Author: Shenchao TechFlow

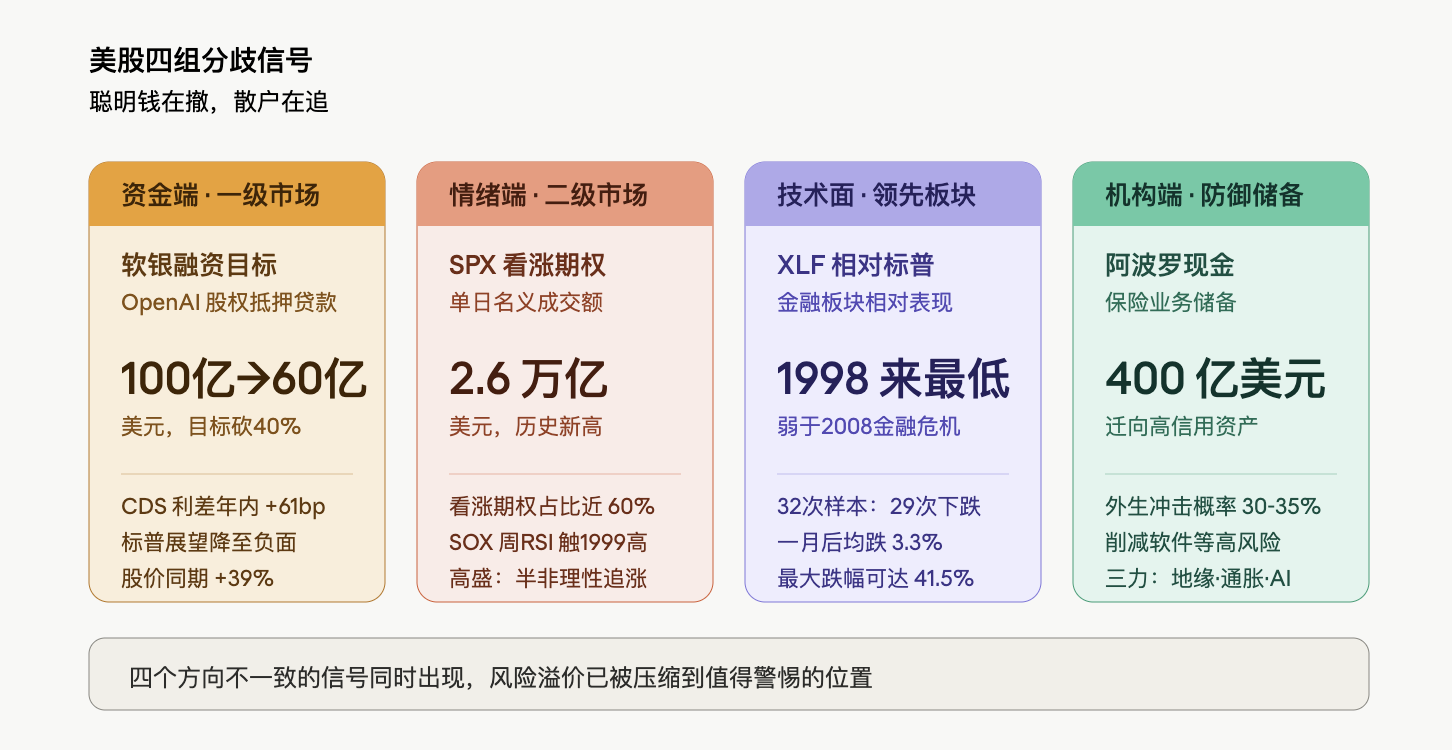

The U.S. stock market is displaying a highly unusual divergence: while the S&P 500 continues to hit new highs, the financial sector has cumulatively fallen 6% this year, underperforming relative to the market during the 2008 financial crisis and the COVID-19 impact; meanwhile, the nominal trading volume of S&P 500 call options surpassed $2.6 trillion in a single day, setting a record, while the RSI of the Philadelphia Semiconductor Index reached its highest level since 1999. In the primary market, SoftBank’s financing plan backed by OpenAI equity has been forced to lower its target scale from $10 billion to $6 billion; on the institutional side, Apollo has reserved approximately $40 billion in cash within its insurance business. Smart money is withdrawing, while retail investors are chasing.

The narrative around the scarcity of AI computing power continues to drive the U.S. tech sector upward, but the funding situation, sentiment, technical indicators, and institutional behavior are all sending inconsistent signals. This divergence itself is worth examining more than any single piece of data.

Lenders doubtful about OpenAI's valuation, SoftBank cuts financing target by 40%

According to Bloomberg citing insiders, SoftBank has reduced the target size of its margin loan backed by OpenAI equity from $10 billion to a minimum of $6 billion, representing a 40% cut. The core of the resistance lies in valuation, as some investors who were persuaded to participate have doubts about how to determine a reasonable value for OpenAI, a private company. Potential lenders involved in discussions include private credit firms, financial institutions, and hedge funds, with discussions starting as early as mid-March.

OpenAI’s own fundamentals are also under pressure. The company has repeatedly failed to meet its monthly sales targets in early 2026, while competitor Anthropic continues to erode its share in programming and enterprise markets; the internal target of reaching 1 billion weekly active users for ChatGPT by the end of last year was also not achieved. OpenAI's Chief Financial Officer Sarah Friar refuted this, stating that the company is meeting its various goals and seeing product demand showing "vertical growth."

SoftBank's own financial leverage is also at a historical high. The group has recently committed an additional $30 billion to OpenAI, having already invested over $30 billion; the $40 billion loan completed in March set a record for their dollar loan size, with some funds used to support the latest follow-on investment in OpenAI.

Capital market judgments on SoftBank have shown significant divergence. SoftBank's stock price has risen 39% this year, significantly outperforming Japan's benchmark TOPIX, which has risen 12.3%; however, its credit default swap spreads have widened by about 61 basis points this year. In March, S&P Global Ratings downgraded SoftBank's credit outlook from "stable" to "negative," citing that the investment in OpenAI could harm the company's liquidity and asset credit quality.

The pricing disparity in the primary market for leading AI assets is most directly reflected: lenders are willing to lend 40% less than what SoftBank wants to borrow.

Options market sees $2.6 trillion in a single day, Goldman Sachs partner calls it "semi-irrational"

The secondary market presents a different picture. On Thursday, the nominal trading volume of S&P 500 call options exceeded $2.6 trillion, setting a historical record, with nearly 60% of all SPX options that day being call options. Rich Privorotsky, head of Goldman Sachs’ One-Delta trading desk, characterized the current U.S. stock market as a "buying on rising spot market and rising volatility" model.

The RSI of the Philadelphia Semiconductor Index (SOX) has risen to its highest level since 1999. A Goldman Sachs partner remarked: "It feels like we are in a semi-irrational buying phase." Privorotsky cited 1999 as a more apt historical analogy, when telecommunications equipment suppliers were overwhelmed with orders, providing support for that cycle's growth narrative, which is highly similar to the current discourse surrounding the scarcity of computing power and the deployment of AI infrastructure.

The implied volatility of QQQ has sharply risen with the market, and its difference from SPX volatility has expanded to over 6 volatility points. Goldman’s volatility trading desk described that day as "one of the craziest trading days in recent weeks." Notably, the number of stocks in the S&P 500 that experienced movements exceeding 3 standard deviations in a single day reached 35, the highest level since February 3 of this year.

Bank of America’s global equity derivatives research team also pointed out that the latest record rise of the S&P 500 evokes memories of the late 1920s and the internet bubble of the 1990s, but the market's pricing of "tail options" remains below the implied level of realized volatility. Simply put, the market is chasing higher prices but unwilling to pay for downside risks.

Goldman warns that the dynamic of "rising spot market and rising volatility" has limited the space for systematic strategies to further increase their positions. Commodity trading advisors (CTAs) have essentially returned to full long positions, while the marginal incremental demand for volatility control strategies is weakening as realized volatility in the upward direction increases. In other words, the programmed buying from the institutional side is nearing its limit, and subsequent upward momentum will increasingly rely on retail and sentiment-driven capital.

XLF weakest relative to S&P 500 since 1998, financial stocks sound alarm

If the options market represents an extreme reading of sentiment, then the relative performance of the financial sector is a technical warning signal.

This year, the U.S. financial sector has cumulatively fallen about 6%, while the S&P 500 index has risen 7% during the same period, closing at historical highs 14 times in the past 17 trading days.

Relevant data is analyzed in "Cracks Behind the New Highs of the S&P 500: Financial Sector Falls 6% This Year, $2 Trillion Private Credit Underflow Is Spreading".

The financial sector is considered a leading indicator due to its core role as a provider of economic liquidity. Concerns regarding the private credit market are believed to be one of the important reasons for the pressure on the financial sector. Melissa Brown, head of global investment decision-making research at SimCorp, noted that the financial system is highly interconnected, and the related risks "could spread more widely than currently expected." She suggested that investors might consider gradually "reducing holdings in chip stocks" instead of continuing to chase prices, and it would be inappropriate to inject new funds into the market.

Apollo reserves $40 billion in cash, Rowan estimates probability of external shocks at 35%

Defensive measures from the institutional side have already begun. Apollo Global Management CEO Marc Rowan stated during the company’s earnings release that he estimates the probability of external shocks at between 30% and 35%, significantly above typical levels.

Rowan attributes this risk to the convergence of three forces: a complete reset of geopolitics, inflationary pressures driven by trade tariffs and immigration policies, and AI's profound reconstruction of the economic structure. He characterizes the current AI wave as "without a doubt the largest technology cycle of his career," specifically highlighting the vulnerability of government finance—compared to businesses and consumers, the government’s balance sheet is under pressure.

Apollo has taken a series of defensive measures: migrating its fixed income portfolio to higher credit quality, reducing exposure to high-risk sectors like software, and reserving approximately $40 billion in cash within its insurance business. "This means we are focusing on protecting capital when investing, ensuring we can navigate the cycle, and we candidly expect that adjustments will occur," he stated.

Rowan reserved his sharpest criticisms for competing firms, warning that not all insurance companies are operating as they should, with some relying on what he calls "outrageous" practices, including offshore structures in the Cayman Islands, complex mortgage arrangements, and aggressive credit assumptions, making some balance sheets appear more robust than they actually are. "We are indeed concerned about contagion," he said.

Notably, Apollo's quarterly performance has been impressive, with assets under management exceeding $1 trillion and fee-related revenues reaching historic highs. Choosing to adopt significant defensive measures at a time of optimal operating performance is a judgment in itself.

Consumer sector shows stark contrast, confirming macro differentiation

Consumer data provide micro-validation for the aforementioned macro judgments. Whirlpool (WHR) plummeted 16% after hours on Thursday, with management describing the current environment as "macro conditions deteriorating sharply" and announcing "decisive measures" such as price increases and accelerated cost reductions to restore profitability. The chill in housing and major consumer goods starkly contrasts with the heat in the semiconductor sector.

In contrast, DoorDash reported a "strong start" to the second quarter, with demand remaining "quite strong," resulting in a stock price increase of about 10%.

This differentiation reflects a deeper logic in current consumer behavior: large expenditures (such as remodeling and appliances) feel as if they are experiencing a recession, while small immediate purchases (like takeout) are nearly unaffected. Consumers have not vanished; they are simply becoming highly discerning, which aligns closely with the conclusions from the business side: AI infrastructure investment is accelerating, while traditional durable goods consumption is shrinking.

Putting the above four groups of signals together: lenders unwilling to offer $10 billion for OpenAI, the options market betting $2.6 trillion on rising prices in a single day, the financial sector falling to the weakest relative level since 1998, and Apollo hoarding $40 billion in cash. This does not constitute a judgment of "imminent collapse," as Scott Brown himself emphasizes, such warning signals can sometimes persist for a long time before being digested by the market, and may even not materialize. However, when the primary market, secondary market, leading sectors, and top institutions all provide inconsistent readings, this at least indicates that the risk premium corresponding to current price levels has been compressed to a level worth monitoring.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。