Original |Odaily Planet Daily(@OdailyChina)

Author|Golem(@web3_golem)

On May 8, Coinbase announced its Q1 financial report for 2026. Coinbase CEO Brian Armstrong summarized the quarter on the earnings call, stating, "Faced with a sluggish cryptocurrency trading market, Coinbase still performed excellently within a controllable range."

In the earnings report PPT, Coinbase highlighted achievements made in Q1, such as the cryptocurrency trading market share rising to 8.6%, a historic high; derivatives trading volume TTM (trailing twelve months) increasing 169% year-on-year; projected market annualized revenue reaching $100 million in March (only two months after launch); and twelve products with annual revenue exceeding $100 million.

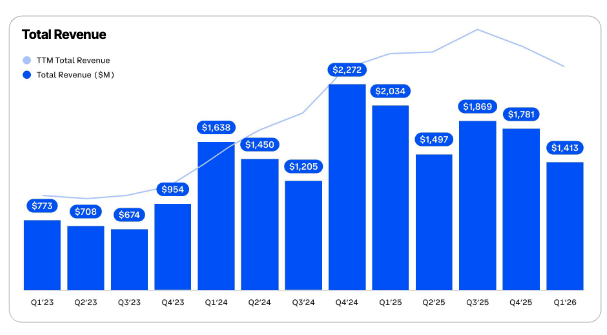

However, no matter how impressive the PPT, it cannot obscure the dismal core financial data of Coinbase for Q1. The report shows that Q1 2026 total revenue for Coinbase was $1.41 billion, a 31% year-on-year decline and a 21% quarter-on-quarter decline, falling short of market expectations, with a net loss of $394.1 million. Coinbase has recorded net losses for two consecutive quarters (Odaily Note: Q4 2025 net loss was $666.7 million).

As a result, Coinbase (NASDAQ: COIN) fell over 5% during trading on May 8, but today it recovered all losses, closing at $201.16.

Is the weakness in the crypto market the only reason for Coinbase's losses?

The drop in stock prices following the earnings report reflects market concerns about Coinbase's short-term performance, while Coinbase attributes the primary reason for its losses to the weak crypto market. Since Q3 2025, Coinbase's revenue has started to decline, and the overall trend of quarterly revenue aligns with the cryptocurrency market transitioning from a bull to a bear cycle.

Coinbase Quarterly Revenue

However, is market weakness the only reason for Coinbase's losses? What other potential issues can we uncover from the financial report?

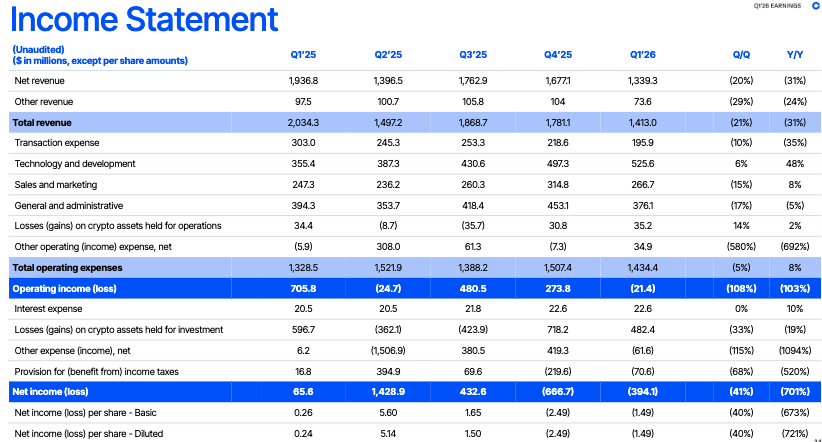

Some analysts believe that Coinbase's Q1 net loss is affected by impairments on its owned crypto assets. The financial report also indicates that digital assets held for investment purposes resulted in a loss of $482 million. However, upon reviewing Coinbase's Q1 income statement, it can be seen that even excluding these non-operating expenses, Coinbase’s operating income for Q1 2026 was negative, with a loss of $21.4 million.

Moreover, in Q4 2025, similarly impacted by the overall decline in the crypto market and sluggish trading, Coinbase’s impairment on crypto assets reached as high as $718.2 million, leading to a final net loss of $666.7 million, but Coinbase still reported positive operating income that quarter, reaching $273.8 million.

Coinbase Q1 Income Statement

This indicates that although the weakness in the crypto market has impacted Coinbase's net profits, Coinbase's performance is not as robust and controllable as Brian Armstrong described.

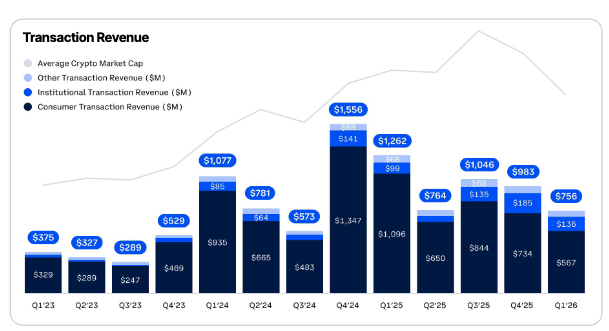

The problem lies in Coinbase's main source of revenue, its brokerage business, which provides digital asset trading intermediary services for retail and institutional clients. The Q1 2026 report shows that Coinbase’s trading revenue reached $756 million, of which retail contributed $567 million, down 48.2% year-on-year and 23% quarter-on-quarter, bringing retail trading revenue back to 2024 levels.

Coinbase Quarterly Trading Revenue

This actually reflects a potential threat that Coinbase is facing: users have started to leave amid the declining crypto market.

Investors should not be misled by the historic high market share of cryptocurrency trading volume in Coinbase's earnings report PPT, as this encompasses derivatives and prediction markets among other products, and not just the spot market. According to Coinbase CFO Alesia Haas, these new products have not been included in trading revenue (but are still part of total revenue).

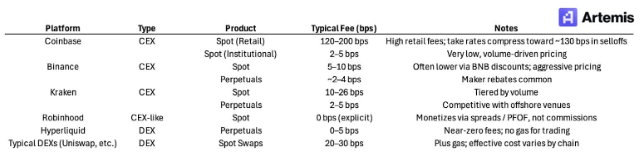

Coinbase's core competitiveness lies in its compliance in the United States; thus, the trading fees Coinbase has historically charged have been significantly higher than most global exchanges, which is meant to cover the high compliance costs and also to charge a premium to users after Coinbase's early "monopoly in the U.S. crypto market." However, the regulatory landscape in the U.S. has drastically changed, and Coinbase’s compliance is no longer a decisive advantage as more than ten exchanges have obtained licenses to offer crypto trading services to U.S. users, such as Robinhood, Kraken, and Binance.US.

These emerging competitors, without exception, charge lower fees than Coinbase and use this as one of the main competitive strategies to attract retail users.

Fee Ratios Charged by Different Exchanges

For U.S. retail investors, in the early days of the crypto market, they might have been willing to pay an extra fee to Coinbase for convenience, trust, and regulatory certainty. But as crypto regulations mature and the market declines, retail investors will naturally opt for platforms with lower fees, especially after traditional brokers and financial institutions like Robinhood have entered the cryptocurrency space.

In response to fee issues, Brian Armstrong also commented on the earnings call, stating, “Customers choose us not because we have the lowest fees, but because we can offer products that meet their needs.” Although Coinbase One has more than one million paid users, if it comes to comparing the richness of cryptocurrency tokens and the speed of listing, the rise of DEXs like Hyperliquid will also pose significant pressure on Coinbase and other CEXs.

Recently, Coinbase announced a 14% workforce reduction, leaving approximately 4,300 employees (down from 4,988 at the end of Q1). Brian Armstrong attributed the layoffs to market downturns and the AI technology revolution. However, the real revenue situation revealed by Q1's financial report has confirmed that this is just a cost-cutting initiative dressed as an AI revolution. (Related reading:Coinbase Layoffs 14%, What is the main cause, the bear market or AI?)

While making grand promises, it relies on Circle for survival

Facing challenges such as the sluggish crypto market, declining spot trading, and user churn, Coinbase is also seeking a way out. Brian Armstrong mentioned during the earnings call that Coinbase is moving away from reliance on spot trading, transitioning from a "spot-focused cryptocurrency platform" to a platform where users can trade a broader range of asset classes, including derivatives, stocks, commodities, and prediction market contracts, referred to as the "Everything Exchange."

These products were launched at the beginning of 2026. According to Coinbase, retail market derivatives have generated an annualized revenue of over $200 million, with prediction markets generating an annualized revenue of over $100 million. Coinbase CFO Alesia Haas stated that the revenues from these new products are not included in the trading revenue and subscription revenue; if assuming all other revenue is generated by these new products, then the real situation in the financial report is that these new products generated a maximum total revenue of $73.6 million in Q1.

At the same time, Coinbase is also deliberately "blurring" the profits generated by Base. Brian Armstrong claimed that Base processed 62% of the global on-chain stablecoin trading volume, with over 90% of on-chain stablecoin trading occurring on Base, yet Coinbase did not separately disclose the revenue generated by Base in the report. After a careful examination of the report, it seems that Coinbase either did not disclose the true revenue of Base or mixed it into the report under "Other subscription and services revenue," a category where Coinbase has commonly included on-chain revenues in previous quarters, and for Q1 2026, this item generated only $109.4 million.

Base's on-chain fee income over the past 30 days is $2.72 million (Source: DeFiLlama)

In summary, it appears that Coinbase is attempting to paint a grand narrative using long-term stories about derivatives, prediction markets, AI, and on-chain to divert market attention from its main business struggles, but whether these areas will ultimately become Coinbase's new "cash cows" remains to be seen. Expanding product lines too broadly in pursuit of market hotspots may provide more stories to tell the market, but it could also lead to significant setbacks if not handled carefully.

However, Coinbase has the capital for trial and error, as it still has its "good brother" Circle to sustain it.

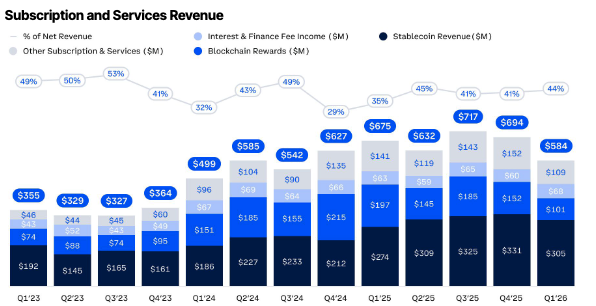

Q1 earnings report shows that Coinbase's stablecoin revenue reached $305 million in Q1 2026, a year-on-year increase of 10%, making stablecoin revenue Coinbase's second-largest source of income (Odaily Note: The primary source of income is retail trading revenue, and their combined share is 62% of total income.)

Coinbase Q1 Subscription and Service Revenue

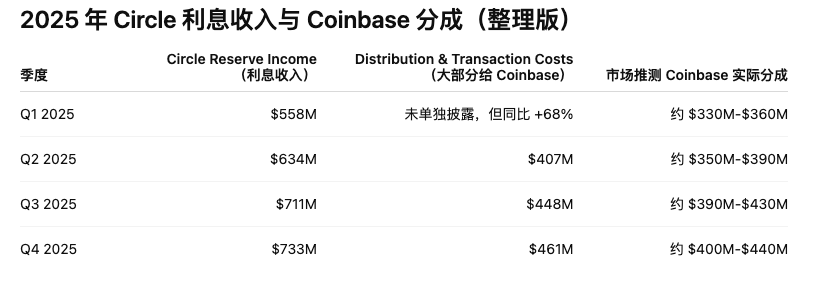

This substantial revenue is primarily due to the revenue-sharing agreement with Circle. Under the agreement signed in August 2023, Coinbase receives all interest income generated from USDC on its platform, while interest income generated from USDC outside the platform is split 50/50 between Coinbase and Circle. During the Q1 2026 earnings call, Alesia Haas emphasized that the distribution contract between Coinbase and Circle automatically renews every three years and is never terminated.

This structure positions Coinbase as a toll gate for USDC, and in the future, stablecoin income is highly likely to become Coinbase's primary source of income. On one hand, the USDC accumulated in Coinbase's platform and products is continuously increasing. According to the financial report, over 25% of the circulating USDC is stored on Coinbase (an average of about $19 billion in USDC held in Coinbase products); on the other hand, as stablecoins become mainstream, Circle's interest income is also increasing. As seen in the chart, Circle's interest income grew from $558 million in Q1 2025 to $733 million by year-end.

On May 11, Circle will officially release its Q1 2026 financial report, allowing investors to examine Circle's interest income and Coinbase's distributed profits for that quarter.

However, Coinbase has indeed made significant contributions to the distribution of USDC. In addition to conventional channels, Coinbase has also been actively promoting USDC in the fields of AI and agent payments (A2A). According to the financial report, Coinbase's x402 protocol (Note: now managed by the Linux Foundation) has processed over 100 million payments, with over 99% of x402 transactions completed using USDC. Coinbase estimates that by 2030, AI Agents will process between $30 trillion to $50 trillion in transactions, and cryptocurrencies will become the preferred native execution channel for Agents. If USDC dominates the settlement of Agent transactions, it would also create significant economic value for Coinbase.

Therefore, if the distribution agreement between Coinbase and Circle is indeed perpetual, Coinbase has effectively tied itself to this "printing press" of USDC. As long as the global stablecoin market continues to grow, and USDC keeps expanding in payments, AI Agents, cross-border settlements, and internet finance, Coinbase will consistently extract profits. To some extent, this may yield even higher and more stable returns than Coinbase's current exchange business and the revenue generated from various new products.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。