The "delivery" of cryptocurrency to fiat is far from as simple as it seems.

Written by: Lisk

Translated by: Eric, Foresight News

Stablecoin channels have indeed significantly improved the cross-border aspects of international payments. However, the part that consistently faces issues is the final delivery of funds to local accounts and wallets.

The value of stablecoins in cross-border payments has been widely recognized and has essentially been validated at the wholesale level. Transferring value from one country to another using USDC or USDT is faster than traditional correspondent banking chains, cheaper than most traditional wire transfers, and available around the clock. For the “intermediate segment” of cross-border payments—the part that crosses borders—stablecoins represent a real infrastructure advancement.

The unresolved issue is the last mile. Reliably and at scale converting settled stablecoin balances into local fiat according to local regulatory requirements, and sending them to the correct bank accounts or mobile money wallets—this is where most of the friction, cost, and failures in cross-border crypto payments truly concentrate. Stablecoin channels shorten the distance between countries, while the last mile represents the distance between stablecoins and the people who genuinely need this money; it remains the hardest part to build within the entire technology stack.

What Exactly is the Last Mile

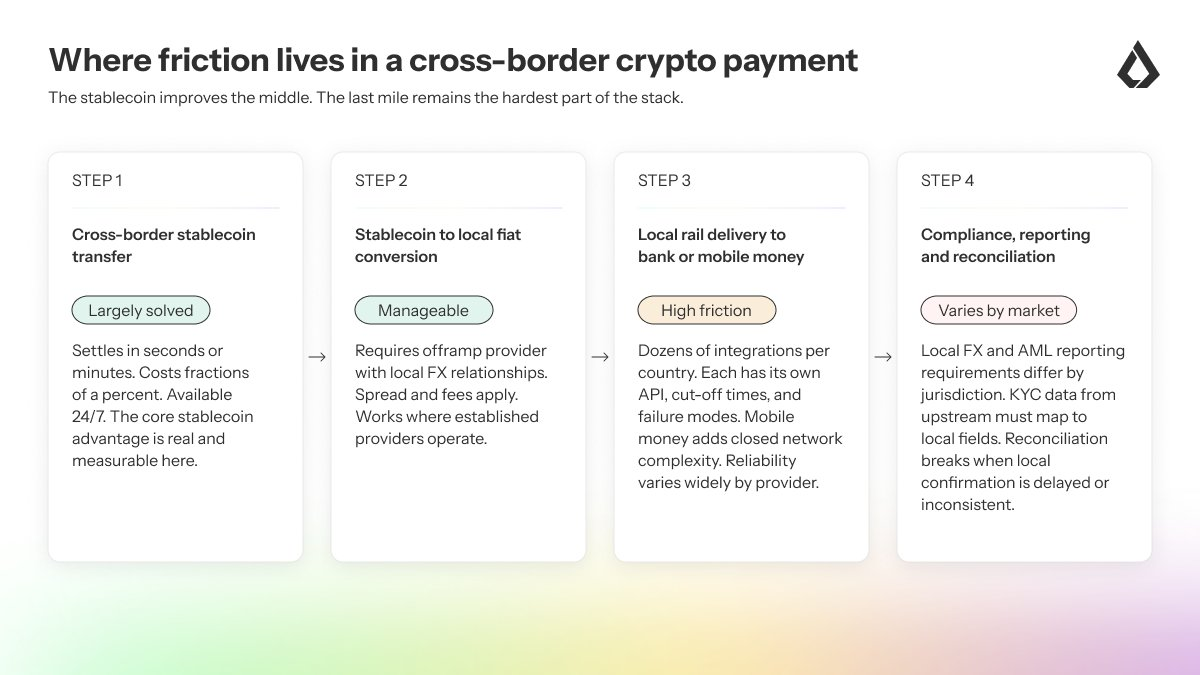

The last mile of cross-border crypto payments consists of four steps, the first three of which have essentially been resolved.

- The stablecoin transfer arrives at the service provider's wallet after cross-border settlement—this step is fast and cheap.

- The provider needs to convert the stablecoins into local fiat, often through local forex partners or internal reserves—this step involves costs and spreads, but is operationally manageable in most channels.

- Then, the fiat needs to be sent to local payment channels: Real-Time Gross Settlement systems (RTGS), Automated Clearing Houses (ACH), instant payment networks, or mobile money platforms—this is where reliability issues start to surface.

- Finally, payments need to be reconciled, reported, and in many jurisdictions regarded as regulated cross-border or forex inflows—this step adds compliance overheads, and differences between markets can be significant.

Friction does not accumulate evenly across these steps. Where offshore exchange providers have built stable relationships with local banks and forex partners, conversions and liquidity are manageable. The integration of local payment channels is where reliability issues emerge: every country has multiple banks, various mobile money operators, different technical APIs, different cutoff times, and different error-handling mechanisms. A provider serving ten markets must maintain and monitor dozens of independent integrations, each of which could potentially fail independently. Compliance and data requirements add another layer of complexity: the KYC (Know Your Customer) and KYB (Know Your Business) data collected upstream in the payment chain must be converted into local reporting fields, thresholds, and document requirements, which vary across jurisdictions. Reconciliation—matching stablecoin settlement records with local disbursement confirmations—is theoretically straightforward but operationally difficult in practice, especially when local payment confirmations are delayed or arrive in incompatible formats.

Stablecoins solve the "distance" problem, while the last mile addresses the "delivery" problem. These are two different issues that require different infrastructures.

The Problem of Fragmentation in Withdrawals

The last mile relies on local withdrawal providers—those companies that convert stablecoins into local fiat and send them to local banks and mobile money channels. In most emerging markets, this area is highly fragmented, with varying quality and susceptibility to shocks.

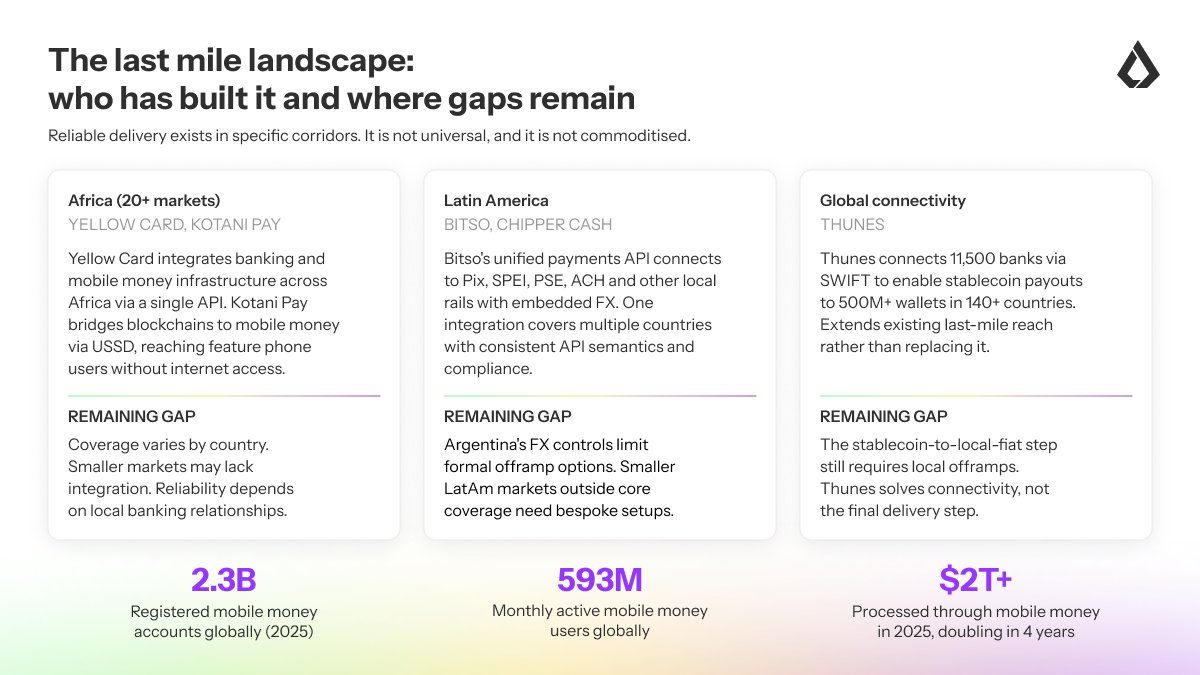

In Africa, Yellow Card has built a pan-African stablecoin channel covering over twenty markets, integrating banking and mobile money infrastructure, positioning itself as an offshore exchange provider for global platforms like Coinbase, Block, and PayPal. Kotani Pay takes a complementary approach: it provides blockchain-to-mobile payment APIs for East and West African markets, utilizing USSD instead of internet connectivity, allowing even feature phone users to receive stablecoin-supported payments without smartphones or bank accounts. These are meaningful infrastructures, but they are not all-encompassing—coverage gaps still exist for specific countries, banks, and mobile money operators.

In Latin America, Bitso's unified payment architecture executes payment collection and disbursement functions across the region's major local payment channels (including Brazil's Pix, Mexico's SPEI, ACH, etc.) through a single API, with embedded forex and stablecoin settlements. This architecture works effectively because Bitso has invested heavily in addressing the trickiest parts: building and maintaining local channel integrations, forex relationships, and compliance infrastructures in each operational market. Building similar capabilities from scratch requires years, not months.

In addition to major providers, there are numerous smaller withdrawal operators serving specific channels, which exhibit significant differences in uptime, liquidity depth, compliance capabilities, and operational terms. When smaller offshore exchange providers experience disruptions—be it due to regulatory uncertainty, liquidity crises, or changes in banking relationships—payments queue up, reconciliation backlogs increase, and operators are forced to manually route to secondary providers, which have different formats, KYC standards, and fees. This risk is not theoretical but a reality faced when relying on infrastructure with no standardized reliability.

Cost data clearly indicates the contribution of the last mile to total payment costs. According to World Bank remittance data for the first quarter of 2025, the global average remittance cost is 6.49%. In Sub-Saharan Africa, the cost is higher—averaging about 8% at the beginning of 2025. The costs of the stablecoin transfer itself may be under 1%. However, when adding forex conversion, local payment fees, mobile money charges, and compliance overheads, many African channels see end-to-end costs climbing back to the range of 7% to 8%. The savings brought by stablecoin channels are real, but a large portion is offset by the last mile.

Mobile Payments and the Last Mile

For hundreds of millions of people in parts of Africa and Asia, mobile payments are not one of several optional channels but the primary financial account. The GSMA's "2026 Industry Status Report" indicates that there are 2.3 billion registered mobile payment accounts globally, with 593 million monthly active users in 2025, processing transaction volumes exceeding $2 trillion—doubling in just four years. Most of these active accounts are located in Sub-Saharan Africa, where mobile payment accounts are often the only viable financial accounts available to a large population.

For businesses making cross-border stablecoin payments to these markets, reaching the recipient usually means reaching their mobile money wallet, not a bank account. This adds a series of specific technical and regulatory challenges on top of the problem of withdrawal fragmentation.

Mobile payment networks are closed systems. M-Pesa, MTN MoMo, Airtel Money, OPay, and Wave each have their own integration patterns, technical APIs, compliance rules, and operational characteristics. A provider wishing to deliver to mobile money wallets across five African countries needs to manage fifteen to twenty independent integrations, each requiring a direct commercial relationship with mobile network operators, ongoing technical maintenance, and real-time monitoring. When Kenya's M-Pesa experiences a failure, all payments in that channel will be affected until the service is restored. By this time, the stablecoin settlement by the provider may have been successfully completed, but the final delivery step that the recipient is waiting for is stuck.

The regulatory aspect further complicates matters. Mobile payment transactions exceeding certain thresholds require KYC verification at the wallet level. In many jurisdictions, cross-border mobile money flows are regarded as forex inflows and trigger reporting requirements. In some markets, the regulatory boundaries governing stablecoin to mobile payment delivery are still being defined, leading to uncertainties about what compliance documents are needed and by whom. Kotani Pay, which integrates directly with mobile money operators via USSD (allowing payments without internet or bank accounts), demonstrates that innovative infrastructure can reach populations that would otherwise be excluded; whereas Chipper Cash’s collaboration with Stable in December 2025 to build stablecoin payment channels in Africa shows that even mature players continue investing to resolve last-mile issues rather than viewing them as a completed task.

What Reliable Last Mile Infrastructure Requires

Companies capable of reliably executing stablecoin cross-border payments at scale share a set of common characteristics that distinguish them from suppliers who operate on a smaller scale but fail to meet enterprise demands.

Single Integration, Multiple Channels: The operational overhead of maintaining dozens of independent integrations is a major reason why last mile infrastructure is expensive and hard to replicate. Abstracting this complexity into a single API behind a provider—providing just one integration point outward, while parsing to multiple local channels internally—creates significant operational leverage for its clients. Thunes’ expansion to support stablecoin payments through SWIFT connecting 11,500 banks, linking over 500 million stablecoin wallets in 140 countries worldwide, exemplifies the application of this principle on a global scale: one connection point corresponding to a vast network beneath.

Deep Local Licensing and Relationships: Technical integration is necessary, but far from sufficient. Reliable last mile delivery requires establishing commercial relationships with local banks and mobile payment operators, gaining regulatory approvals in each market, and creating compliance systems that meet local anti-money laundering and forex requirements. These take years of effort and significant capital to build. New entrants cannot quickly replicate this, which is why reliable last mile providers in most markets are often those companies that invested in regulatory infrastructure before transaction volumes arrived.

Enterprise-Level Operations: The difference between last mile solutions that work well for small-value transactions and those that perform for enterprise-level traffic lies mostly in operations rather than technology. It requires multiple banking partners for redundancy in each channel, the ability to switch seamlessly between different payment channels when one fails, real-time monitoring of payment status across all integrations, and providing predictable contract service level agreements (SLAs). Manual processes that handle hundreds of transactions a day will collapse when the volume reaches tens of thousands daily. The reconciliation layer—from stablecoin receipt, forex conversion to local posting confirmation—must be automated and auditable to support large-scale operations.

The last mile is not a problem with a single technical solution. It is an operational and regulatory issue that requires continuous market-by-market investment in infrastructure, relationships, and compliance.

Why This is Critical for Operators

For companies engaged in cross-border stablecoin payment services, the last mile issue is far from an abstract concept. It directly affects which channels you can reliably serve, what your actual end-to-end costs are, and how your customers experience payment delays.

The practical implication is this: channel selection is not just a business decision about where there is demand, but a decision about where reliable last mile delivery infrastructure exists. If a channel's stablecoin settlement is quick and cheap, but local offshore exchanges are highly fragmented, capacity-limited, or regulatory uncertain, then the payment experience for that channel becomes unpredictable. The stablecoin has done its job, but the last mile has not.

For businesses that build payment products rather than just using them, the last mile issue is even more fundamental. Decisions about which local channels to integrate, which offshore partners to rely on, how to handle mobile money deliveries, and how to manage compliance in the payment process are product-level decisions that determine which markets you can serve and what the quality of service will be. Those providers who have already solved this issue—like Yellow Card in Africa, Bitso in Latin America, and Thunes globally—have achieved this through sustained investment in these decisions over many years. Stablecoin channels are becoming a commodity, while last mile infrastructure is far from it.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。