Author: Tom Wan

Translator: Jiahua, ChainCatcher

The lending landscape of Ethereum and Solana follows a remarkably similar script, with the only truly comparable phase transition (from the first phase to the second phase) occurring about 25% faster on Solana. The third phase has just begun, and whether Solana can maintain this pace remains unknown.

- Ethereum from phase one to phase two (from the peak of Compound to Aave establishing dominance): about 2 years

- Solana from phase one to phase two (from the peak of MarginFi to Kamino establishing dominance): about 18 months

- Both ecosystems are currently in the third phase, with new challengers continually closing the gap

But this time, I do not believe the outcome will be the same. The following will explain the reasons one by one.

Phase One: The Dominance of Compound and MarginFi

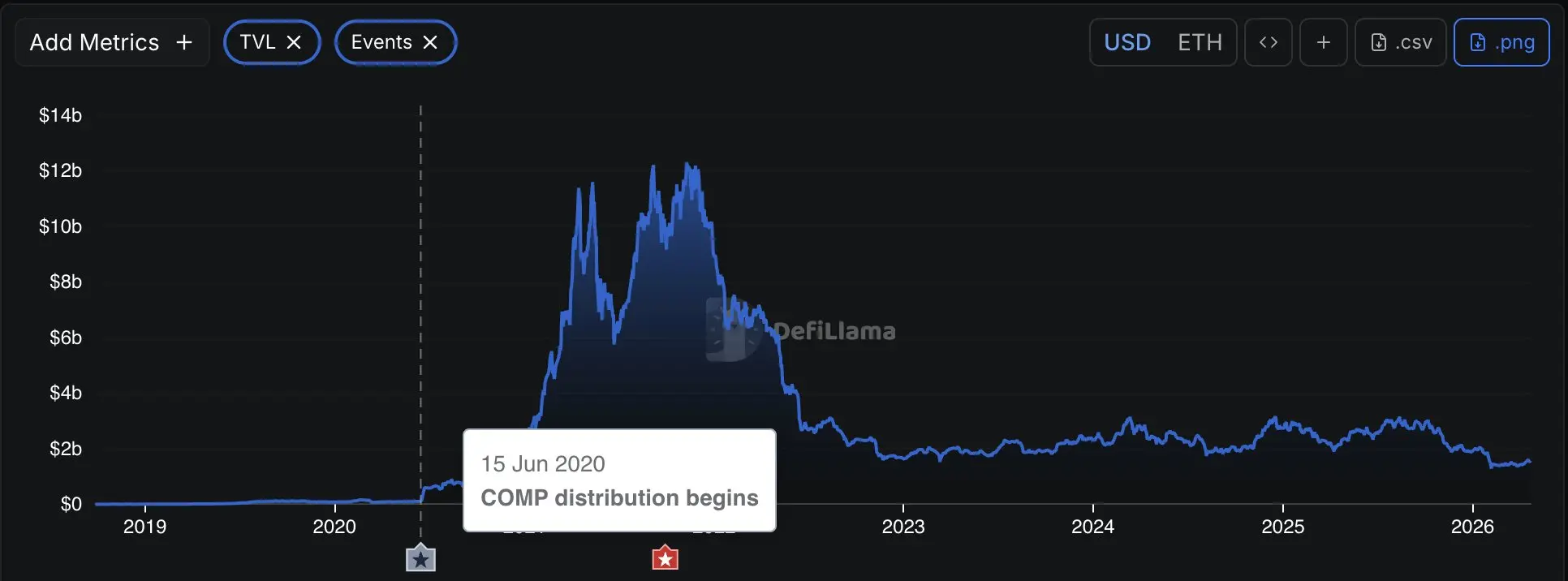

Ethereum: Compound is the protocol that truly ignited the "DeFi summer." In June 2020, the COMP token launched, directly triggering the era of liquidity mining. At its peak, Compound’s TVL was about five times that of Aave.

Solana: After the collapse of FTX, MarginFi launched a long-term points program centered on future airdrops, successfully attracting significant capital, with a peak TVL approximately four times that of Kamino.

The TVL lead of both early dominators relied on token incentives and airdrop expectations rather than true product depth. Once the market turns, this distinction becomes crucial.

Phase Two: The Rise of Aave and Kamino

Ethereum: Compound's TVL essentially consisted of mercenary funds; when the bear market hit in 2022, the value of collateral plummeted, and COMP crashed simultaneously, with mining rewards no longer sufficient to retain funds.

The damage to trust actually happened much earlier — in September 2021, a governance bug led to the excessive distribution of about $90 million worth of COMP, and users tend to remember such events for a long time. The final fatal blow came in 2023 when founder Robert Leshner publicly announced a shift in focus to Superstate, indicating that the core team had given up on this protocol.

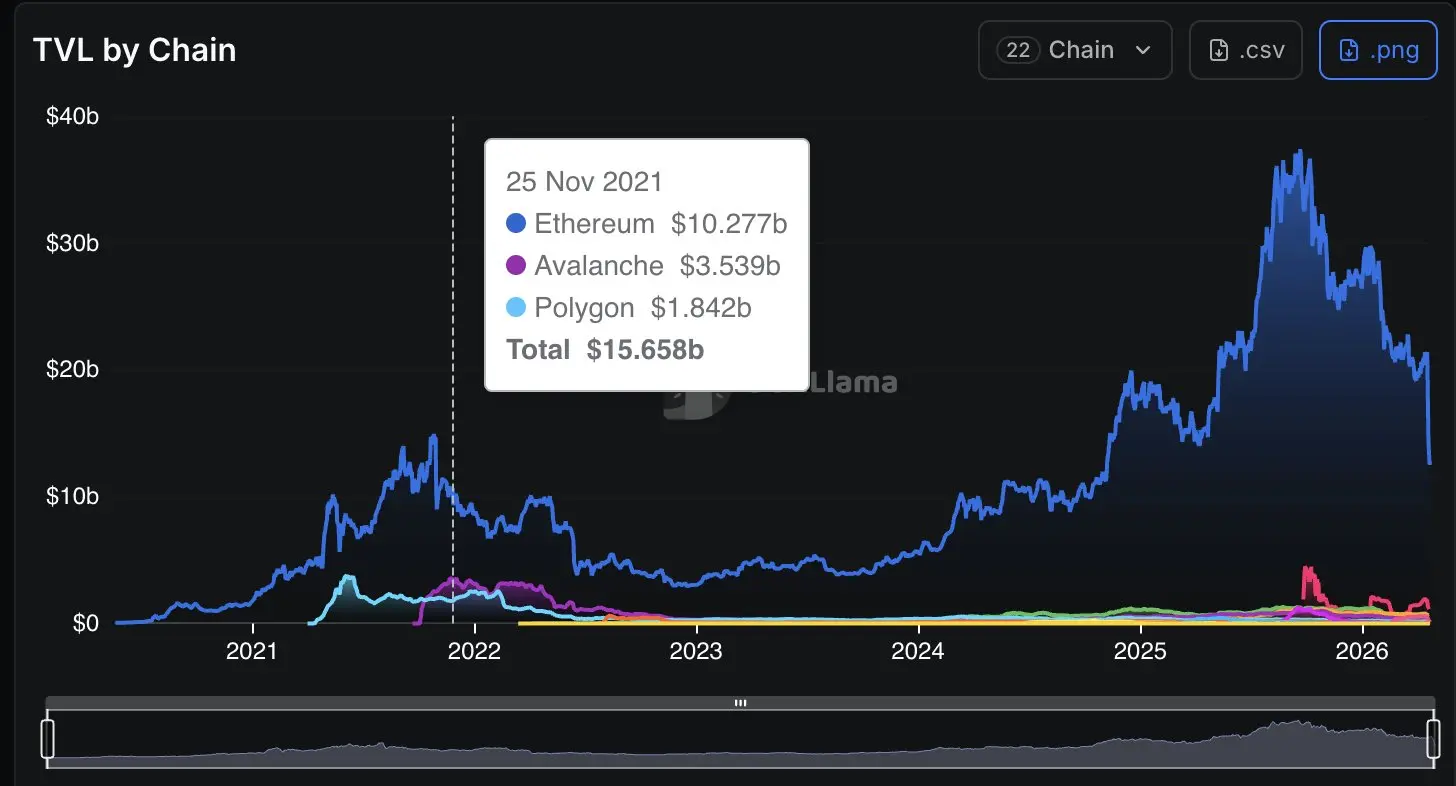

Aave defeated Compound for several interconnected reasons. It was quick to list new collateral, especially stETH, wstETH, and weETH, which made it the default place for Ethereum LST collateralized lending. It began cross-chain expansion early, completing deployments on Polygon and Avalanche through native collaborations.

Purely incentive-driven strategies often deplete token treasuries or crush token prices, but collaborative blockchains allowed Aave to achieve compounding growth of users and TVL without exhausting its own budget.

It also possesses real product depth: flash loans (which Compound never launched) and a security module (which provides real demand for AAVE tokens through staking). Today, Aave's TVL is about $16 billion, while Compound has only about 10% of that.

Solana: The decline of MarginFi stemmed from a prolonged airdrop campaign. Users provided liquidity, waiting for a token that was repeatedly delayed and ultimately concluded under unacceptable conditions, leading to collective frustration and a mass exit.

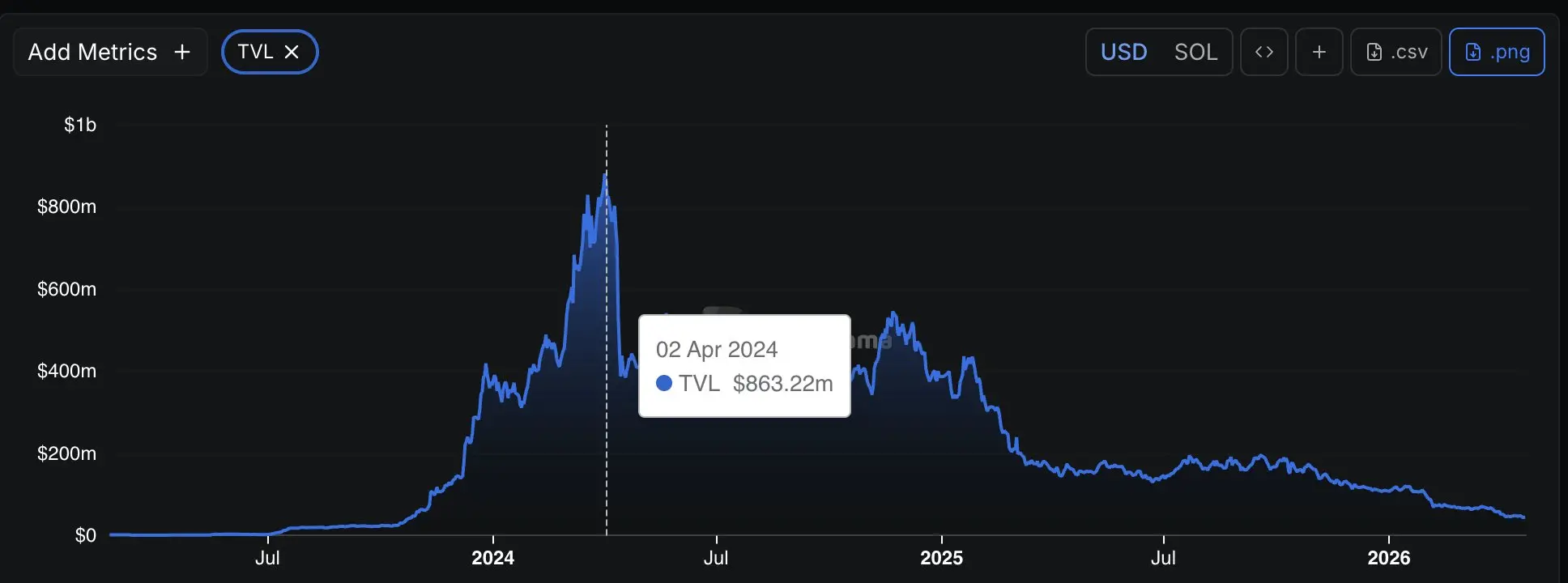

Kamino's success is more structural than incentive-driven. It was initially not a lending protocol but a management tool built around concentrated liquidity vaults, with the lending market developing alongside it.

During the Solana DeFi revival from 2023 to 2024, a surge of new assets emerged — LSTs (jitoSOL, bSOL), yield tokens (JLP), stablecoins (PYUSD) — and Kamino's positioning was spot on: it offered vault products for managing DEX liquidity, a lending market to give utility to new assets, and a Multiply product specifically designed for circular lending.

This made Kamino the go-to place for asset issuers to deploy incentives on Solana — if you are launching a new LST or stablecoin on-chain, Kamino is often your first point of integration.

Today, Kamino's TVL is about $1.6 billion, while MarginFi stands at about $45 million, only 3% of the former.

Kamino's TVL is primarily driven by the integration of new LSTs, stablecoins, and yield-bearing assets.

Phase Three: The Arrival of Morpho and Jupiter Lend

This month, both Aave and Kamino were impacted by external shocks. Kamino did not have direct risk exposure from the Drift incident (dSOL was unaffected by the hack), but depositors withdrew about $300 million as a precaution.

Aave faced a more severe blow—the rsETH was widely used as collateral for circular lending on Aave, and its TVL dropped from approximately $26 billion to about $16 billion.

The proportion change is as follows:

- Morpho to Aave's TVL ratio: from 26% to 42%

- Jupiter Lend to Kamino's TVL ratio: from 50% to 60%

Top protocols suffering from external shocks do not equal being eliminated by competition. This reveals a hidden truth in the lending space: leading projects hold the most trusted collateral (weETH, rsETH, JLP) precisely because they are leaders, and everyone tends to integrate with the winners.

In favorable conditions, this concentration drives TVL growth; however, when an integrating asset encounters problems, the leaders suffer the most due to their own success. At this juncture, challenger data looks good merely because they have smaller risk exposure — this is an illusion caused by lagging indicators, not a structural advantage.

Why I Don't Think This Time the Outcome Will Be the Same

The foundations of the existing dominators are indeed very solid. Both Compound and MarginFi are self-destructive: Compound failed due to slow governance and the departure of its founder, while MarginFi failed due to unmet airdrop promises.

Morpho is infrastructure, Aave is a product. Morpho Blue offers a immutable, permissionless market creation mechanism, with risk management handled by curators (Gauntlet, Steakhouse, MEV Capital) managing their respective vaults.

Aave is a single giant funding pool, managed through governance for listing new tokens — equivalent to a super curator. The logic behind Morpho's bets is that risk management should be decoupled and white-labeled, rather than creating a better Aave.

Jupiter Lend is a function of a super application, Kamino is an independent product. Jupiter keeps users within its ecosystem, covering DEX aggregation, perpetual contracts, prediction markets, stablecoins, LSTs, and now lending.

Users do not need the best rates across the network from Jupiter Lend; they just need to obtain sufficient rates in a familiar place. Its moat is the distribution channel, not the product itself.

What Circumstances Might Change My Judgment

- Aave v4's modular architecture fails to gain substantial market recognition and Aave v3 gets marginalized.

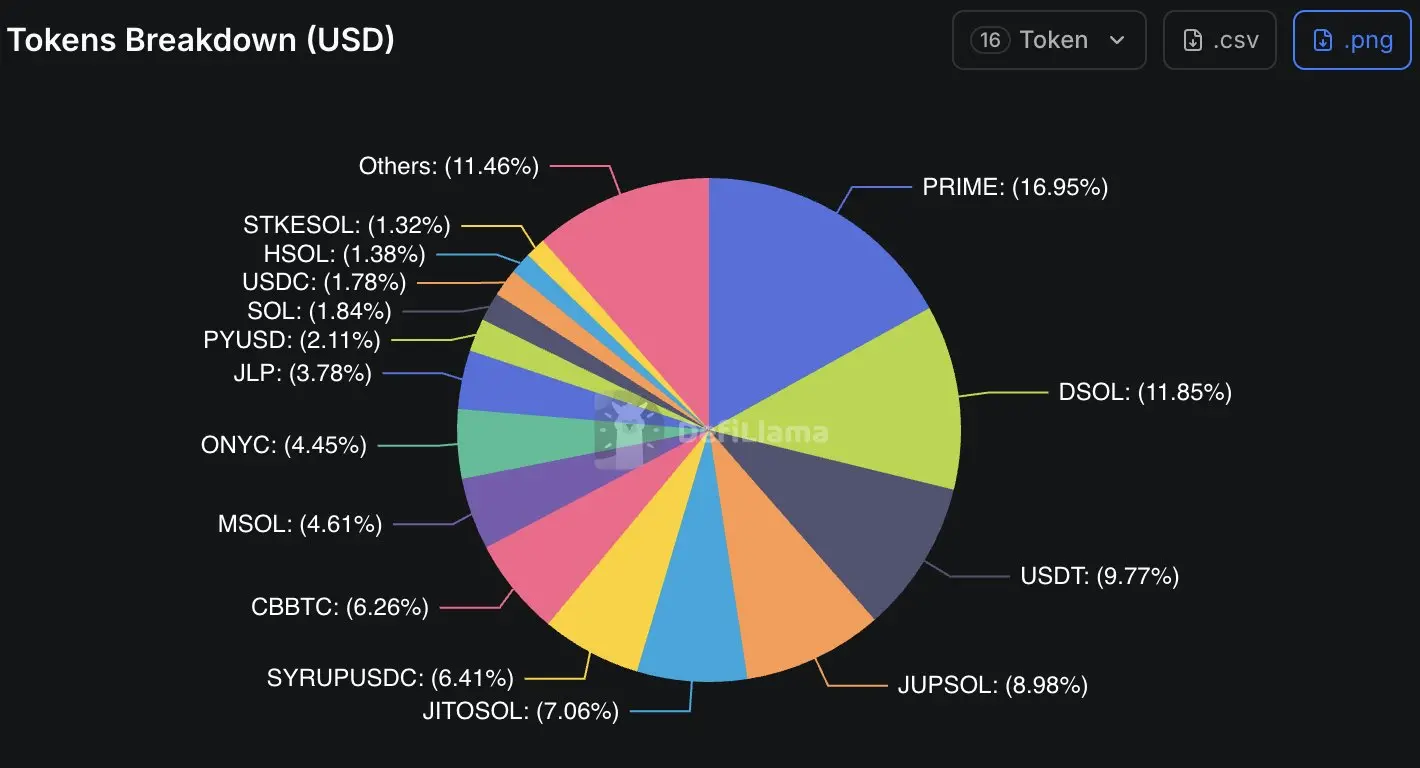

- One of Kamino's major collateral forms, PRIME, experiences a major crash. Currently, PRIME accounts for 20% of the overall size of the protocol.

Core Lessons on Protocol Growth

Relying solely on internal incentives cannot expand the lending market. The success of Aave and Kamino is built on the foundation of growing together with ecosystem partners (blockchains and asset issuers), as purely incentive spending often depletes budget or crushes tokens before product depth emerges.

In early stages, narrative speed and the effectiveness of business development (BD) are more important than protocol depth.

Aave was first to launch stETH, wstETH, and weETH and subsequently collaborated with Ethena for sUSDe circular lending, with Maple for syrupUSDC, and with Pendle for PTs.

Kamino was the first to integrate nearly every major Solana LST and stablecoin as they emerged. In both cases, the rapid capture and execution of the narrative is the true core competitive advantage over the years.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。