Original title: (WCTW) The Oil Market Breaking Point

Original author: HFI Research

Translation: Peggy, BlockBeats

Editor's note: This article suggests that what truly drives oil prices is not just whether conflicts end, but "when the critical point is crossed."

During nearly four weeks of ongoing conflict in Iran, the oil market is experiencing a typical case of "time pricing." The release of strategic reserves has delayed the impact but cannot eliminate the supply gap; disruptions in tanker transportation and delays in capacity recovery are continually accumulating inventory pressure into the future. Once we cross the critical juncture in mid-April, the pricing mechanism will shift from "buffered volatility" to "gap-driven repricing."

More importantly, the game structure itself is changing. The conflict no longer shows a path of "escalation to de-escalation," but shifts to a test of endurance regarding the market's critical point. Whoever can hold out until the supply-demand imbalance is priced by the market will have the upper hand in negotiations. This means that even if the conflict ends in the short term, oil prices are unlikely to return to their previous range. The current supply losses are reshaping the global oil balance for the foreseeable future.

Below is the original text:

In this article, I will break down several possible scenarios that may arise. With the Iranian conflict having lasted nearly four weeks, how will this situation affect the oil market?

On March 9, we published a public article titled "My Latest Judgement on the Oil and Gas Market under the Iranian Conflict," which stated:

Here are the impacts on oil prices under different scenarios ("loss of barrels" includes the time needed for capacity recovery):

Scenario One: Tanker transportation resumes the next day

→ Brent crude oil's average price for the year will be in the range of 70 dollars high to 80 dollars low (approximately 210 million barrels lost)

Scenario Two: Tanker transportation resumes before March 15

→ Brent's average price for the year will be in the mid-high range of 80 dollars (approximately 290 million barrels lost)

Scenario Three: Tanker transportation resumes before March 22

→ Brent's average price for the year will be at a low of 90 dollars (approximately 370 million barrels lost)

Scenario Four: Tanker transportation resumes before March 29

→ Brent's average price for the year will be in the mid-high range of 90 dollars (approximately 450 million barrels lost)

If tanker transportation does not return to normal by March 29, the oil market will face a situation that is too grim to contemplate. The only way out will be a forced contraction in demand, pushing prices to extreme levels.

Shortly after the report was released, the International Energy Agency (IEA) announced the coordinated release of a total of 400 million barrels from global strategic oil reserves (SPR). This will alleviate the shock from supply losses to some extent. But as we pointed out in our subsequent article "IEA Coordinated Release of SPR, Giving Bulls the Biggest Gift":

From a trading perspective, traders will not rush to push oil prices up until this "buffer" has been depleted. The concentrated release of SPR can indeed relieve short-term supply anxiety, but this is only a temporary solution. The market will remain tense as long as tanker transportation has not restored to normal; oil prices will gradually rise.

On the other hand, if the situation quickly eases—such as an immediate ceasefire or reaching an agreement—oil prices will quickly drop. For example, if a peace agreement is reached before March 15, global stockpiles will net increase by 110 million barrels (400 million barrels released - 290 million barrels lost).

This could push Brent prices back down to the mid-range of 70 dollars.

Conversely, if there is no peace agreement and supply disruptions persist until the end of March, global stockpiles will net decrease by 50 million barrels, and for each additional week, the gap will widen by approximately 80 million barrels.

Therefore, the role of SPR is merely to "buy time," without addressing the core issue. Tanker transportation must return to normal. However, it has indeed prevented catastrophic price spikes in the short term, thus preventing a massive collapse in demand.

Fast forward to now, and we have entered the "March 29 scenario" set at the beginning of the month. Next, we will assess the direction of the oil market based on the latest facts.

Facts

The total scale of production shutdowns from Saudi Arabia, the UAE, Kuwait, Iraq, and Bahrain has reached 10.98 million barrels per day:

Iraq: -3.6 million barrels per day

Kuwait: -2.35 million barrels per day

UAE: -1.8 million barrels per day

Saudi Arabia: -3.05 million barrels per day

Bahrain: -180 thousand barrels per day

Saudi Arabia has fully utilized its east-west pipeline capacity, currently exporting about 4 million barrels per day through the Red Sea. The UAE is also rerouting through the Abu Dhabi pipeline (Habshan-Fujairah), whose capacity of about 1.8 million barrels per day has also reached its limit. Tanker transportation through the Strait of Hormuz remains completely interrupted. In fact, even if the war ends tomorrow, it will take months to restore production and normal transportation.

Scenario Simulation

I will present three possible paths:

1) The war ends within this week, and transportation resumes by the weekend

2) The war ends in mid-April

3) The war ends at the end of April

It is worth noting that the release of 400 million barrels of SPR has bought the market more time compared to our initial judgment on March 9. The following oil price scenarios have taken this change into account.

Scenario One: Ends This Week

Impact on global stockpiles: -50 million barrels (already accounted for SPR)

Impact on Brent: Short-term drop to a low of 80 dollars, average for the year in the mid-high range of 80 dollars

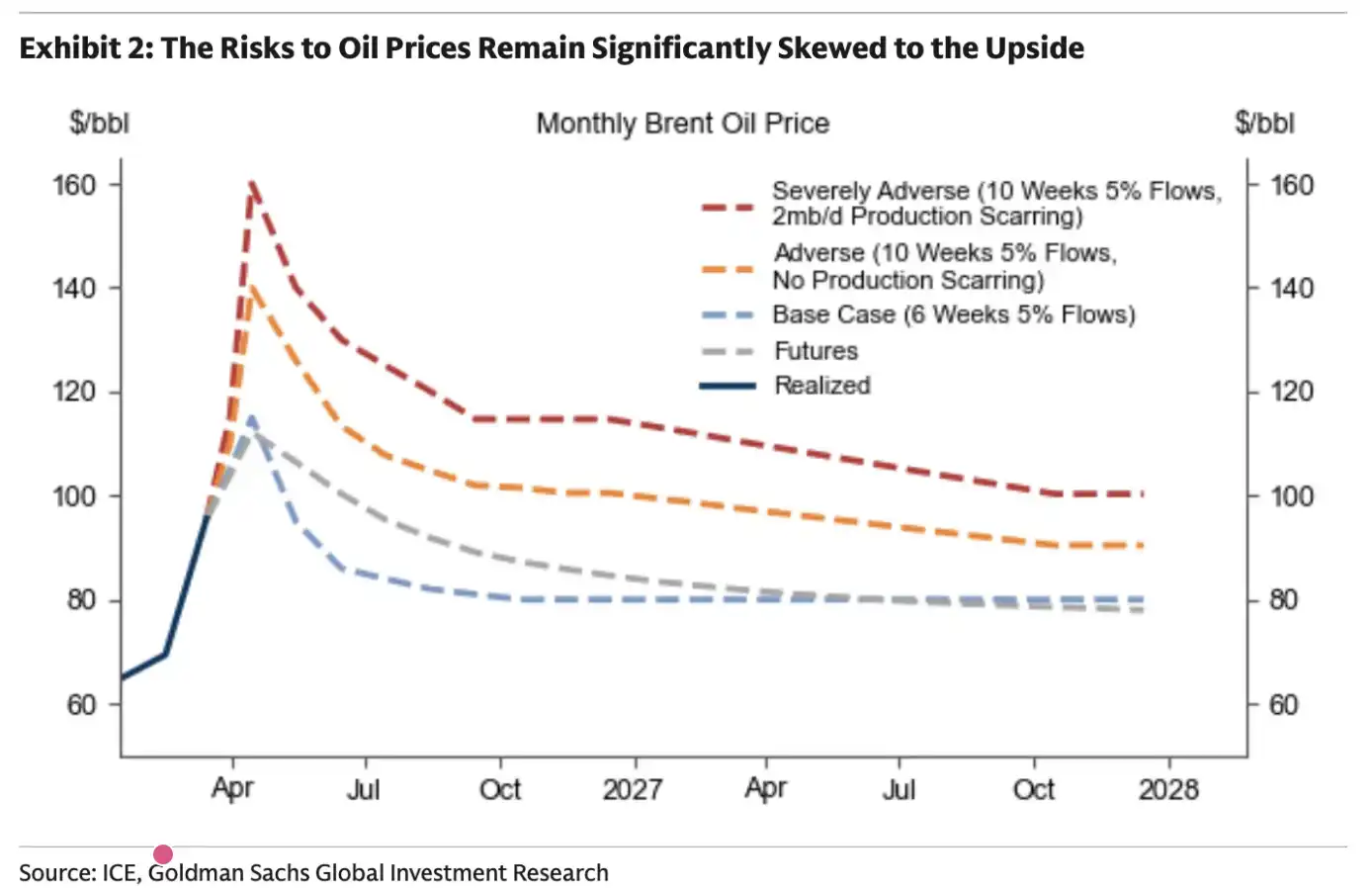

Scenario Two: Ends Mid-April

Impact on global stockpiles: -210 million barrels

Impact on Brent: Short-term drop to a low of 90 dollars, average for the year in the mid-high range of 90 dollars

Scenario Three: Ends at the End of April

Impact on global stockpiles: -370 million barrels

Impact on Brent: Short-term spike to the range of 110 dollars, average for the year in the range of 110-120 dollars

Key Turning Point: Mid-April

There is a clear "critical point" for the oil market. The current market generally expects the conflict to end before mid-April, and this expectation is crucial for the pricing of oil.

Oil prices are a product of "marginal pricing." As long as the market believes that supply is still "barely sufficient," there will be no panic. The current state of the oil market reflects just that—an absence of panic.

The Trump administration's policy statements, the relaxation of sanctions on Iranian and Russian oil, and the release of SPR all exert downward pressure on oil prices.

But once we cross this critical point, these factors will cease to apply.

At present, the evaporation effect of "crude oil in transit" has not yet truly transmitted to onshore inventories. However, our judgment is that by mid-April, this impact will be fully evident.

If the conflict remains unresolved before mid-April, the International Energy Agency (IEA) will have to coordinate again to release about 400 million barrels of strategic oil reserves (SPR). Otherwise, oil prices will surge into the "demand destruction" range (above 200 dollars).

Long-term Impacts

According to Energy Aspect's latest weekly report, the estimated cumulative supply loss in the market is about 930 million barrels. Among them, the cumulative production loss from May to December is about 340 million barrels.

This judgment is noticeably more aggressive than ours. In our inventory sensitivity analysis, we did not fully consider the reality that restoring capacity in countries like Iraq and Kuwait may take 3 to 4 months. This means that our previous estimates might be overly conservative.

For Goldman Sachs, the conclusion is straightforward: the longer the conflict lasts, the longer high oil prices will persist.

In the aforementioned scenarios, Goldman Sachs also provided a hypothesis: if the conflict lasts another 10 weeks, what will the market look like? Their judgment is basically consistent with our previous simulations.

Essentially, there is a "critical point" in the oil market. Once we cross this line, there is no turning back.

Readers need to expect that future oil prices will exhibit structural increases. Even if the war ends within this week, the supply losses that have already occurred will materially impact the future global oil supply-demand balance.

How Long Will It Last?

So far, I have avoided making a judgment on "when this conflict will end." On the one hand, I do not want to "set a flag," and on the other hand, I really cannot predict.

But one thing is clear: this time is different from previous conflicts. What was commonly seen in the past was a strategy of "escalate to de-escalate," but such signs are almost nonexistent now.

Retaliatory strikes occur without warning; Iran's range of attacks seems no longer limited to Israel, but extends to Gulf nations. It is this type of reaction that made me realize from the beginning—this time, the situation is different.

As the conflict has now lasted nearly four weeks, I increasingly worry that with no agreement reached after prolonged delays, the longer it drags on, the significantly lower the probability of reaching an agreement will become. As we analyzed in "Time Is Running Out," Iran is very clear about the operational logic of the oil market. It only needs to wait for the market to touch that "critical point" to negotiate maximum concessions from the United States. From a tactical perspective, reaching an agreement at this point offers no advantage to it. The card of the Strait of Hormuz has already been played and cannot be reused in the future.

For Gulf states, if the current Iranian regime is not overthrown, this "strangulation" situation will repeatedly occur in the future. Even if some form of "toll" mechanism is established, such uncertainty remains unacceptable.

Therefore, logically, the initiative is not in the hands of the United States, but on Iran's side. In this case, Iran is more motivated to push the situation toward the oil market's "critical point" to test the United States' endurance. All it needs to do is "hold on" for another three weeks until fissures begin to appear in the market.

However, it needs to be emphasized that I am not a geopolitical expert and do not have complete confidence in this judgment. What I can provide is only a current situation judgment based on fundamental analysis.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。