Original text from:Prediction Market Accuracy: Crowd Wisdom or Informed Minority?

Translation | Odaily Planet Daily (@OdailyChina)

Translator | Wenser (@wenser2010)

Editor's Note: For a long time, prediction market platforms like Polymarket and Kalshi have defined themselves as "a concentrated manifestation of collective wisdom," distinguishing themselves from betting platforms and enhancing their valuations by emphasizing this narrative. However, a recent paper from the London Business School and Yale University, after dissecting Polymarket's on-chain data, found that less than 4% of addresses drive price changes and enjoy substantial profits, while approximately 97% of addresses are mostly "also-rans," with over 67% of individuals experiencing losses. Considering that the number of Polymarket user addresses has now exceeded 2.43 million, the data in this paper may exhibit some lag, but the phenomena it reveals are still worth deep reflection.

Below are the main core contents of this paper, summarized by Odaily Planet Daily.

Truth One: The accuracy of prediction markets is unrelated to "collective wisdom" and is determined by 3.14% of a minority

This is the core conclusion of the entire paper and a direct challenge to the industry narrative.

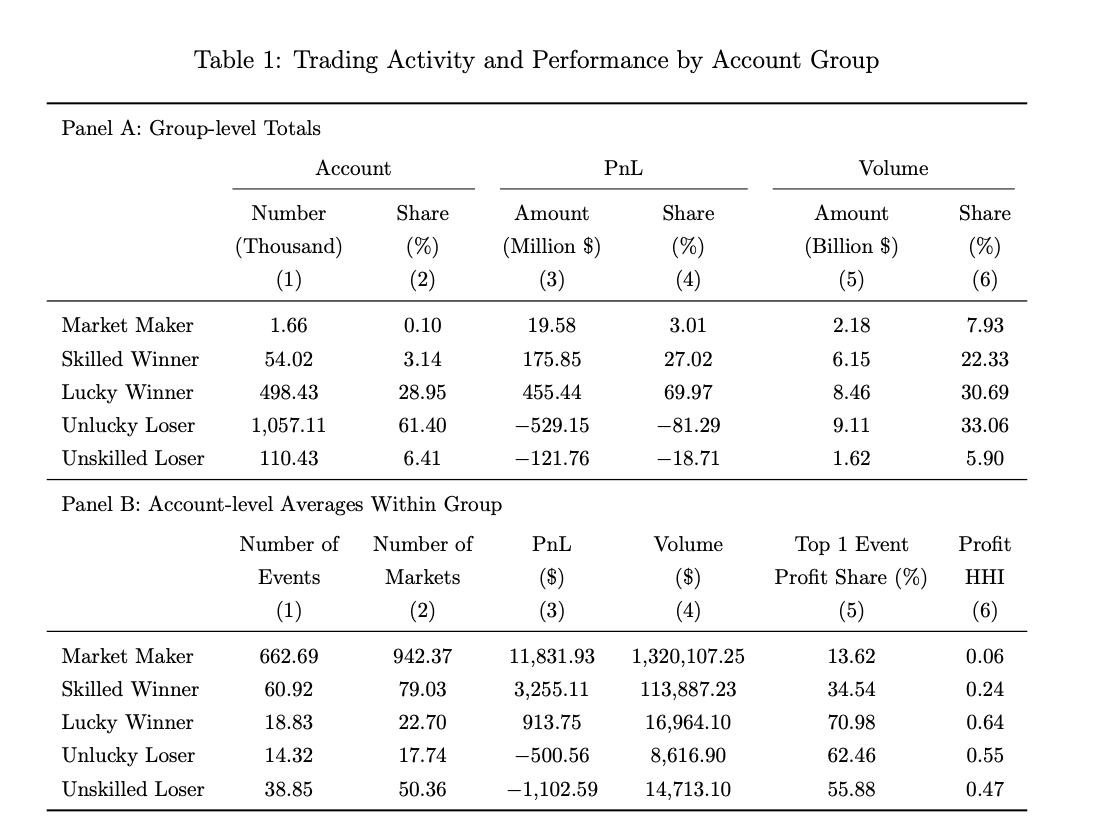

Previously, several representative figures in the industry have taken pride in this: Kalshi CEO Tarek Mansour said that prediction markets "utilize collective wisdom," Polymarket CEO Shayne Coplan has repeatedly promoted that "financial incentives can aggregate information more effectively than experts," and Robinhood CEO Vlad Tenev referred to it as "capitalism's pursuit of truth." However, study data informs us: among the 1.72 million Polymarket accounts, only about 54,000 accounts (3.14%) are identified as "skilled winners" (Odaily Planet Daily Note: this type of individual is characterized in the paper as being able to average judgments and absorb information, while also reacting efficiently when news occurs).

The primary driver of price discovery in prediction markets is this minority group, not the crowds that often hide behind "collective wisdom."

Truth Two: Both earning and losing money may be luck; 67% of participants are essentially "philanthropists"

In this paper, Roberto Gómez-Cram et al. used a sign-randomization statistical method to categorize all traders' accounts into four types: skilled winners (3.14%), lucky winners (29.0%), unlucky losers (61.4%), and skilled losers (6.4%).

The most counterintuitive number is that the lucky winners account for nearly 30%, and they made money, but their trading contributed nothing to price discovery, statistically it is no different from randomly flipping a coin.

In other words, making money in prediction markets and "having the ability to predict the future" are two different matters; while the approximately 67% of loser group bear all the losses, essentially paying for the informational advantage of a few.

Truth Three: Among the top profit earners, 88% make money by luck

Among the 54,000 traders ranked by actual profit on Polymarket, only 12% are also identified as "skilled winners" by statistical methods.

That is to say, the vast majority of big winners on the leaderboard made their gains through a few lucky bets.

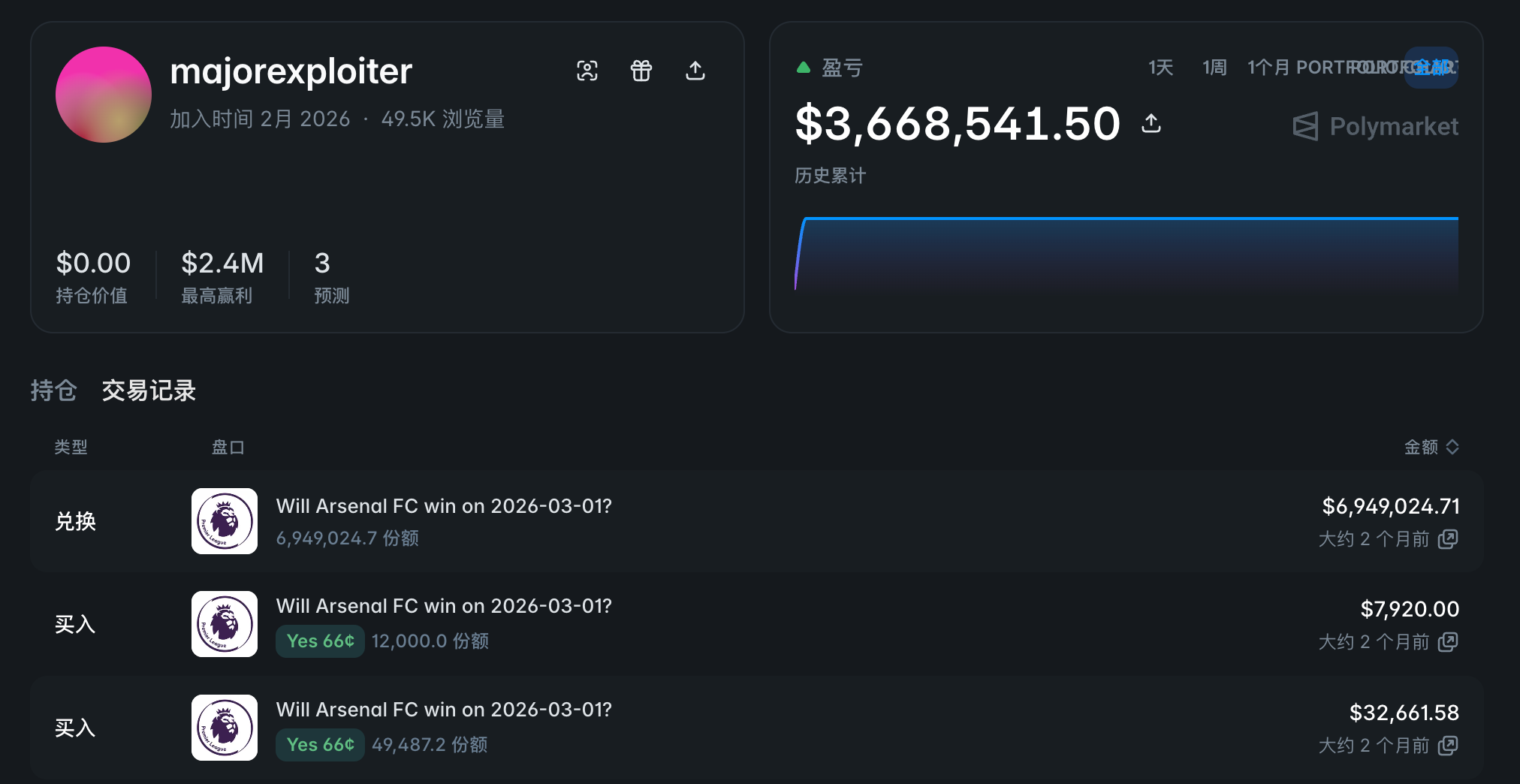

A typical case is account @majorexploiter—in a weekend at the beginning of 2026, this account invested $4.5 million on three sporting events and profited over $3.6 million.

This kind of concentrated betting profit is extremely unsustainable, as 60% of lucky winners turned into losers in out-of-sample validation.

Truth Four: The skill efficacy in prediction markets far exceeds that of traditional fund industries

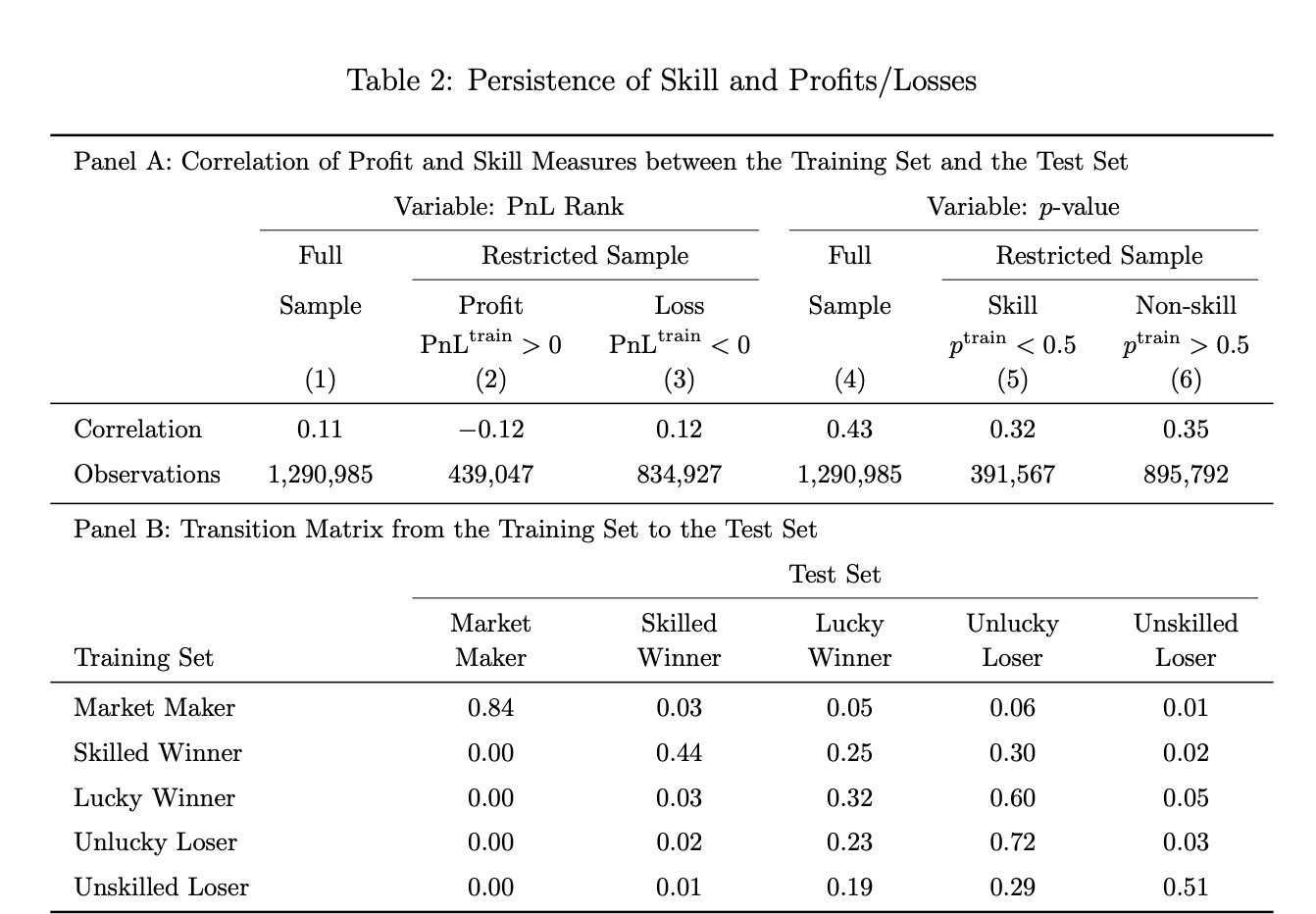

The researchers randomly divided betting events into training and testing sets for out-of-sample validation.

Results showed that accounts identified as "skilled players" in the training set, 44% remained identified as "skilled users" in the testing set; in contrast, American actively managed mutual funds had a skill efficacy of only 10% in the same test.

Conversely, "anti-skill" (sustained losses) also maintained high consistency: 51% of "skilled losers" in the training set continued to be losers in the testing set, whereas this number for American mutual funds rose to 20%.

The final conclusion is that the experts in prediction markets are true experts, and the novices are true novices.

Truth Five: Skilled winner orders are highly correlated with the direction of final results

Researchers calculated that the net buying index (OIB) of skilled winners increases by about 2 basis points in the next price when it increases by 1%, and the probability of the final event occurring increases by about 8 basis points, with high statistical significance (t-values of 12.71 and 9.51 respectively).

In contrast, the order flow of lucky winners is not significant on both metrics (t-values of only 1.47 and 1.49).

In other words, even though lucky winners have positive profits, their trading operations do not carry informational content—this conclusion is very solid from a data perspective.

According to the study, it can be observed that in markets where the settlement result is "yes," skilled winners are net buyers; in markets where the settlement result is "no," they are net sellers; they are consistently building positions in the direction of the final result. Market makers are usually net sellers in markets that settle as "yes," and net buyers in markets that settle as "no," consistent with their role of profiting from directional order flow rather than establishing insider orders.

Truth Six: Skilled traders are the only group that makes prices more accurate

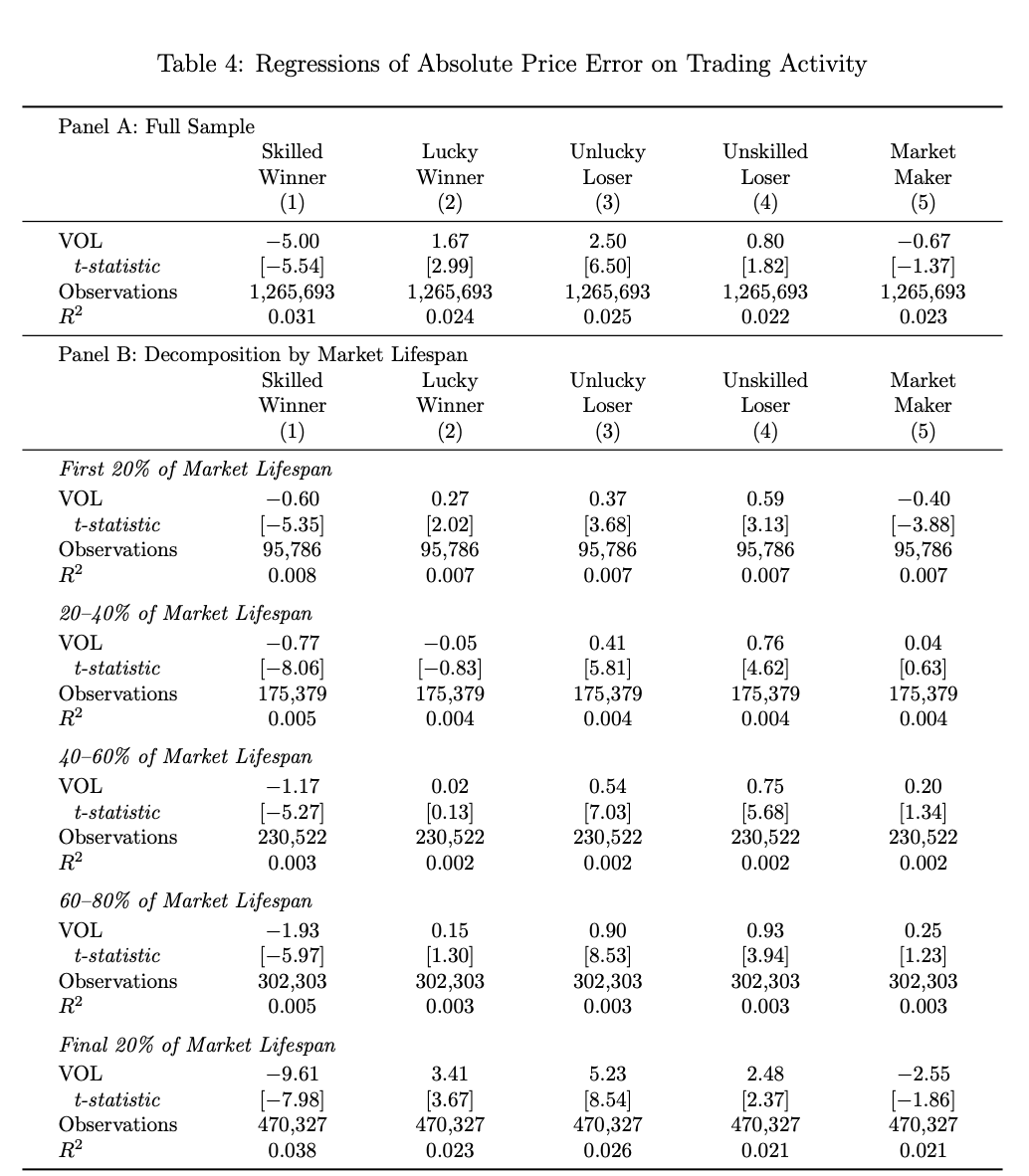

Based on the premise that "some trades actually drive prices towards final results," researchers created a "price discovery contribution index" to measure whether prices are closer or further from final result accuracy within each time window.

Results indicated that it is only when the trading volume proportion of skilled winners increases that the betting event can significantly reduce pricing errors (coefficient -5.00, t-value -5.54).

Conversely, trades from the other three groups—lucky winners, unlucky losers, and skilled losers—actually lead to prices deviating from final results—indeed, most are just generating noise at the trading level, and this impact grows larger as the market approaches settlement. Within the last 20% of the lifecycle of bets, the contribution coefficient of skilled winners expands to -9.61.

Truth Seven: Skilled winners are the only "News Trading" players

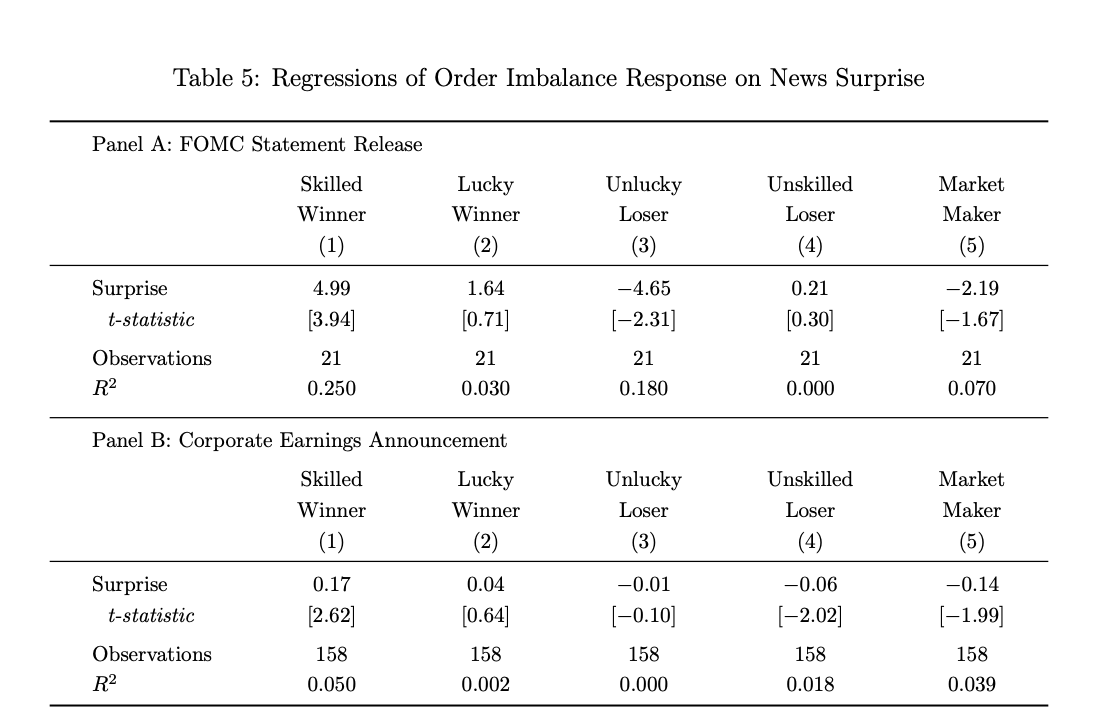

To minimize errors caused by news transmission time, researchers selected two types of events with clear information release timings as research samples: FOMC rate decisions and corporate earnings announcements (Odaily Planet Daily Note: the former is central to monetary policy expectations; the latter is core to understanding a company's fundamentals).

Research data shows that only the order flow of skilled winners significantly shifts in the unexpected direction within a short window after news announcements.

In the FOMC betting events, for each 1% increase in unexpected direction, the net buying amount of skilled winners increases by about 5% (t=3.94); since the unexpected direction amplitude of the FOMC is relatively small (maximum about 6 percentage points), thus the reverse buying amplitude is quite large. For earnings announcements, each 1% increase in unexpected direction corresponds to approximately a 17 basis point increase in the net buying of skilled winners (t=2.62). In contrast, all other groups show no consistent reaction to news, with some even taking opposite trading directions.

Truth Eight: Market maker profits come from liquidity spreads, not information differentials

Research data indicate that market makers on Polymarket only account for 0.1% of total accounts (about 1,660), but they participate in an average of 942 betting markets, with an average profit of $11,832 per account.

Moreover, their order flow can predict price changes in the short term (because they are constantly "taking the market"), but their impact on the prediction of final event outcomes is negative (as per the above Table 3 data: coefficient -5.69, t=-10.30).

This means they are short-term accepting the sell orders of insider traders, but in the long term they are "harvested" by insiders, mainly making money through spreads rather than directional predictions.

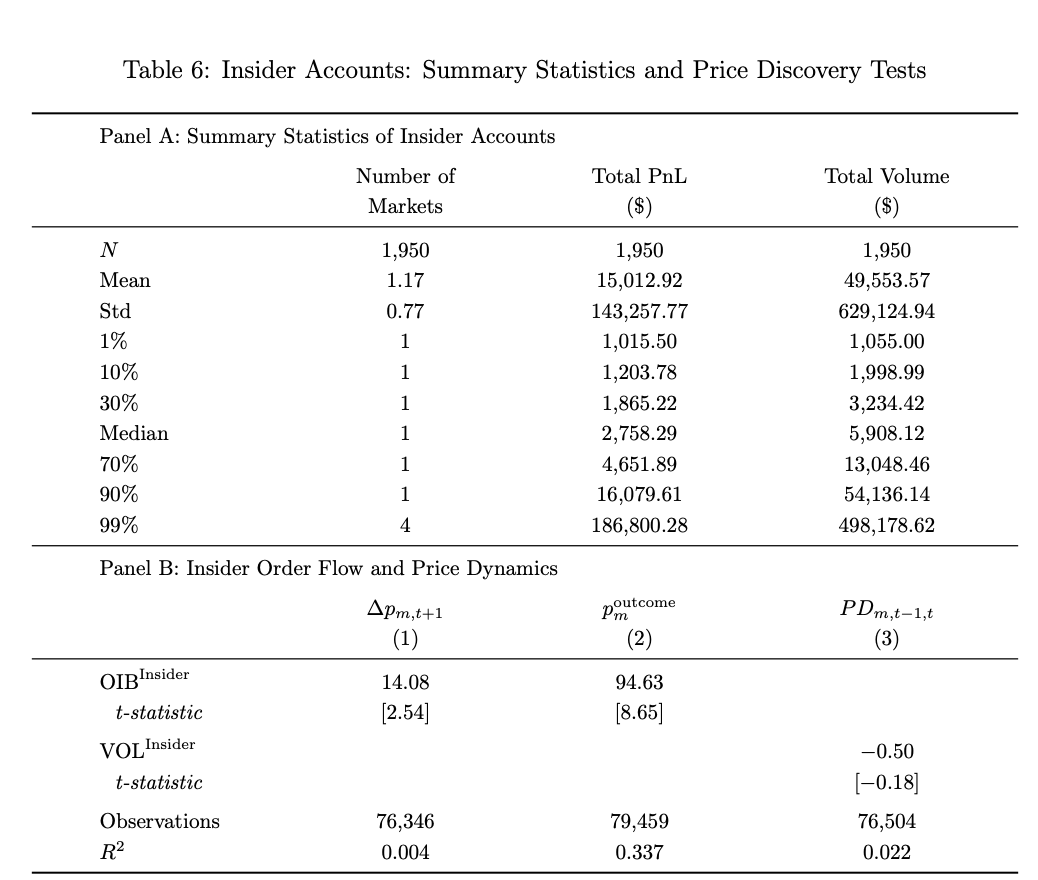

Truth Nine: Insider trading only affects a few event outcomes

Considering the unavoidable nature of insider trading in prediction markets, this study also analyzed the data on the impact of insider trading on price discovery. (Odaily Planet Daily Note: this study used two criteria to mark suspicious trades. The first is timing, i.e., accounts that open trades shortly before a specific event, such as 7 days, and stop trading after the event settles; the second is belief intensity, i.e., accounts that are concentrated in a single event contract with abnormally large positions, trading volume of at least $1,000 and profit of at least $1,000. Accounts meeting both conditions are classified as insider traders.)

In the paper, about 1,950 suspicious insider trading accounts were identified using "account time characteristics + position concentration" from two dimensions; these accounts had an average profit of $15,000.

Notably, the orders of these accounts have extremely high prediction accuracy for the price and outcomes of certain events (final outcome prediction coefficient of 94.63, which is 12 times that of skilled winners), but they are only concentrated on a few events and do not significantly contribute to the overall price discovery of the prediction market.

It’s worth mentioning that this study has detailed the case of the prediction market for the "U.S. military raid on Maduro": three accounts bet days before the operation, concentrating on buying the event with a probability of occurrence of only 10%, ultimately earning more than $630,000 in total—one of the account holders was later charged by the CFTC as an active duty U.S. military member. Details can be read in“After 4 months, Polymarket helped Trump catch the leaker of military operations, but the cost was…”

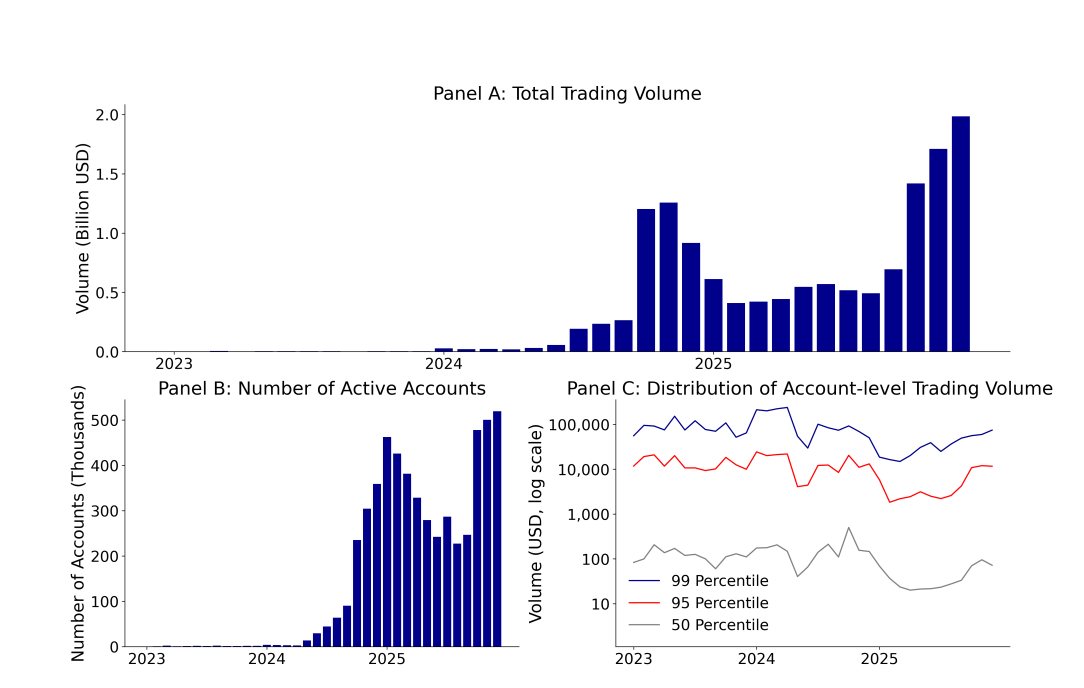

Truth Ten: The trading distribution in prediction markets is extremely unequal, akin to the power law

As of December 2025, Polymarket's transaction volume grew from $3.3 million in December 2023 to $1.98 billion, an increase of over 600 times within two years; during the same period, its monthly active accounts surged from 1,600 to over 519,000.

While its operation data is impressive, the truth behind the data is even more counterintuitive—on Polymarket, the median active account's average transaction volume is only $72, while the average transaction volume for the top 1% of accounts is $74,000, a difference exceeding 1000 times.

From the overall transaction volume perspective, as of December 2025, Polymarket's total transaction amount reached $13.76 billion across 1.72 million accounts, but the lucky losers and skilled losers two groups accounted for 67% of the accounts, contributing 39% of the transaction volume, and bearing 100% of the losses.

There is no doubt that this is not a fair market of "everyone is equal, concentrating collective wisdom," but rather a zero-sum game ecology where a minority sets prices while the majority provides capital and bears losses.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。