Written by: Frank, MSX

From energy to fertilizers, from helium to AI chips, this conduction chain spanning dozens of industries is much longer than most people imagine.

Many people did not expect that a military conflict in the Middle East would eventually transmit layer by layer through natural gas, fertilizers, helium, semiconductors, consumer electronics, and other links, turning into a systemic stress test across dozens of industries.

At the end of February 2026, the U.S. and Israel launched military strikes against Iran, which subsequently restricted traffic through the Strait of Hormuz, a critical throat for global energy transport was forced into a semi-frozen state. Afterwards, Qatar's largest natural gas facility, Ras Laffan Industrial City, was continuously attacked, forcing one of the world's most important LNG production and export hubs to halt operations.

According to Reuters, about 17% of Qatar’s LNG export capacity was damaged, leading to a suspension of 12.8 million tons of LNG production annually, with some facilities potentially taking 3 to 5 years to repair.

Looking only at the surface, this seems like an energy event of "natural gas price increase."

But what is truly concerning is that natural gas is not just a fuel for power generation and heating; it is also the upstream entry for several key industrial products such as synthetic ammonia, urea, methanol, hydrogen, and helium. If this entry is blocked, the conduction chain will spread from the energy market to agriculture, food inflation, semiconductor manufacturing, and ultimately land in the valuation differentiation of technology stocks.

This is also the core logic that this article seeks to deconstruct layer by layer, that is, this crisis is not a single point impact, but a continuous conduction of four chains—natural gas prices → energy sector; natural gas → synthetic ammonia → fertilizer agriculture; helium supply interruptions → chip manufacturing; AI chips vs consumer electronics → technology stock differentiation.

1. Natural Gas Prices: The "First Shockwave" of the Energy Sector

The first to be breached is the global natural gas market.

The suspension of Qatar's LNG production alongside the obstruction of the Strait of Hormuz effectively pulled two fuses from the global natural gas supply side. On one hand, Qatar is one of the most important exporters in the global LNG supply system; on the other hand, the Strait of Hormuz is a key passage for its LNG exports. With both production and transportation sides constrained, a surge in natural gas prices is almost inevitable.

From market performance, Asian LNG spot prices once skyrocketed from just over $10 per million British thermal units before the conflict to over $25, and although it has since retreated, it remains significantly higher than pre-war levels. European TTF prices were similarly affected, and Goldman Sachs maintained its second-quarter TTF forecast around €63 per megawatt-hour, pointing out that if Qatar's supply cannot be restored by early May, prices may need to rise further to suppress demand.

This chain's beneficiaries are very direct, namely U.S. and other non-Middle Eastern LNG exporters, as well as energy companies with stable production and export capacity, will undoubtedly become the biggest winners of alternative supply, such as MSX's listed OXY.M, XOM.M, and CVX.M, corresponding to Berkshire Hathaway's long-held Western Oil, global integrated oil and gas leader ExxonMobil, and Chevron, which has both U.S. shale gas and global LNG export capability.

But the affected parties are equally clear. The Asian economies highly dependent on LNG imports are the first to suffer, especially South Korea, Japan, Singapore, Taiwan, and some South Asian countries, which explains why the rise in energy prices will not only remain on the profit and loss statements of oil and gas companies.

For importing countries, rising LNG prices mean increased power generation costs, increased industrial production costs, and rising pressure on residential electricity prices, ultimately extending the tail of inflation. For capital markets, this will compress the expectations for interest rate cuts and put greater pressure on high-valuation growth sectors due to higher discount rates.

In other words, natural gas is the first shockwave, but it is never the last link.

2. Natural Gas → Synthetic Ammonia → Fertilizer: The Neglected Agricultural Chain

The second conduction chain is more concealed yet closer to everyone's daily life, directly related to the "rice bowls" of 8 billion people globally.

Why would rising natural gas prices affect food? The logic is not complex: Natural gas is a key raw material for synthetic ammonia, which is the basis for urea and nitrogen fertilizers, and nitrogen fertilizers directly affect the global food planting costs. Hence, when natural gas supply tightens and prices rise, the production costs of fertilizers will also rise, and when traffic through the Strait of Hormuz is obstructed, the Middle Eastern fertilizer exports will further be limited by logistics.

This was clearly reflected in this round of conflict. The CRU Group pointed out that the situation in the Middle East has intensified uncertainty in urea supply. After Qatar Energy Company halted LNG and related product production in early March, QAFCO’s 5.6 million tons per year urea plant in Mesaieed was also affected, becoming the first confirmed case of fertilizer production affected in this round of conflict.

Data from IFPRI further illustrates the seriousness of the issue, indicating that in 2024, up to 30% of global fertilizer trade needs to pass through the Strait of Hormuz, while approximately 20% of LNG and 27% of global crude oil is also transported through this strait. This means that the Strait of Hormuz is not just an oil and gas channel, but an important channel for global agricultural inputs.

The danger of this chain lies in its high binding to agricultural seasons. Energy prices can rapidly respond in futures markets, but the impact of fertilizer shortages on crops has a clearly defined window. If the critical fertilization phase is missed during the spring planting season in the Northern Hemisphere, even if subsequent supply recovers, it is difficult to completely make up for previous losses. This means that the impact of this round of crisis on food prices may not fully reflect in the monthly CPI but will be released over several months through food production, agricultural product prices, and food processing costs.

However, the difficulty of the fertilizer chain is that individual fertilizer companies often find it hard to comprehensively cover the complex transfer between natural gas, synthetic ammonia, urea, agricultural products, and raw materials. Therefore, ETF tokens are more suitable to undertake this type of medium- to long-term logic, such as MSX’s listed FTAG.M, MOO.M, XLB.M, corresponding to the global agricultural supply chain, global agricultural leaders, and U.S. basic materials sector:

- FTAG.M is more inclined to be a "basket of agricultural input chains" covering fertilizers, pesticides, seeds, and agricultural machinery;

- MOO.M focuses more on global agricultural production, processing, and equipment leaders, suitable for observing the process of rising planting costs transmitting to agricultural product prices;

- XLB.M covers the basic industrial sectors such as chemicals, materials, metals, and building materials, including companies like Linde and Sherwin-Williams that are significantly affected by inflation and industrial costs.

In other words, if rising fertilizer prices represent a long chain from energy to food, these ETF tokens do not just bet on a single company but capture the re-pricing opportunities of the entire agricultural input chain through a combination approach.

3. Helium: A Systemic Risk Most People Overlook

This is the most underestimated link in the entire conduction chain but may have the farthest-reaching impact.

If the fertilizer chain connects to food, then the helium chain connects to chips.

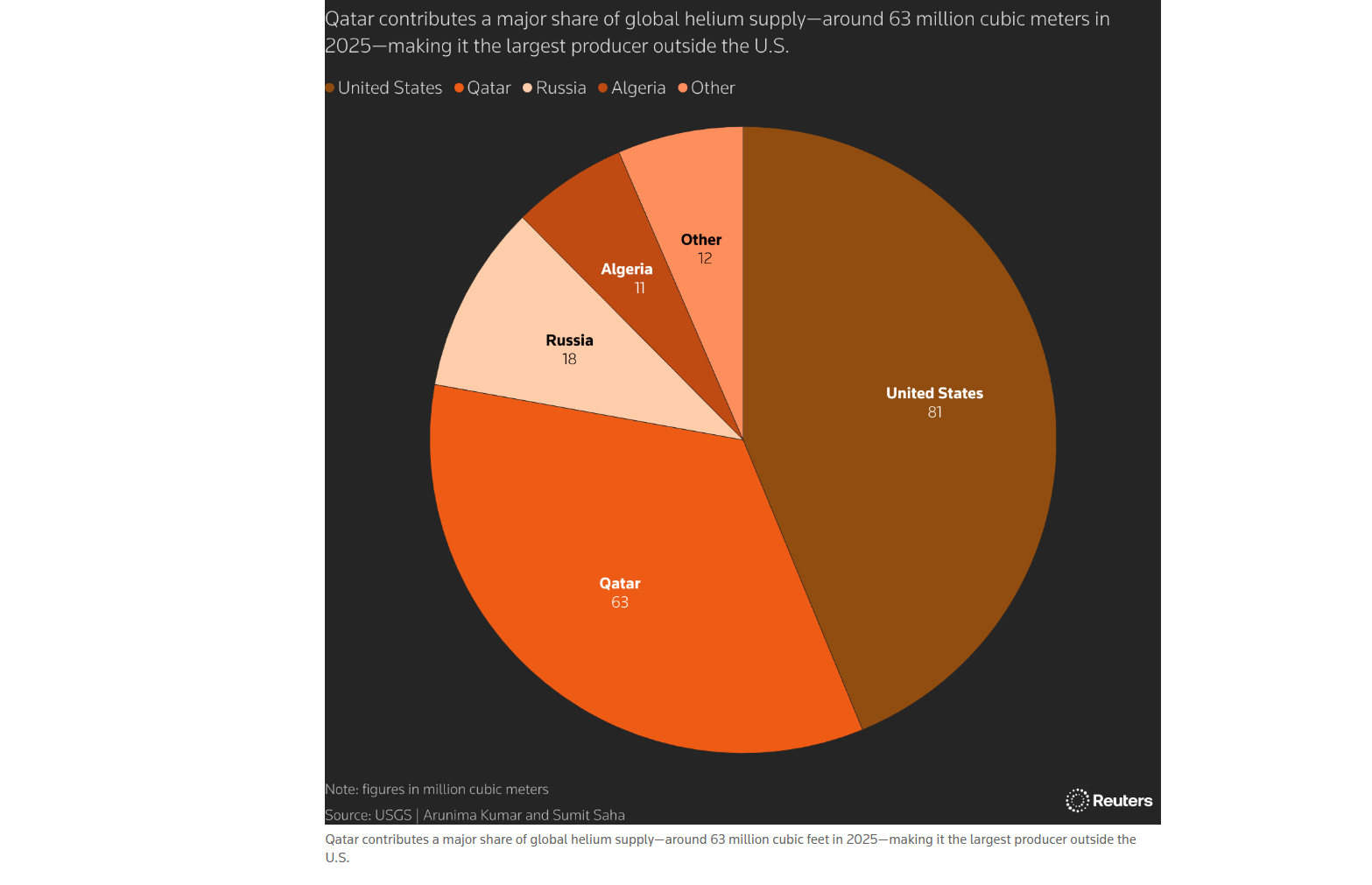

Many may wonder: how does a shutdown in natural gas plants affect semiconductors? The answer lies in the fact that helium is an important byproduct in the natural gas processing process and cannot be manufactured in large quantities through chemical synthesis. Qatar has long been one of the significant sources of helium supply globally. Reuters cited data from the U.S. Geological Survey stating that Qatar produces nearly one-third of the global helium supply; after this round of Middle Eastern conflict, tightening helium supply has already begun to affect the global technology supply chain.

Helium is almost irreplaceable in semiconductor manufacturing; it is used for wafer cooling, vacuum system leak detection, inert environment control, and certain precision manufacturing processes. For advanced manufacturing processes, temperature stability, cleanliness, and process consistency are extremely important, and helium is one of the foundational materials to maintain these conditions.

Once supply becomes unstable, chip manufacturers can buffer in the short term through inventories and recycling systems, but if shortages persist for months, production scheduling, material prioritization, and customer delivery rhythms will be forced to adjust.

Even more concerning is that unlike crude oil, helium cannot be easily stored in large quantities. It is one of the smallest monatomic gases, making it difficult to store and transport, and liquid helium transport relies on specialized low-temperature equipment. This also explains why the impact of this round of crisis on semiconductors is not just a simple "negative news for chip stocks," but rather a more segmented structural shock.

Among them, MSX’s listed DRAM.M, TSM.M, MU.M correspond to several critical observation points on this chain:

- DRAM.M is the world's first pure-play storage ETF token, covering storage leaders such as Samsung, SK Hynix, and Micron, and can be used to observe the supply-demand changes in the storage sector during the AI era, such as HBM, DRAM, NAND, etc.;

- TSM.M (Taiwan Semiconductor Manufacturing Company) corresponds to TSMC, which is a core node in global advanced process foundry and is an important supplier for terminal chips such as NVIDIA, AMD, and Apple;

- MU.M (Micron Technology) corresponds to the leading U.S. memory chip company Micron, covering DRAM, NAND, and HBM, and is more benefited by the reshaping of the U.S. domestic supply chain compared to South Korean manufacturers;

Ultimately, the real implication of helium shortages triggers a larger proposition: the global semiconductor supply chain relies not only on EUV, EDA, advanced packaging, and high-end equipment, but also on those industrial gases, chemicals, transport tanks, and regional energy security that are usually not focused on by capital markets.

This is precisely where this crisis can be most easily underestimated; it is not merely reminding the market that "chips are important," but rather reminding the market that the construction of computing power in the AI era is built on an extremely long, fragile, and globalized physical supply chain.

4. AI Chips vs Consumer Electronics: The Real Differentiation Begins

When helium shortages, rising energy prices, and delayed material transportation transmit to semiconductor manufacturing, the most common mistake the market makes is to lump all technology assets together.

But in reality, the opposite is true; this round of impact will not lead the technology sector to simply decline collectively but will drive further differentiation within technology stocks.

AI chips will certainly face short-term pressure, as advanced process manufacturing heavily relies on stable high-purity gases, photolithography materials, packaging capacity, and energy supply; the supply chain links required for HBM, GPUs, and AI servers are evidently more complex. Once upstream materials tighten, the delivery cycle of AI chips may be prolonged, and the capital expenditure rhythms of some cloud vendors and server manufacturers may also experience temporary disruptions.

However, on the demand side, the rigidity of AI chips is clearly stronger than that of consumer electronics. The competition for computing power among cloud vendors, model companies, and enterprise clients is far from over; AI infrastructure remains one of the most certain directions for technology capital expenditure. Therefore, under conditions of limited production capacity, the manufacturing side is more likely to prioritize securing high-margin, strategically valuable AI chip orders rather than first satisfying low-profit, price-sensitive consumer electronics orders.

What will be truly under pressure are the endpoints of consumer electronics such as PCs, smartphones, and tablets. This means that the core contradiction in this round of technology chain is not "whether AI will continue to grow," but "who exactly will the limited advanced capacity, storage capacity, and critical materials be prioritized for allocation:"

- Among them, NVDA.M (NVIDIA) remains the absolute leader in AI chips, AMD.M (Advanced Micro Devices) is the second-largest AI chip design force, AVGO.M (Broadcom) possesses both AI ASIC and network chip attributes;

- MSFT.M (Microsoft), GOOGL.M (Google), AMZN.M (Amazon) correspond to AI infrastructure and cloud computing demands, representing three paths: Azure + OpenAI, self-developed TPU + cloud services, and AWS global cloud services;

- In comparison, AAPL.M (Apple) and DELL.M (Dell Technologies) are more susceptible to fluctuations in consumer electronics, PC, server hardware costs, and endpoint demand, with clearer pressure logic;

- As for SOXL.M, SOXS.M and similar 3x leveraged semiconductor ETF tokens, they are more suitable for expressing short-term sentiment and sector volatility rather than long-term allocation logic;

In other words, although they are all technology assets, the risk-reward structures of AI chips, cloud infrastructure, consumer electronics, and leveraged ETF tokens are completely different. The real test of this crisis is whether investors can continue to dissect finer industry chain positions under the broad label of "technology."

For investors, what is truly worth seizing is not simply being bullish or bearish on technology stocks, but rather identifying who has pricing power, who has supply priority, and who can only passively bear rising costs within technology stocks.

Final Thoughts

Returning to the core point at the beginning of the article, this ongoing Middle East crisis lasting about 60 days transmits from natural gas all the way to AI chips, and the conduction chain is much longer and more complex than it appears on the surface.

After all, the underlying global industrial chain is not an abstract financial model, but energy, shipping lanes, minerals, gases, chemicals, equipment, and transport capabilities. In recent years, the market has accustomed itself to understanding the technology cycle through grand concepts such as "AI," "computing power," and "globalization," but this round of crisis reminds us that any narrative of high-end industries ultimately must return to the supply constraints of the physical world.

At the same time, complexity itself implies opportunities, because there are winners and losers on every conduction path; each time point and conduction chain corresponds to different trading strategies and sector opportunities.

Overall, the most critical variable moving forward remains the duration of the conflict.

If the conflict drags into May and beyond, the pressures on natural gas, fertilizers, helium, and chip chains may shift from price shocks to actual capacity constraints. By then, the market will be trading not just risk premiums but the re-balancing of global industrial chains.

Hopefully, we are all prepared for the trading opportunities that arise then.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。