Circle and Coinbase are looking for a platform that can truly increase the issuance of USDC.

Written by: Eric, Foresight News

USDC is returning to Hyperliquid.

On the evening of May 14, Beijing time, Coinbase, Circle, Hyperliquid, and the deployer of the Hyperliquid native stablecoin USDH, Native Markets, successively issued announcements. This also means that Hyperliquid has abandoned its native stablecoin plan that had been running for 8 months, turning to cooperate with Circle and Coinbase to use USDC as the only settlement asset for the platform.

According to the statement released by Native Markets, Coinbase and Circle acquired the "USDH brand assets", while Native Markets will still operate independently and "focus on its next chapter." Essentially, Coinbase and Circle have converted the "Hyperliquid native stablecoin" from USDH to USDC, so it also requires staking HYPE and sharing the returns generated from USDC reserve assets on Hyperliquid.

This is what Hyperliquid referred to in its announcement as AQA (Aligned Quote Asset) v2. AQAv2 requires Coinbase to stake 500,000 HYPE, responsible for reserve management and ensuring that the returns generated from AQA (i.e., USDC) reserves are shared; Circle also needs to stake 500,000 HYPE to deploy on-chain native USDC, CCTP V2, and other cross-chain infrastructure.

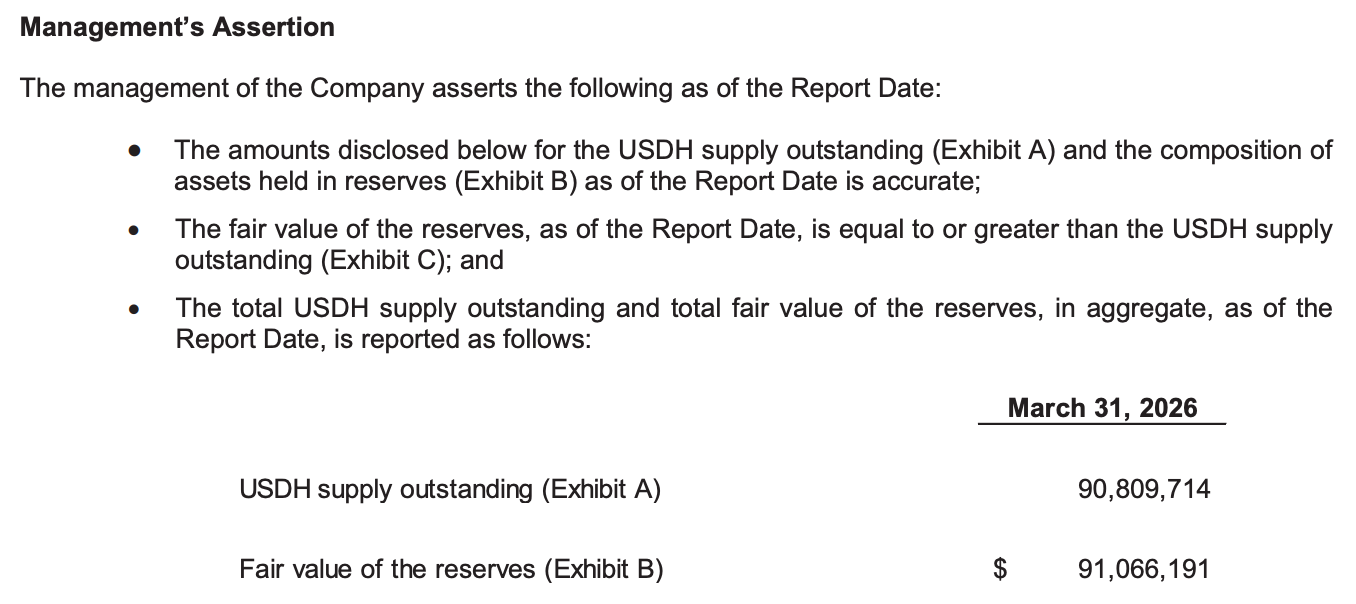

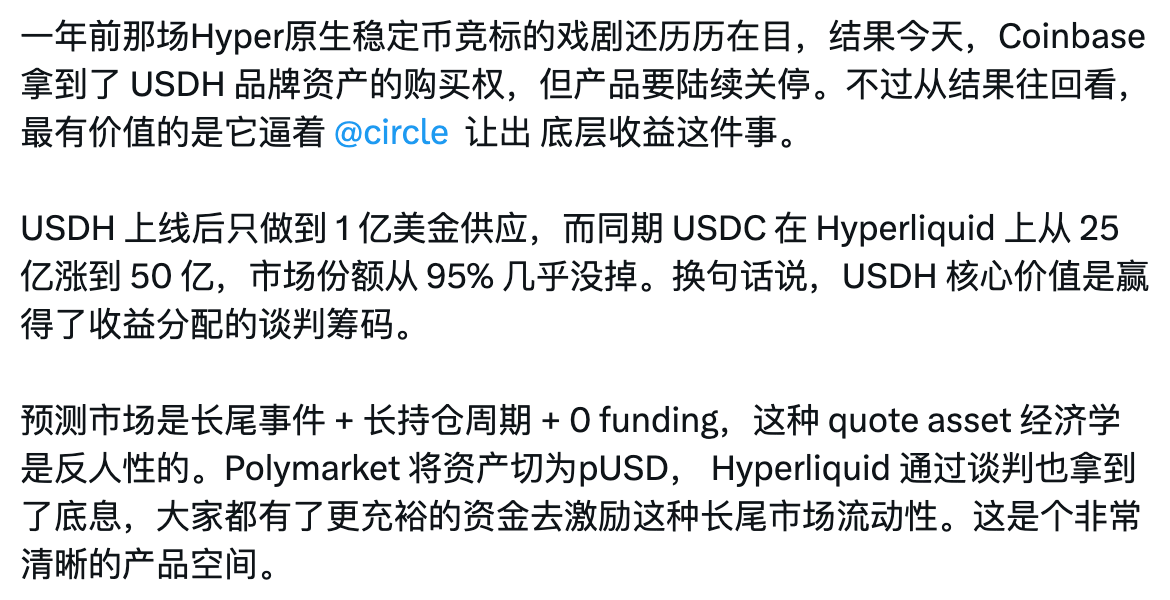

The requirements for profit-sharing in AQAv2 are much higher than in AQAv1. While v1 provided transaction fee discounts for traders using USDH, it only required 50% of reserve profits to be allocated to Hyperliquid; v2 has no fee discounts, but 90% of the profits flow to Hyperliquid. Interestingly, on-chain data shows that the peak circulation of USDH was only around $100 million, and according to the reserve proof document from March this year, as of March 31, the circulation of USDH was only around 90 million.

Meanwhile, the circulation of USDC within the Hyperliquid ecosystem has remained stable at around 5 billion, with the number of switches from USDC to USDH being minimal. Initially, Hyperliquid wanted to keep the issuance rights of stablecoins within the ecosystem, hoping that the ecosystem could share the reserve profits behind the stablecoins and not let such a large ecosystem work for the stablecoin issuer for free.

At that time, entities like Paxos, Frax, Sky (formerly MakerDAO), and Ethena Labs all joined the battle of "who will issue the native stablecoin USDH," ultimately, it was Native Markets, deeply rooted in the Hyperliquid ecosystem, that unexpectedly won the issuance rights. Everyone was calculating who could bring more profits to Hyperliquid, but a question that was overlooked at that time but is now very clear is: who can truly get users to use USDH.

Clearly, Native Markets has failed on the product level, but it might have turned out the same regardless of who was in charge. Many analysts on X pointed out that Native Markets used USDH as a bargaining chip, forcing Coinbase and Circle to not only stake 500,000 HYPE but also to cede 90% of the profits.

This analysis makes sense because even with USDH, the usage of USDC remains unaffected; Circle has no reason to "lose money." However, if the aim is to "pressure" Circle into sharing profits, this reasoning still seems weak.

Last September, during the early stage of the "Battle of the Hundreds," I wrote an article "The Right to Mint USDH Draws Competitors, But Does HyperLiquid Really Need a New Stablecoin?". At the end of the article, I suggested that "even if it loses Hyperliquid, Circle can still choose to support other protocols, and can sacrifice some revenue like with the cooperation with Coinbase in exchange for distribution channels. Perhaps in the short term, the emergence of USDH will bring some pain to Circle, but in the long run, it remains to be seen who is more attractive, Circle's influence and ecosystem coverage effect or the full return of US treasury interest income."

The logic is quite simple: Hyperliquid does not want to put stablecoin profits into its own pocket, but rather wants to promote further development of the ecosystem through profit sharing and token buybacks. For founder Jeff, he might care more about how large Hyperliquid can become. Likewise, I do not believe that the intervention of Coinbase and Circle is the result of "negotiation," but more likely an instance of "actively seeking connections."

Previously, Coinbase and Circle released their Q1 financial reports one after another, both facing some issues with USDC, their flagship product. For Circle, although interest rates are unlikely to return to 0 in the short term, a gradual decline is a trend, and increasing issuance is urgent; for Coinbase, it has experienced continuous increases in the cost of distributing USDC exceeding revenue growth over the past eight quarters, forming an almost irreversible trend, so increasing the issuance of USDC through Coinbase is also urgent.

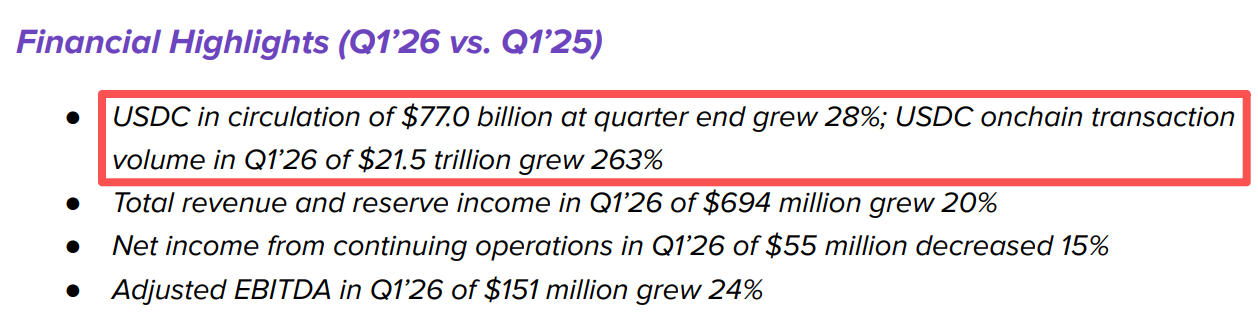

Circle's Q1 financial report showed that the on-chain transaction volume of USDC was approximately $21.5 trillion for the quarter. USDC achieved such a high transaction volume with less than 80 billion in issuance due to its core reason being that in compliant payment and transaction fields, especially everyday consumption, there is simply no need for that much currency.

Therefore, expanding use cases is one aspect, while increasing issuance is another.

According to Robinhood's Q1 financial report, the platform has approximately $45.7 billion in user deposits, and the total assets of the platform (including user-purchased stocks, cryptocurrencies, etc.) reached $345.4 billion. In comparison, this number for Hyperliquid is 5 billion. In my view, Coinbase and Circle's foray into Hyperliquid is more about betting on the future funding growth on the Hyperliquid platform.

If Hyperliquid achieves one-third of Robinhood's scale in the future, the issuance of USDC could already rival the current scale of USDT. More importantly, unlike consumption, trading requires real money to mint USDC into Hyperliquid, which is the real way to improve "issuance." Because if you do not have USDC, you could still use your domestic currency for payments or even barter, but on Hyperliquid, USDC is the only settlement asset.

If that day really comes, whoever uses Hyperliquid will instantaneously achieve "second to none," and instead of praying that day will never come, one might as well bind interests first and leave the rest to time.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。