Author: Alex Weseley

Translation: Deep Tide TechFlow

Deep Tide Read: Artemis has released an in-depth research report on Payward, the parent company of Kraken. Kraken has just completed a $800 million financing, with a valuation of $20 billion, and then suspended its IPO. However, in the past five months, it has obtained a master account with the Federal Reserve, acquired derivative clearing infrastructure, launched the world’s largest tokenized stock product, and reached cooperation with Nasdaq. The author, Alex Weseley, believes that the $20 billion pricing only reflects the "crypto exchange" layer, while the combination options of clearing, bank licenses, and tokenized securities have not yet been priced by the market.

Background

Payward, the parent company of Kraken, raised $800 million from institutions such as Jane Street and Citadel Securities, with a valuation of $20 billion, and subsequently submitted an S-1 to the SEC in secret, intending to go public. If successful, Payward would become the second publicly traded crypto exchange after Coinbase. But four months later, in March 2026, they froze the IPO plan citing unfavorable market conditions.

At first glance, this looks like a failed attempt at an IPO. But during the five months since the S-1 submission, Kraken's actions have clearly accelerated:

- Become the first digital asset company to obtain a Federal Reserve Master Account

- Complete the acquisition of Backed Finance, vertically integrating the ability to issue tokenized stocks

- Announce cooperation with Nasdaq to jointly build a tokenized asset channel

- Complete a $550 million acquisition of Bitnomial, securing a full set of CFTC licenses

- Deutsche Börse purchased $200 million in secondary market equity

For a company defined by the market as a "crypto exchange," these actions are too dense. In April 2026, Bitnomial’s trading again confirmed the $20 billion valuation ( Payward official announcement). The core argument of this article is: at the $20 billion price point, the profit distribution is asymmetric—downside has a valuation floor from the crypto exchange, and the upside depends on the execution of clearing, tokenization, and bank licenses.

What does Kraken look like now

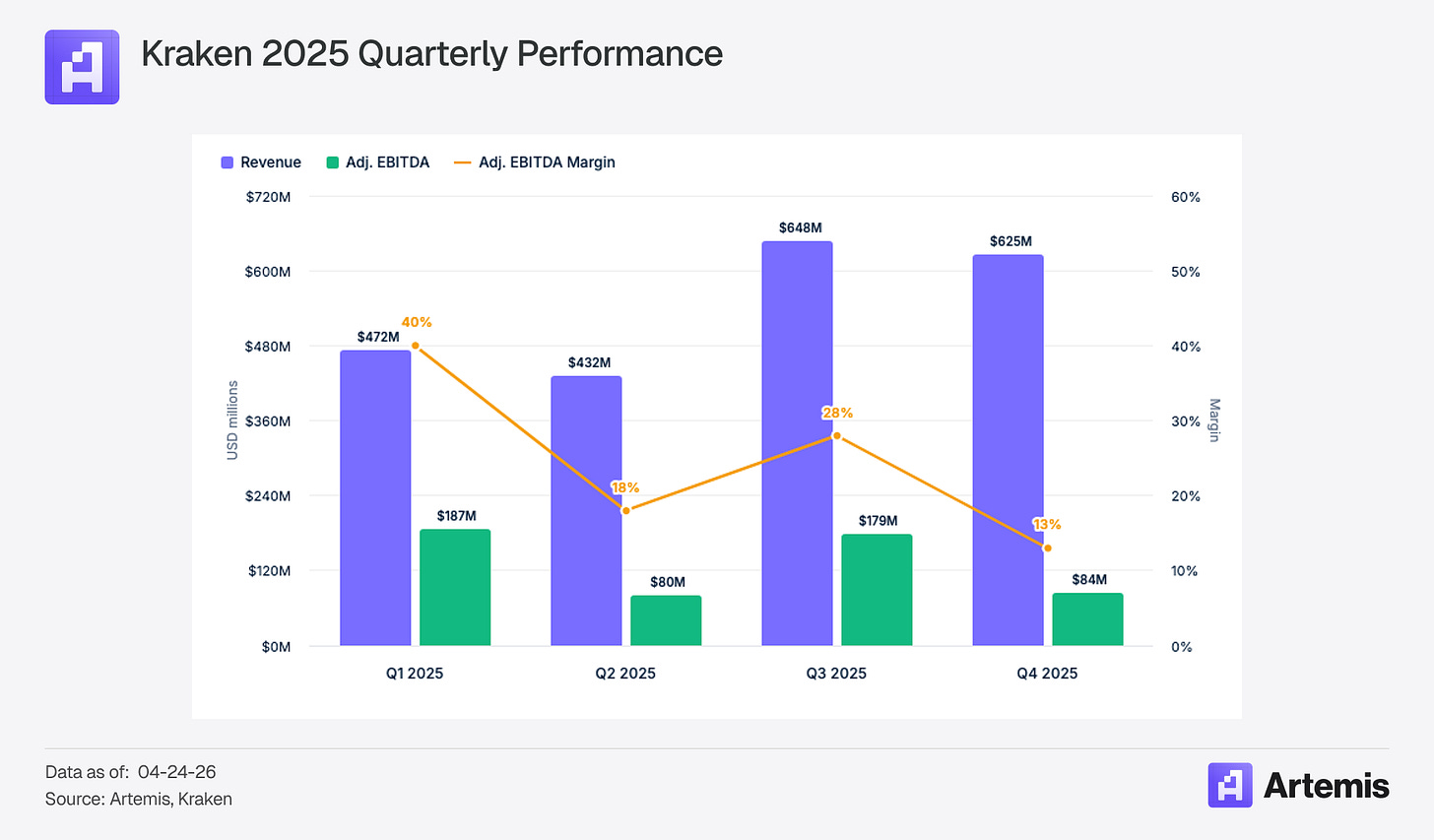

In 2025, Kraken’s adjusted revenue was $2.2 billion (up 33% year-on-year), with an adjusted EBITDA of $531 million. In terms of operational data, there were 5.7 million active accounts (up 50% year-on-year), platform assets of $48 billion (up 11% year-on-year), and platform trading volume of $2 trillion (up 34% year-on-year). The revenue structure is more diversified than most people think: trading accounts for 47%, while asset-based revenue (custody, yield, payments, financing) accounts for 53%. Most of the time, Kraken's main revenue source is actually not trading. ( Kraken financial data)

Caption: Kraken's revenue structure in 2025

Upside Leverage

Regulatory License Combination

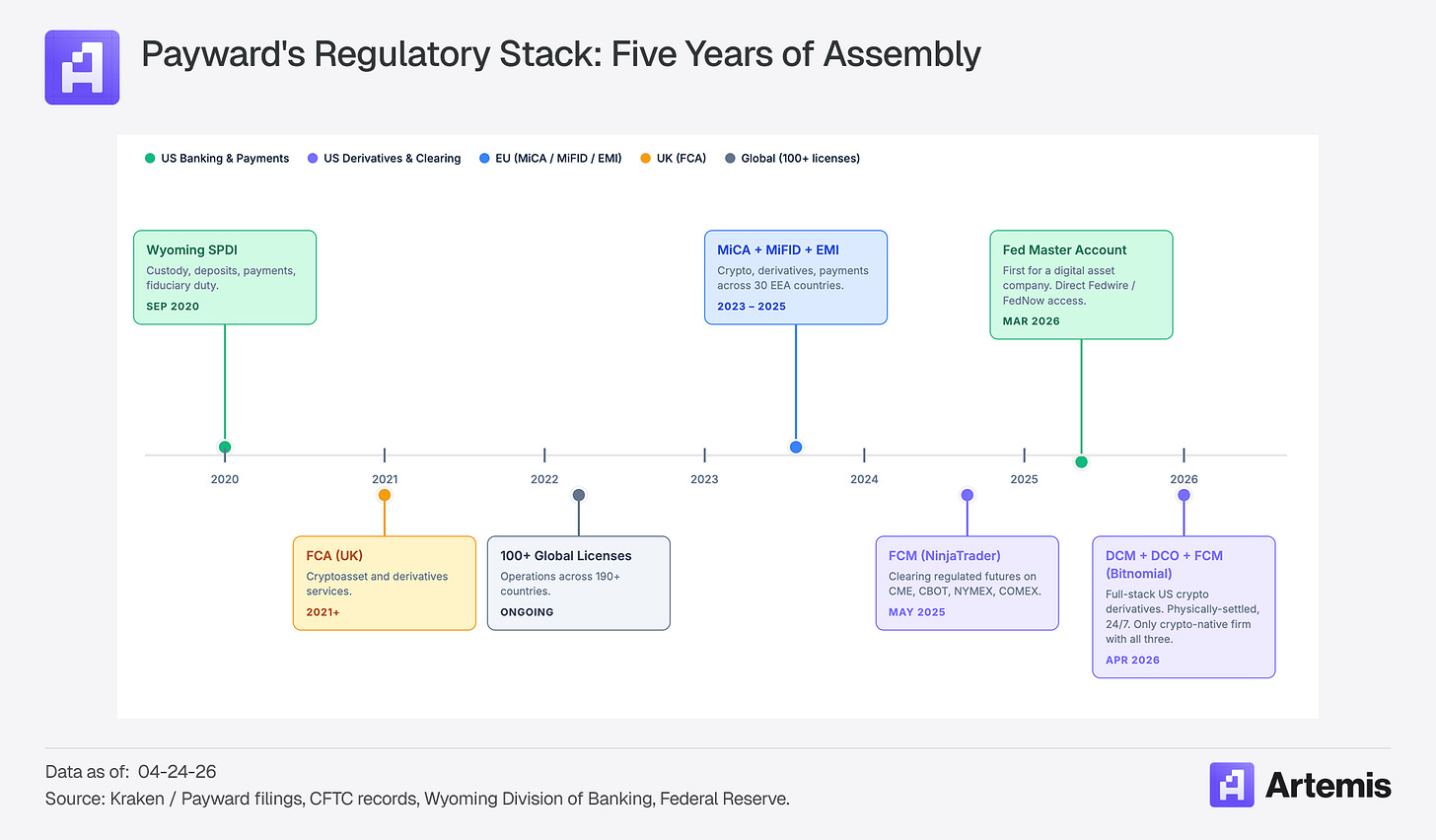

Kraken has spent over five years and invested billions of dollars to build a unique regulatory and infrastructure system in the crypto industry.

Caption: Kraken Regulatory License Matrix

The significance of acquiring Bitnomial is enormous—it allows Kraken to obtain all three CFTC licenses required for the U.S. crypto derivatives business in one go: DCM (Designated Contract Market, i.e., exchange license), DCO (Derivatives Clearing Organization, i.e., clearinghouse license), and FCM (Futures Commission Merchant, i.e., broker license).

"The form of the market is determined by the clearing infrastructure, not by the front-end interface. The U.S. previously had no clearing infrastructure built for digital assets. Bitnomial spent a decade to build it: crypto settlement, crypto collateral, 24/7 continuous markets. These capabilities cannot be replicated in traditional systems."

——Co-CEO Arjun Sethi

With the previous acquisition of NinjaTrader (which brought a distribution channel of 2 million retail futures users), Kraken now has a vertically integrated derivatives link from the front-end to clearing. Being the first to integrate DCM, DCO, FCM with physical delivery, crypto-native collateral, and a 24/7 market under one roof creates a barrier in itself. Clearinghouses are natural monopolies with strong economies of scale. Once institutions connect their risk control systems to Kraken's DCO, the switching costs will be high. CME dominates the futures market not because its interface is aesthetically pleasing, but because everyone clears there.

Other companies in the industry are also moving toward compliance infrastructure, but with different paths. Coinbase recently received conditional approval for the OCC national trust license, which enables it to offer a unified custody and settlement framework across all 50 states in the U.S.—which is reasonable for a company that provides custody for most U.S. spot crypto ETFs. Kraken's Wyoming SPDI is a state-level license, but with broader functional authority: it can accept deposits, provide payment services, and operate with fiduciary duties. This distinction is crucial, as it allows Kraken's roadmap to extend into banking products (deposit accounts, stablecoin issuance, FedNow payments), which a pure custody license cannot. The master account obtained from the Federal Reserve in March 2026 is the foundational layer to activate these capabilities.

Tokenized Stocks and xStocks

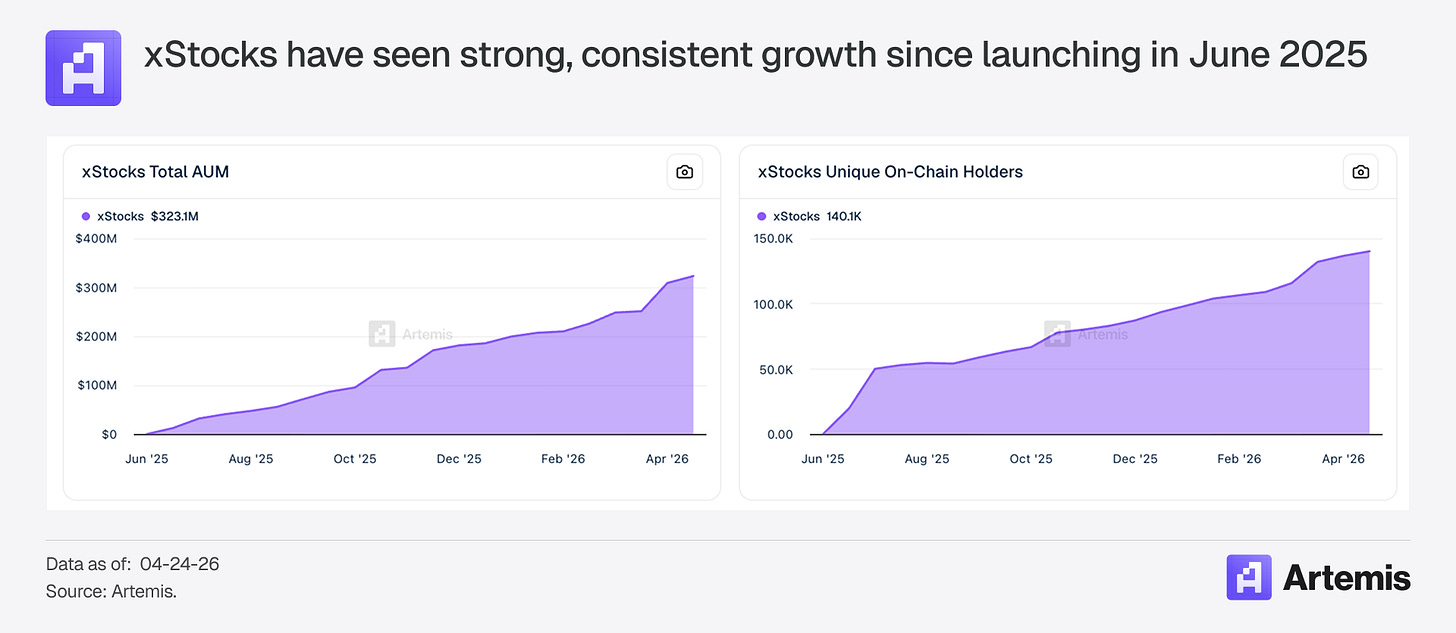

In June 2025, Kraken, in collaboration with Backed Finance, launched xStocks, supporting trading of tokenized U.S. stocks and ETFs 24/5. In less than a year, xStocks' AUM surpassed $320 million, covering more than 100 tokenized stocks, deployed on Ethereum, Solana, Ink, and Ton. xStocks is currently the world's largest tokenized stock product.

In December 2025, Kraken announced its acquisition of Backed Finance, the Swiss issuer that mints these tokens. Thus, Kraken acquired a complete vertical chain: issuance (Backed), trading (Kraken), settlement (Ink), custody.

Caption: xStocks Tokenized Stock Product Structure

Then came the announcement of the partnership with Nasdaq:

"The collaboration between Nasdaq and Payward... will focus on designing a stock conversion gateway that allows issuers and investors to seamlessly flow between permissioned and public chain environments." ( Nasdaq announcement)

Kraken is becoming the owner of essential infrastructure connecting traditional securities and public chains. Nasdaq's Equity Token framework is expected to go live in the first half of 2027, with Payward serving as the primary settlement layer. (Nasdaq has previously collaborated with projects such as Ondo, Republic, etc. for tokenization. Business terms were not disclosed, and products have not yet launched.)

Coinbase and Robinhood have both announced plans for tokenized stocks, but as of April 2026, neither has officially launched a product backed by physical assets. Kraken's xStocks already has $323 million AUM, 140,000 on-chain holders, and achieved DeFi composability across multiple protocols. Kraken has a first-mover advantage, but the scale of $320 million AUM is more like an option value and does not yet constitute a moat. The partnership with Nasdaq is a potential catalyst to transform this option into a lasting advantage.

Ink: Toll Station

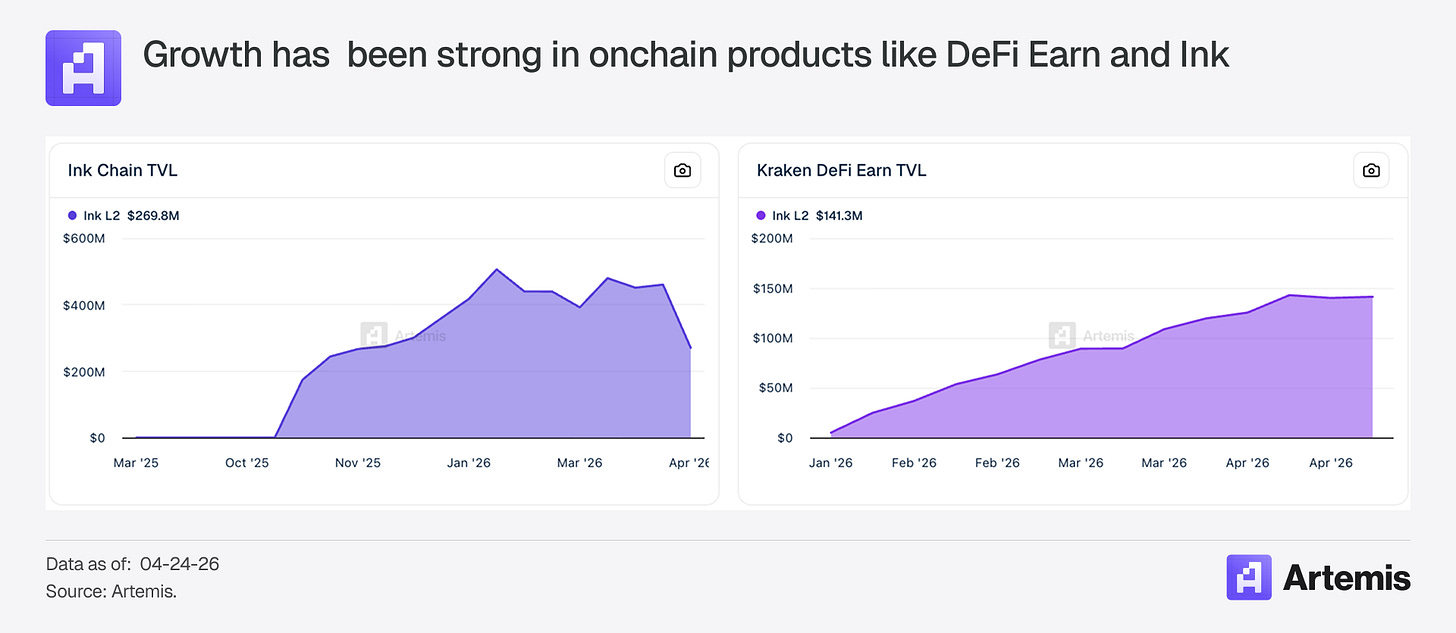

Ink is Kraken's Ethereum L2 built on the OP Stack. The mainnet launched in December 2024, with a TVL of approximately $270 million (after the KelpDAO vulnerability incident). Application revenue increased from $500,000 in October 2025 to $5.77 million in January 2026. Kraken exclusively operates the sequencer, meaning 100% of the gas fees belong to Kraken.

Caption: Ink L2 Revenue Growth Trend

If the settlement of xStocks fully moves to Ink, every tokenized stock transfer, DeFi interaction, and lending transaction will generate fees for Kraken's sequencer. It acts like a toll station spanning between traditional finance and on-chain markets. Compared to more mature L2s, Ink is still early—Coinbase's Base generated approximately $75 million in sequencer revenue in 2025, making it the largest L2 so far. But Ink's growth curve is steep, and it has xStocks as a differentiated asset to drive on-chain activity, which other L2s lack.

Platform Vision

The management’s direction for growth is clear: expand asset classes (tokenized stocks, foreign exchange, futures, RWA), enhance asset productivity (custody, payments, yield, financing, settlement), and achieve global expansion through "a single global core" complemented by localized entry points. ( Kraken Blog)

Asset productivity has the most significant impact on valuation. This model is not unfamiliar: when Charles Schwab obtained a bank license in 2003, the market widely questioned why a discount broker would want to be a bank, but net interest income later became Schwab’s largest source of revenue. Of course, the analogy has boundaries—Schwab was already the largest discount broker in the U.S. when obtaining the license, managing $800 billion in customer assets. Kraken has platform assets of $48 billion, and the Federal Reserve account has just been obtained. A more relevant recent reference is SoFi: net interest income grew from $252 million in 2021 to $2.2 billion in 2025, but SoFi’s market cap is around $23 billion. The market recognizes the bank economic model but does not easily grant growth premiums. Kraken’s differentiation must come from this crypto-native perspective.

Early signs have already appeared. Instant dollar withdrawals (24/7/365, 1.5% fee, capped at $50) are likely to run on FedNow. The Krak App has been downloaded over 450,000 times in 130 countries ( The Block). The unified wallet has already achieved cross-margining between spot, margin, and futures within crypto assets. The next logical step is to expand cross-margining to crypto + xStocks + NinjaTrader futures, which will be a highly differentiated product, and Kraken's license combination is precisely the best foundation for building it.

Stablecoins: The Biggest Shortcoming

Stablecoins remain the largest gap for Kraken relative to competitors. Coinbase’s USDC revenue sharing agreement is expected to contribute around $1.35 billion in 2025, with high profitability and strong repurchase. Kraken lacks a comparable revenue source. USDG (a collaborative stablecoin with Robinhood, Paxos, and Galaxy) has a market cap of $1.95 billion, compared to USDC's roughly $76 billion. Kraken also has a distribution partnership with Circle and plans to issue a compliant stablecoin in Ireland under MiCA. Whether it can close this gap—through the scaling of USDG, issuing a U.S. stablecoin under SPDI after the passage of the GENIUS Act, or another path—is a key strategic question.

Valuation

Kraken does not belong to any single category. It spans crypto exchanges, futures clearing, tokenized securities, banking, and L2 infrastructure.

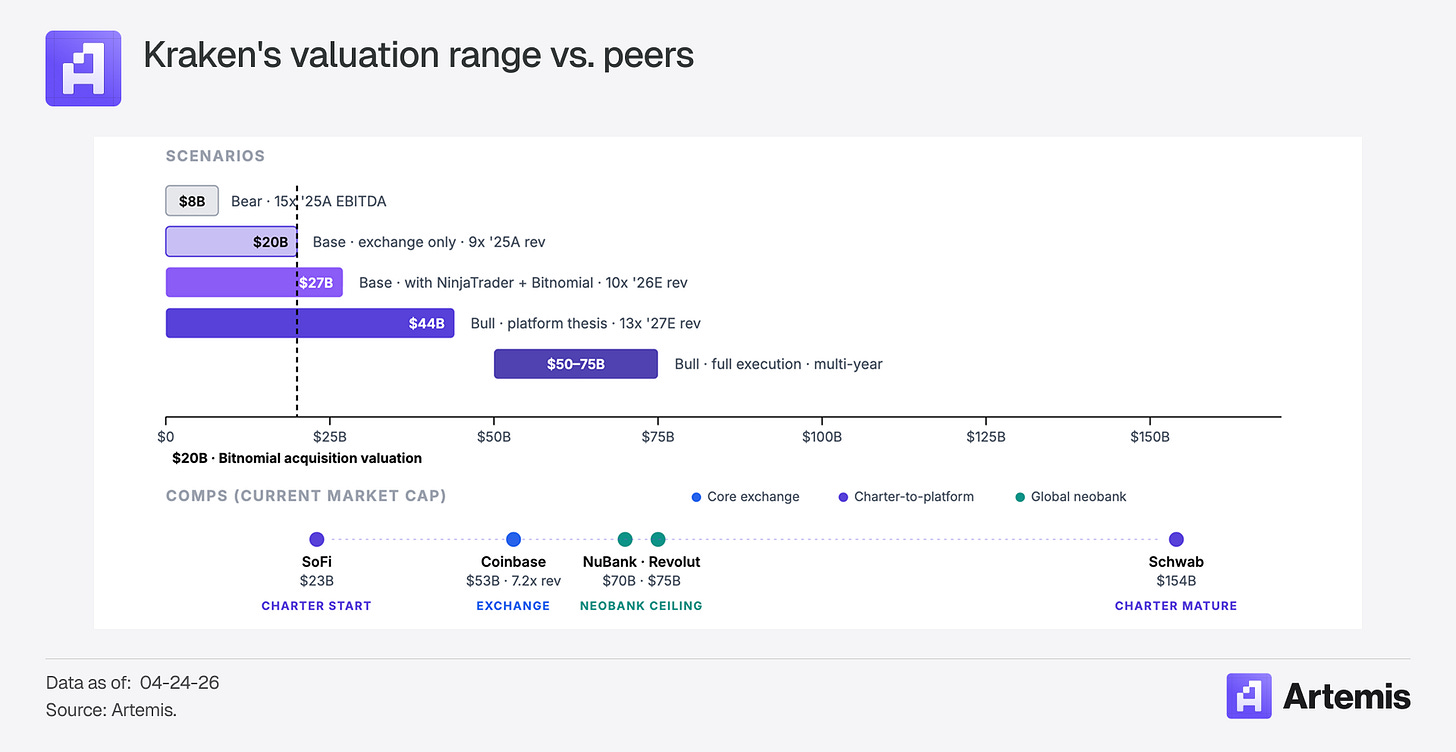

A $20 billion valuation is roughly reasonable for the parts the market can verify today: a cyclical exchange priced at 8-9 times revenue, plus a maturing derivatives business. The institutional investors in November 2025 reflected a pricing based on what they could see. What has not yet been fully priced is the distribution of results from here on. The downside is anchored at the valuation floor of exchanges: even if the platform logic never materializes, the base case implies an enterprise value in the range of $20-27 billion. The upside depends on the execution of three independently operating but yet-to-be-verified catalysts: Bitnomial's clearing scale-up, xStocks' U.S. launch, and bank products on the Federal Reserve master account. Betting at this price point is not about misjudging the market's current evaluation of Kraken but betting that the result distribution starting from $20 billion is asymmetric—downside has a floor, upside is open.

Caption: Kraken Valuation Scenario Analysis

Risks

The cyclical nature of crypto is the biggest short-term risk. Revenue increases from $696 million in 2023 to $2.2 billion in 2025. Staking, margin interest, and custody fees are all highly correlated with coin prices. No matter how you break down the 47/53 revenue structure, Kraken's revenue is essentially crypto beta.

U.S. xStocks approval is the biggest catalyst, but also the biggest uncertainty. Without the U.S. market, xStocks is meaningful, but not enough to change the investment thesis.

Regulatory moats may erode over time. The clearer the crypto regulation becomes, the more companies will obtain more licenses. Kraken's advantage lies in its combination and first-mover status, not in permanence.

Institutions will eventually join the game. If tokenized stocks truly become mainstream, BlackRock, JPMorgan, Fidelity, and Goldman will step in with larger balance sheets, deeper client relationships, and established distribution networks.

If everything goes smoothly

- U.S. xStocks launch: a step function leap in trading volume, user numbers, and narrative

- Federal Reserve master account launching bank products: non-cyclical recurring revenue

- Cross-asset cross-margin products: attracting currently displaced institutional funds

- Bitnomial clearing infrastructure: massive physical delivery of crypto derivatives

- Issuing stablecoins under SPDI license: direct net interest income

- NinjaTrader cross-selling: 200,000 futures traders converting at 10% = 20,000 high-value accounts

Kraken is the first crypto-native company to gather the full set of U.S. clearing licenses and also holds the largest tokenized stock product globally. Whether this advantage will compound growth or be eroded by competition will determine whether it truly is a $20 billion exchange or much more than that. No other company simultaneously holds clearing, tokenized stocks, bank licenses, and a Federal Reserve master account. Each individual piece can be replicated. But this combination—the first to be completed—is where the bet of this investment lies.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。