely to evolve into multiple parallel regional closed ecosystems rather than a unified open standard. Therefore, the future integration layer will not be led by platforms but constructed by third-party infrastructure providers serving merchants.

3.2 Market Opportunities

Based on the above judgments, opportunities clearly exist on two levels:

Settlement Layer: The Most Certain Opportunity

Regardless of how fragmented the upper-layer ecosystems become, payment is a fundamental issue that every Agent must solve. A clear trend is emerging: the orchestration layer continues to fragment due to platform interests, whereas the settlement layer is moving towards abstraction and integration due to developer efficiency pressures. Developers cannot maintain independent payment integrations for every ecosystem, and the economic drive towards unifying solutions is increasingly strong.

This puts clear demands on Agent wallets: they must support multiple payment channels. The fiat channel (like SPT, Agentic Token) covers traditional consumer goods, while stablecoin channels (like x402, MPP Session) cover onchain services and A2A transactions. Both scenarios coexist, and they are not expected to merge in the short term. The responsibility for flexible adaptation lies on the Agent side, not the merchant side: merchants decide which payment channels to support, which is a relatively stable decision. Enterprises only need to configure stablecoins and authorized cards for Agents, and Agents can complete payments according to the channels supported by counterparts. Only wallets that can handle multiple channels can cover the complete consumption scenarios of Agents. Their value will continue to accumulate seamlessly with each transaction crossing different ecosystems, forming a deep infrastructure moat.

A2A Economy and Business Model Reconstruction: A Long-Term Blue Ocean Direction

The real market gap lies in service applications. Currently, the A2A economy is still limited to cryptocurrency-native scenarios. Technically, allowing an Agent to "hire" another Agent to complete real-world tasks (like data analysis, content creation, legal research, code review) is completely feasible, but corresponding on-demand API service offerings are extremely scarce. This is indeed the greatest long-term opportunity, and also the direction with the least current competition.

This opportunity is currently constrained by a real cold start dilemma: trust mechanisms based on reputation like ERC-8183 require sufficient trading density to produce meaningful trust signals. Microsoft predicts that by 2028, the number of active AI Agents will reach 1.3 billion, but there is currently a significant gap in quantity to meet this target. This is not a temporary gap that will naturally resolve but is a threshold that the A2A economy must cross to expand beyond crypto.

Its deeper significance lies in the reconstruction of business models. The mainstream internet advertising and subscription models are based on the assumption that "users are humans." Agents are not swayed by advertisements and do not require monthly subscriptions; they only pay for the results of a single task. The "pay-per-call" model represented by HTTP 402 offers a new path for API service providers: shifting from selling access permissions to selling exact results, achieving more refined value exchange. The expansion of the A2A economy and the prevalence of HTTP 402 are two sides of the same coin.

Conclusion

Agent business will evolve along two dimensions: on the consumer side (Agents shopping for humans) will mainly rely on card tracks, with development depending on the establishment of enterprise authorization and user trust; meanwhile, between Agents (A2A) will be technically ready on stablecoin tracks, awaiting the scaling of applications and services.

The final pattern will be a coordinated evolution of the dual-layer protocol stack: the intention orchestration layer determines how transactions occur, while the settlement layer ensures how value flows.

For builders, the key now is to construct broad access and integration capabilities. Those who can automatically route cross-protocol transactions and shield developers from underlying complexities will gain structural advantages when the market explodes. This is a type of value that accumulates quietly and is hard to replace.

The key moment that triggers the turning point will be when enterprises are willing to delegate spending authorization to Agents—this includes auditable transaction tracking, budget delegation mechanisms, and clear accountability in case of Agent errors. At that time, Agent wallets covering multiple payment tracks along with easy-to-use "pay-per-call" service catalogs will become the two most critical yet unoccupied pieces of infrastructure. Both positions currently lack strong incumbents, and they will become crucial at the same moment.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。