The prediction market is always faced with a dilemma between "information accuracy" and "market fairness."

Written by: Nic Carter

Translated by: Saoirse, Foresight News

The prediction market faces the unavoidable problem of insider trading, which is no coincidence and also leads to a significant operational failure mode.

The social value of prediction markets derives from incentivizing insiders to disclose confidential information through economic means. However, over time, this will continuously undermine the confidence of ordinary retail traders in the market.

Two days ago, the most severe scandal to date was exposed: The U.S. Justice Department charged Army Master Sergeant Gannon Ken Van Dyke with illegal trading using confidential information about the Maduro raid. He profited $400,000 through trading on Polymarket before the military operation began. He is not an ordinary soldier but a seasoned Green Beret Special Forces NCO who is deeply involved in the planning and operational deployment of special operations.

It is worth mentioning that although there is widespread compliant insider trading within the U.S. Congress, many are calling for leniency in his punishment; however, he should rightfully be sentenced to prison. His trading actions could have leaked intelligence about the raid to the Venezuelan side, which poses serious issues both legally and morally. Although Venezuela did not ultimately notice, the government cannot tolerate such a precedent: allowing active elite combat personnel to disclose details of upcoming military operations through market trading for personal gain. I understand Van Dyke's situation, but he did violate the law and betray the confidentiality obligations he swore to uphold.

This is merely the latest instance among a series of insider trading scandals and suspected violations in prediction markets. Previously, Israel arrested two reservists who traded on Polymarket using military confidential intelligence. Markets related to the outbreak of the Iran war, ceasefire negotiations, rumors of Khamenei's assassination, and Biden's pardons are also deeply embroiled in questions of insider trading, but no one has been arrested yet. Kalshi and Polymarket have also marked and banned accounts for violations, including those of three congressional candidates betting on the outcomes of their own elections.

You may think that as more people realize: not only the securities market but prediction markets also prohibit trading on confidential information, these issues will simply disappear. However, I believe the root of the problem runs much deeper.

The underlying logic of prediction markets relies on rewarding informed insider traders to achieve efficient pricing of information.

Simply put, the value of prediction markets comes from gathering a large number of ordinary retail traders who lack information advantages. The presence of retail traders provides economic returns to insiders, encouraging them to disclose private confidential information and integrate it into the market. This theory has long been recognized in the financial field, and recent academic papers have extended this logic into the prediction market field.

It is precisely for this reason that prediction markets can claim to have social value — compared to expert analysis and public opinion polls, they indeed can provide higher quality and more timely information signals. Kalshi and Polymarket know this very well but are unwilling to publicly admit it, only indirectly implying it in their promotions.

Kalshi CEO Tarek Mansour candidly stated in the Sourcery podcast: "There is no strict definition of insider trading in the commodities market; in reality, there is information differential trading everywhere." This statement is an extremely strained interpretation of the law. He added: "Indeed, a portion of non-public information is strictly prohibited from being used for trading, but the current restrictions are overly harsh."

Kalshi has been using promotional phrases like "Everything is tradable" and "Everyone has their areas of expertise," which indirectly suggest that ordinary people with special non-public information can monetize it on the platform.

Last year, Polymarket CEO Shayne Coplan had a conversation with a host during an interview with CBS:

Anderson Cooper: But the operation of prediction markets relies on some people having insider information.

Shayne Coplan: That's right. I think that traders having an information advantage is a good thing. Of course, the platform needs to manage well, clearly delineating ethics and rules, and we have invested a lot of effort in improving this. But the emergence of insider trading is unavoidable, and it brings many benefits; market participants will gradually adapt.

Shayne Coplan also stated that prediction markets are currently the most accurate information tool available to humanity and irreplaceable until a stronger information carrier emerges. A significant portion of this high accuracy comes from insider traders.

Vlad Tenev, CEO of Robinhood, which has partnered with Kalshi, proposed that prediction markets can sometimes release key messages ahead of time, even signaling before an event occurs, bearing enormous economic value.

The economist Robin Hanson, known as the "father of prediction markets," directly faced the controversy, writing a lengthy defense of insider trading behavior in prediction markets. In 2024, he said:

If the core goal of prediction markets is to achieve pricing accuracy, then it is justifiable to allow informed insiders to participate in trading. Even if this deters ordinary bettors, ensuring the accuracy of market prices must take priority; that is the primary goal.

It needs to be objectively stated that both Kalshi and Polymarket have established anti-insider trading rules. Kalshi, regulated by the U.S. Commodity Futures Trading Commission, has long prohibited trading on significant non-public information and has continuously conducted market monitoring. In an article I published in February, I mentioned that Polymarket had not yet explicitly constrained insider trading at that time; however, the platform updated its rulebook in March, clearly prohibiting the following three types of trading behaviors:

- Trading using illegally obtained confidential information (the combat plans held by military personnel belong to the government and are strictly forbidden for personal use);

- Trading based on insider information illegally leaked by insiders;

- Trading any contracts whose outcomes one can artificially influence.

This section is not deliberately accusing Kalshi, Polymarket, and their management of tacitly permitting information differential arbitrage. Objectively speaking, after the establishment of new rules in March 2026, the rules of both platforms are already clear enough. What I truly want to point out is the fundamental contradiction troubling prediction markets:

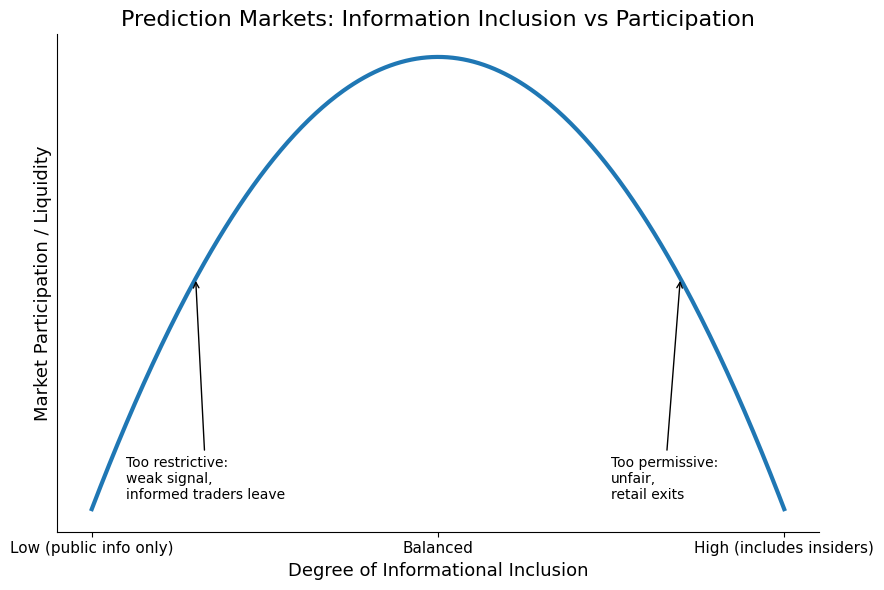

Prediction markets need informed traders to produce accurate price signals; at the same time, they cannot do without ordinary retail traders, relying on them to create profit space and attract insiders to participate. This creates an irreconcilable antagonistic relationship:

- If insider trading controls are too lax: ordinary traders will feel a strong sense of injustice and choose to exit;

- If insider trading restrictions are too strict: the market will lose its most valuable core source of information.

Ultimately, information efficiency and market fairness are destined to counterbalance and compromise with each other.

The prediction market is always faced with a dilemma between "information accuracy" and "market fairness."

This contradiction gives rise to two typical market failure modes:

Mode One: Viral Insider Trading, Retail Trader Exodus

When the rules on insider trading are too relaxed, the market's information efficiency is extremely high, and predictions are accurate, but ordinary traders will feel that the market is being artificially manipulated and that they are constantly competing against opponents holding insider information. Over time, a large number of retail traders exit, and market liquidity continues to dry up. This is also the current situation of prediction markets, but I believe that the industry will soon head toward another extreme.

Mode Two: Overregulation, Value Degradation

If platforms enforce strict regulations, relying on real-time market monitoring and comprehensive compliance reviews to rigorously mitigate insider trading, informed traders will be completely deterred. As a result, the market loses high-value first-hand information, no longer capable of predicting outcomes in advance, and will merely become a platform for aggregating public sentiment, losing the core value of "foreseeing events," and the platform's core competitiveness will also significantly decrease.

The ultimate challenge facing prediction markets today is: can a balance be found in an optimal range that ensures sufficient market liquidity, allows ordinary players to feel relatively fair, while also enabling information gatherers to earn reasonable returns based on exclusive information? A theoretical model may exist for a perfect balance, but the reality is far more complicated than imagined.

My predictions made in February remain valid:

Frequent insider trading scandals will lead retail traders to ascertain that there is dark operation in the market, losing trust and exiting en masse. I predict that this year, the frequent emergence of multiple insider trading incidents will force major platforms to comprehensively upgrade their market regulation and risk control systems, particularly Polymarket will say goodbye to its anonymous trading model.

I expect that Polymarket will completely eliminate the KYC exemption for trading channels, implement real-name verification, and intensify the screening and marking of abnormal transactions. In the future, the number of criminal cases related to confidential insider trading will increase significantly.

Even if the platforms are unwilling to publicly admit it, objectively speaking, there is indeed a scale of insider trading that represents the "social optimal level" in the industry. The challenge lies in whether the platforms can accurately control this scale and whether regulatory agencies will allow such a balanced model to exist.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。