Altcoins no longer occupy an important position in the future plans of all CEXs.

Written by: Henry Kim, Ryan Yoon

Translated by: Chopper, Foresight News

TL;DR:

- The transaction fee model for cryptocurrency spot trading has peaked; the rise of decentralized perpetual contract exchanges like Hyperliquid, combined with a more lenient regulatory environment after the Trump administration took office, has prompted leading global cryptocurrency exchanges to readjust their development directions.

- Now, major exchanges are laying out plans for stocks, financial derivatives, and other traditional financial products, and their operational models are gradually aligning more closely with traditional financial institutions.

- However, a problem arises: centralized exchanges have always been the core liquidity suppliers of the entire cryptocurrency ecosystem. If exchanges gradually weaken their core cryptocurrency operations, the original operating order of the entire cryptocurrency market may be completely disrupted.

- Cryptocurrency projects thus enter a phase of self-survival; whether they can operate independently without the support of exchanges will become a critical turning point for project development, resulting in clear industry differentiation.

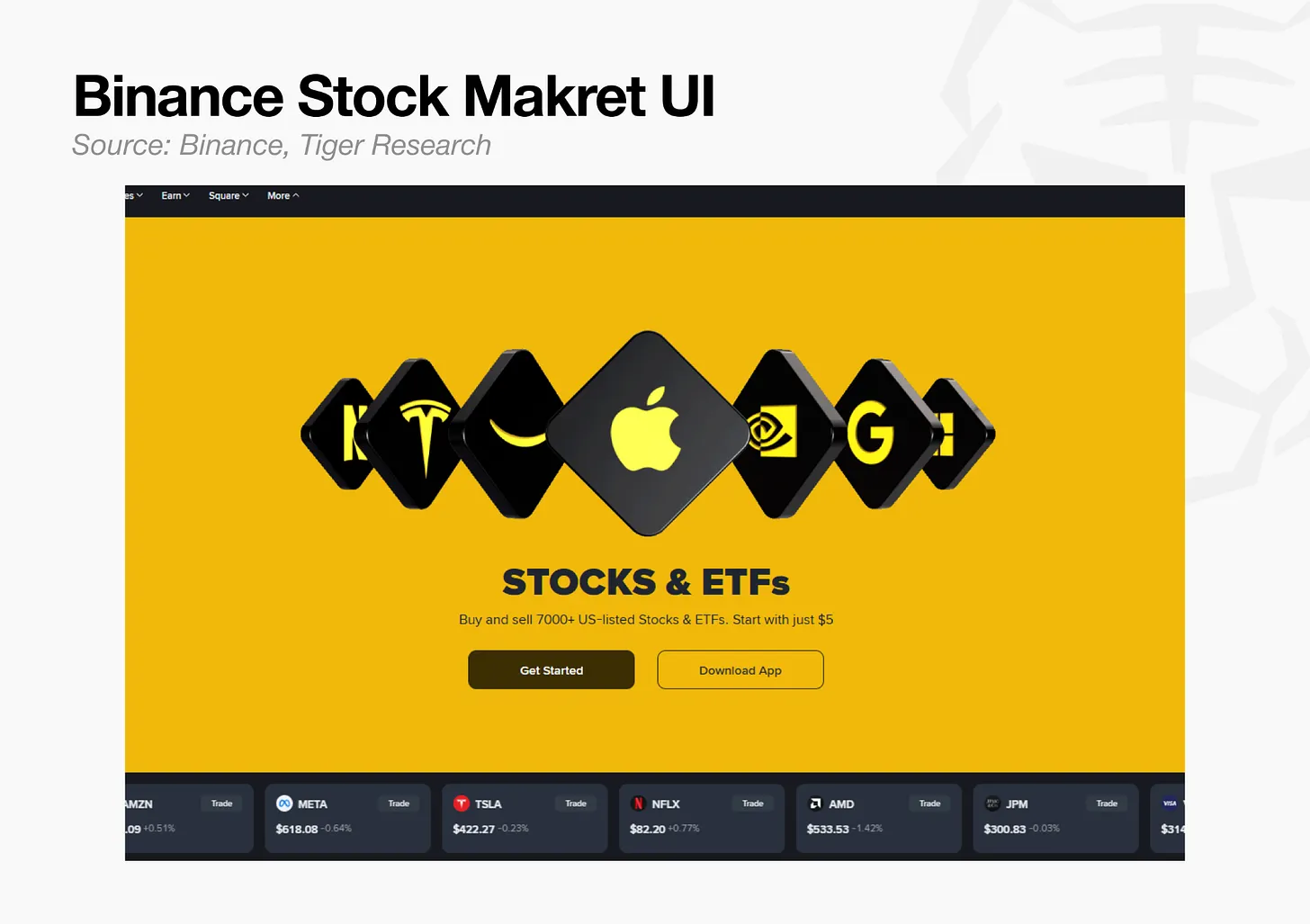

Trading Apple stock on Binance

As of June 1, users can trade Apple (AAPL), Alphabet (GOOGL), and other U.S. stock targets directly through the Binance App. The next day, Binance announced the addition of trading for components of the Korea Composite Stock Price Index, including the three most actively traded South Korean stocks: SK Hynix, Samsung Electronics, and Hyundai Motor.

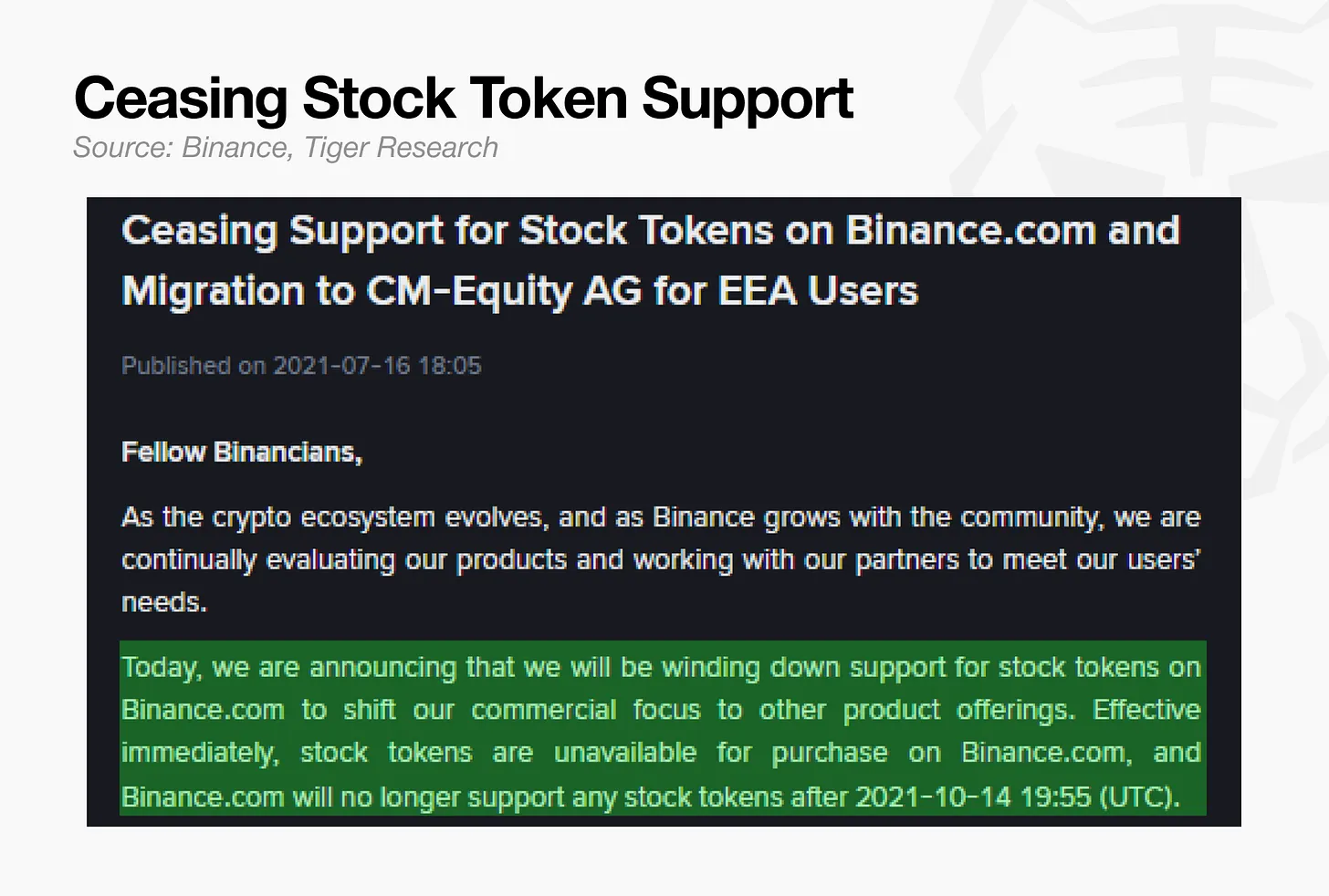

The idea for Binance to venture into stocks can be traced back to 2021. In April of that year, the platform launched tokenized stock trading features, supporting Trading for Tesla (TSLA), Apple (AAPL), Microsoft (MSFT), among others. However, due to ongoing regulatory pressure, the service was completely shut down in July of the same year. At that time, the business was difficult to sustain due to three major structural issues: there was no definitive legal classification of whether stock tokens are securities or derivatives; relevant products did not come with investor prospectuses as required by EU regulations; and Binance lacked the direct qualifications to operate such businesses. Germany's Federal Financial Supervisory Authority, the UK's Financial Conduct Authority, and Hong Kong's Securities and Futures Commission all raised objections based on these issues.

The current relaunch of stock trading services demonstrates significant structural adjustments. Binance now executes orders through a licensed broker in the Abu Dhabi Global Market, with the business clearly defined as securities brokerage services, completely avoiding the previous legal controversies. The core contradiction that halted business in 2021 – the ambiguity over the identity of the underlying asset's issuer – has also largely been resolved.

This industry action shows clear temporal overlap. Meanwhile, Bybit also launched a traditional financial derivatives perpetual contract market, not only launching contracts for South Korean stocks like SK Hynix and Samsung Electronics but also opening trading for Space Exploration Technologies Corp. (SPCX) perpetual contracts. Coinbase followed suit by announcing support for SPCX contract trading.

Leading cryptocurrency exchanges are collectively transitioning at almost the same time, abandoning the single cryptocurrency trading model in favor of comprehensive traditional financial service platforms, and the reasons behind this shift are worth examining.

Three Drivers of Transformation

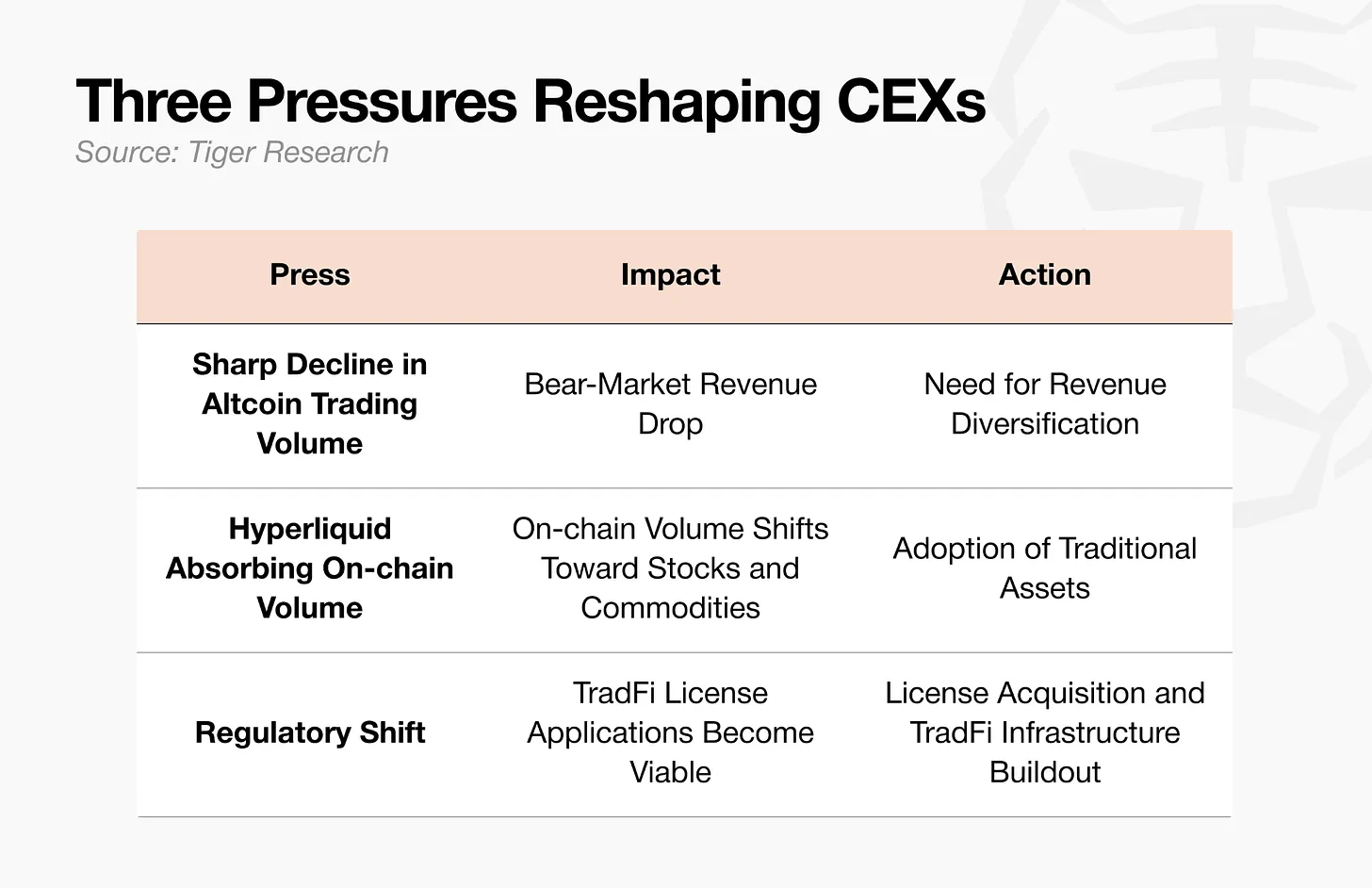

Three external pressures are jointly pushing exchanges to bid farewell to the pure cryptocurrency operational model.

Continual decline in cryptocurrency trading volume

The primary pressure comes from the overall shrinkage of cryptocurrency trading volume. The core source of income for exchanges comes from the trading fees of cryptocurrencies, which are entirely determined by market sentiment.

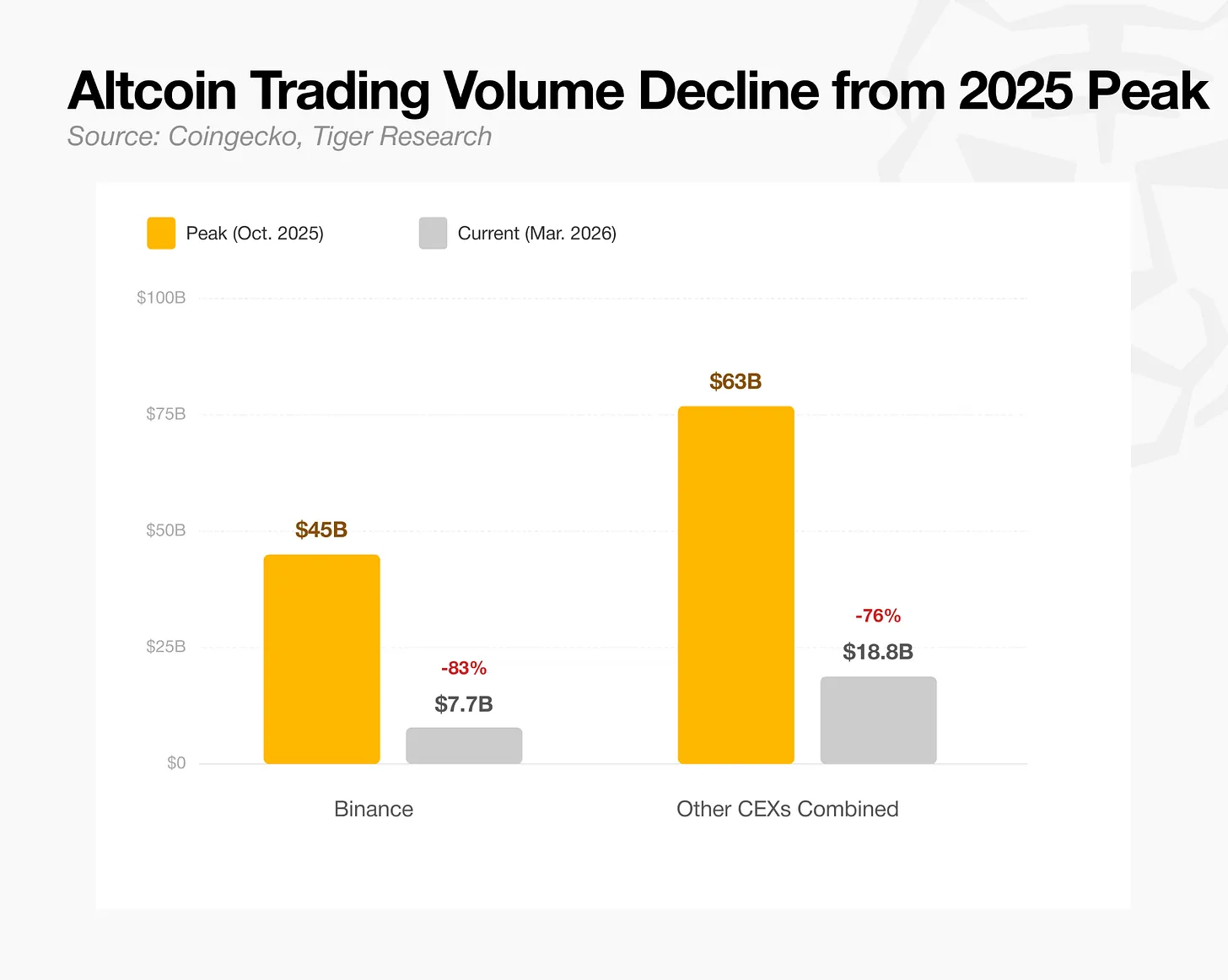

Binance's average daily spot trading volume has sharply fallen from a peak of about $45 billion in October 2025 to just $7.7 billion now, a decline of nearly 80%. The combined spot trading volume of all other centralized exchanges has also dropped from a peak of $63 billion to the current $18.8 billion, a decrease of around 70%. The continuous shrinkage in trading volume means that the business model relying on trading fees is becoming increasingly unsustainable. Major exchanges have long realized that simply relying on cryptocurrency trading fees cannot build a sustainable revenue system.

Hyperliquid diverts on-chain liquidity

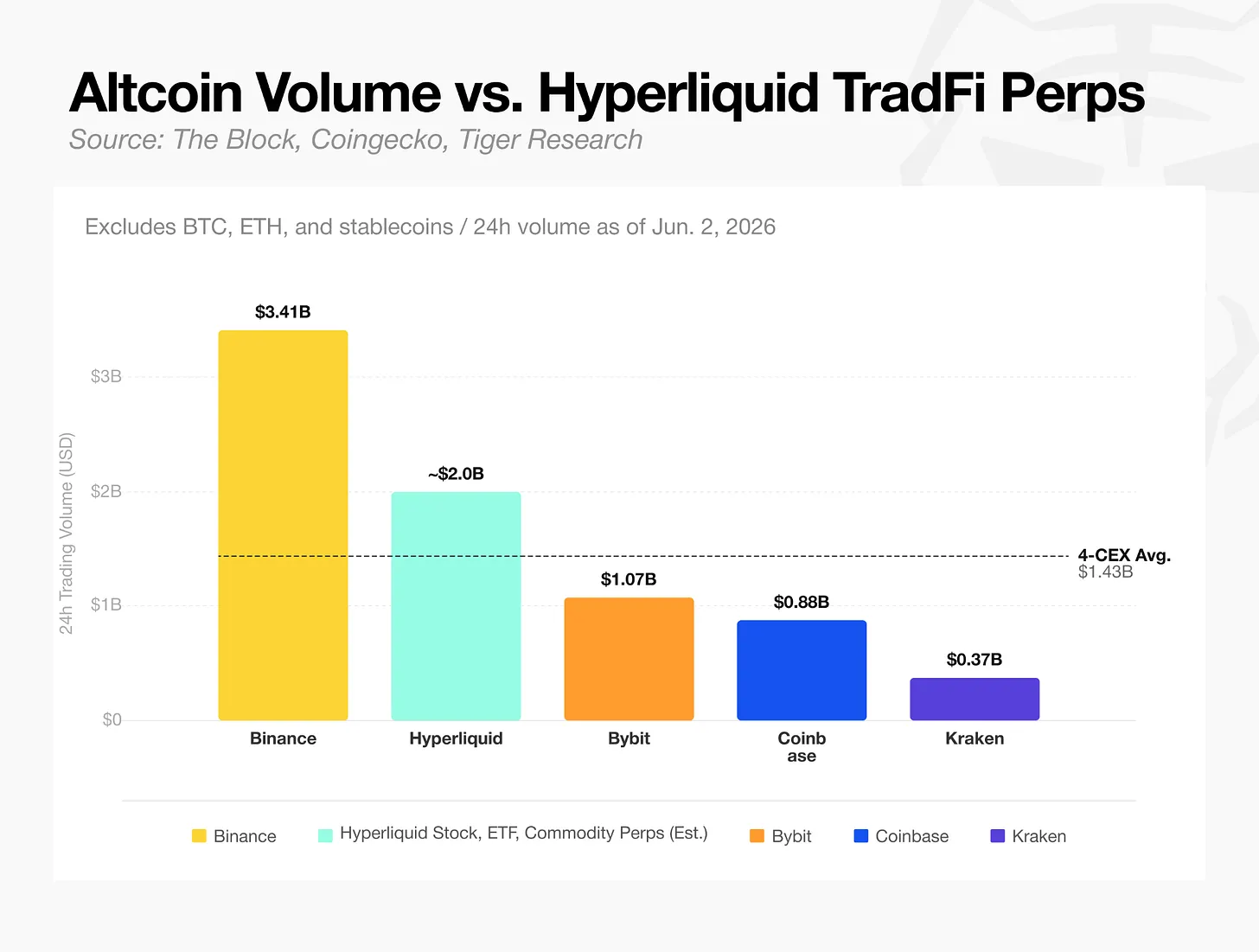

Comparative data clearly shows the current market landscape: comparing the trading volumes of altcoins other than Bitcoin and Ethereum with the trading volumes of real-world assets like stocks and commodities on the Hyperliquid platform reveals a stark disparity.

Hyperliquid continuously absorbs on-chain liquidity through the launch of perpetual contracts for stocks and commodities. By mid-2026, among the top thirty perpetual contract trading volumes on that platform, 23 were stocks and commodities, while cryptocurrency assets became the minority.

The on-chain market is no longer the exclusive domain of cryptocurrencies. The trading volume of a decentralized exchange is now sufficient to compete with traditional centralized exchanges, which has raised alarms for all major CEXs.

Changes in the regulatory environment

The third layer of pressure comes from the shift in the overall regulatory landscape since the Trump administration took office. The U.S. Securities and Exchange Commission dropped lawsuits against Coinbase and Kraken. During the phase when regulatory agencies took a hardline stance, applying for traditional financial licenses came with extremely high compliance risks; now the regulatory boundaries are becoming clearer, and various financial licenses not only serve as endorsements for compliant operations but also become advantages in differentiated competition.

Within a clear regulatory framework, exchanges can leverage their existing advantages to explore new development directions. The three pressures have all become evident at the same time, compounded by the increasing market demand for stocks and various financial derivatives. If leading exchanges wish to survive in the long term, they must accelerate their transformation and venture down new development paths.

Response Strategies of Major Centralized Exchanges

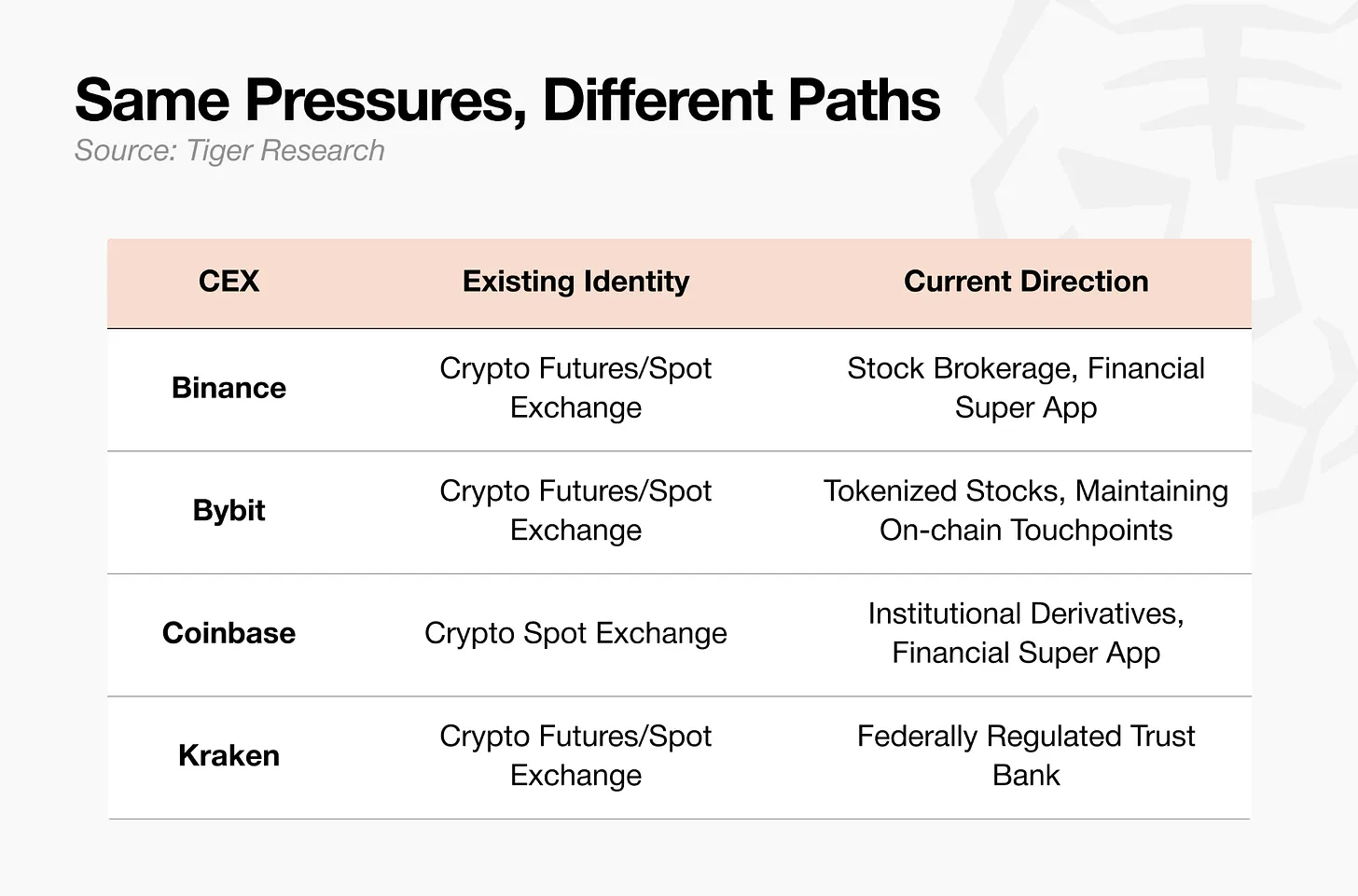

Faced with the same industry predicament, each centralized exchange has chosen distinctly different development routes.

Binance: Building a comprehensive financial super platform

Binance's development strategy is very clear: build a one-stop comprehensive trading platform that retains all user trading activities within its ecosystem to prevent user loss.

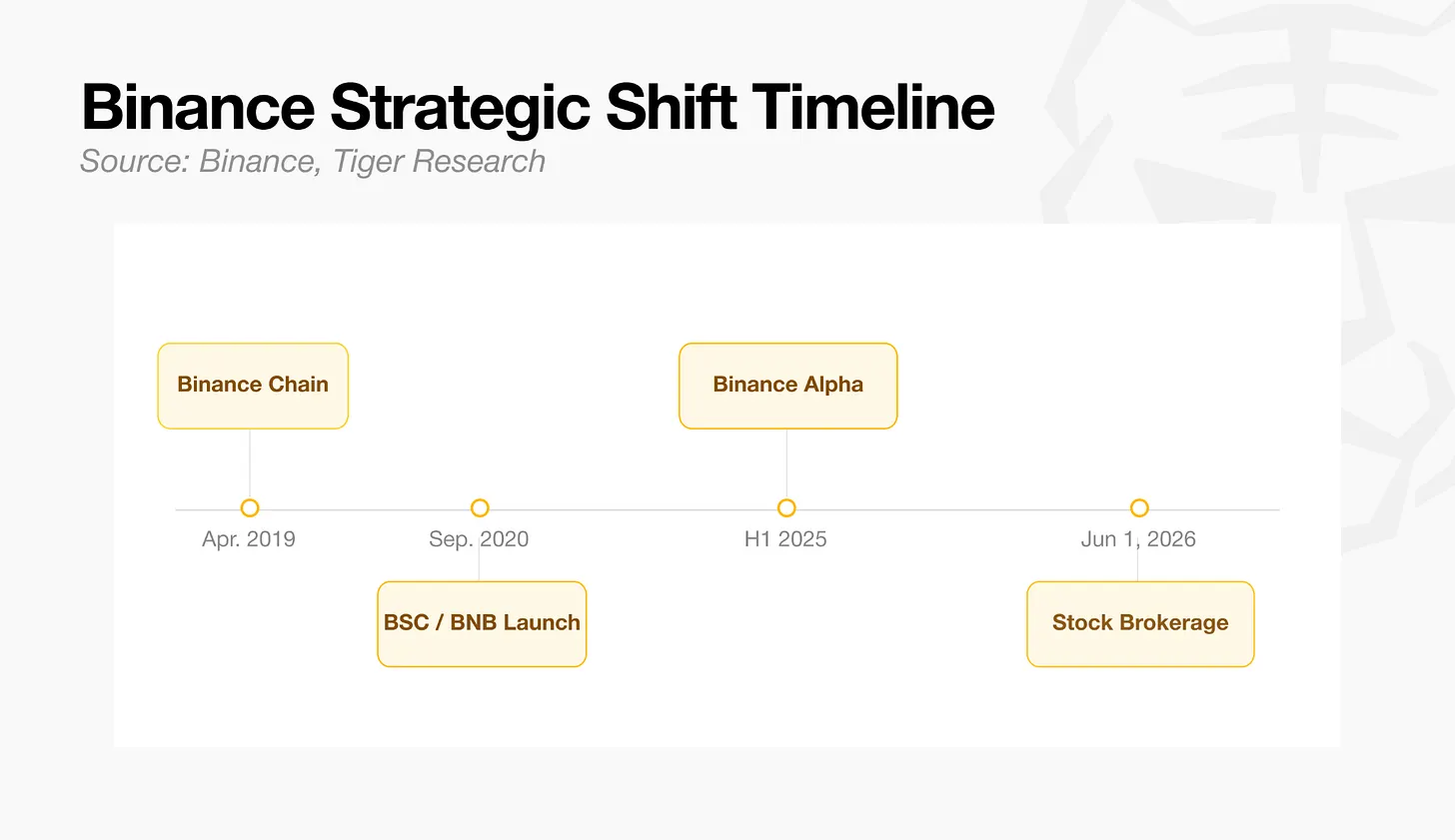

Binance has long been paving the way in the on-chain domain and has achieved notable results. The platform first established centralized trading operations, then launched Binance Smart Chain in April 2019 to penetrate the on-chain ecosystem; in the first half of 2025, it launched the Binance Alpha product, successfully capturing a significant share of the on-chain market.

However, as of 2026, on-chain liquidity began to shift towards stock categories. Hyperliquid took the lead, continuously capturing liquidity with stock and commodity-related products, directly impacting Binance's long-accumulated on-chain user base. In response, Binance did not choose to directly compete with Hyperliquid in the on-chain sector but instead found a new approach by offering stock trading services to its over 200 million existing users. Clearly, securing existing users is a more prudent choice than delving into direct competition with a rival.

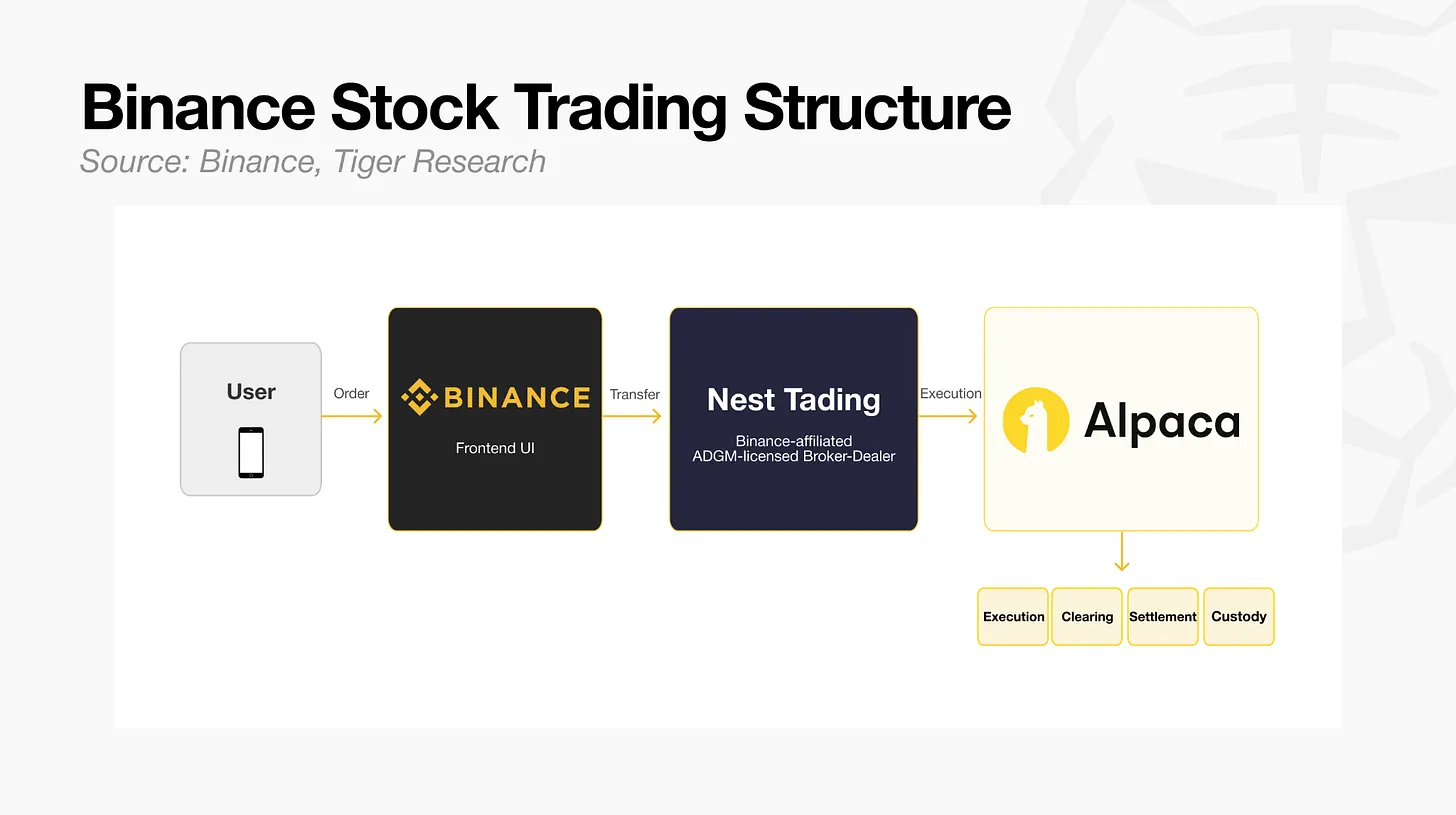

The specific operation model of this business is as follows: trading orders submitted by users at the Binance front end are first received by the licensed broker Nest Trading in the Abu Dhabi Global Market, and then forwarded to Alpaca Securities for the subsequent processes. All steps of order execution, clearing, settlement, and asset custody are handled by Alpaca. Binance does not directly hold related securities assets; this structural design allows it to avoid direct jurisdiction of securities regulation.

It is worth mentioning that Nest Trading has been confirmed as a related entity of Binance, and Binance also holds a minority stake in Alpaca. Both parties have signed a revenue-sharing agreement, allowing Nest Trading to receive 50% of order flow fees and 65% of securities lending income.

Currently, Binance is building a complete set of infrastructure independently, fully transforming into a financial super app. Before the liquidity of altcoins further flows to Hyperliquid and the stock market, the platform is fully committed to consolidating its existing user base.

Bybit: Dual-line parallel development model

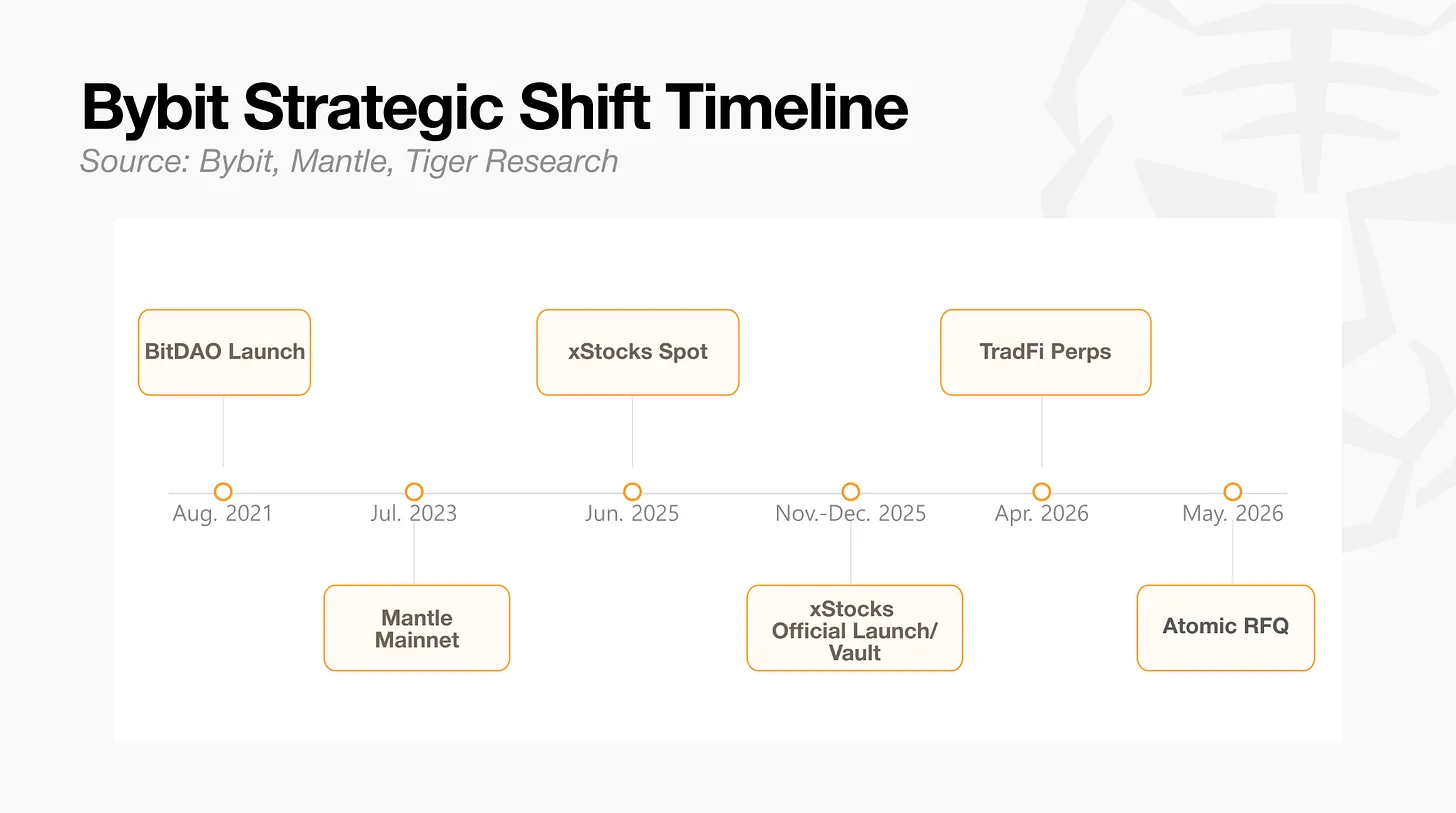

Bybit was established in 2018, starting in the derivatives trading sector, achieving rapid expansion with leverage up to 100 times and low fees. The platform now employs a dual-line parallel strategy of centralized and on-chain; on one hand, it migrates the liquidity of the centralized exchange to the blockchain network, and on the other hand, it directly launches traditional financial asset derivatives on the centralized platform.

The platform's layout initially focused on on-chain business. In June 2025, Bybit launched tokenized stock products developed by Backed in its spot sector, officially taking the first step into the realm of tokenized stocks. In November of the same year, Bybit collaborated with the Mantle public chain and Backed to launch the xStocks product on the Mantle blockchain, covering major U.S. stocks like NVIDIA (NVDA) and Apple (AAPL).

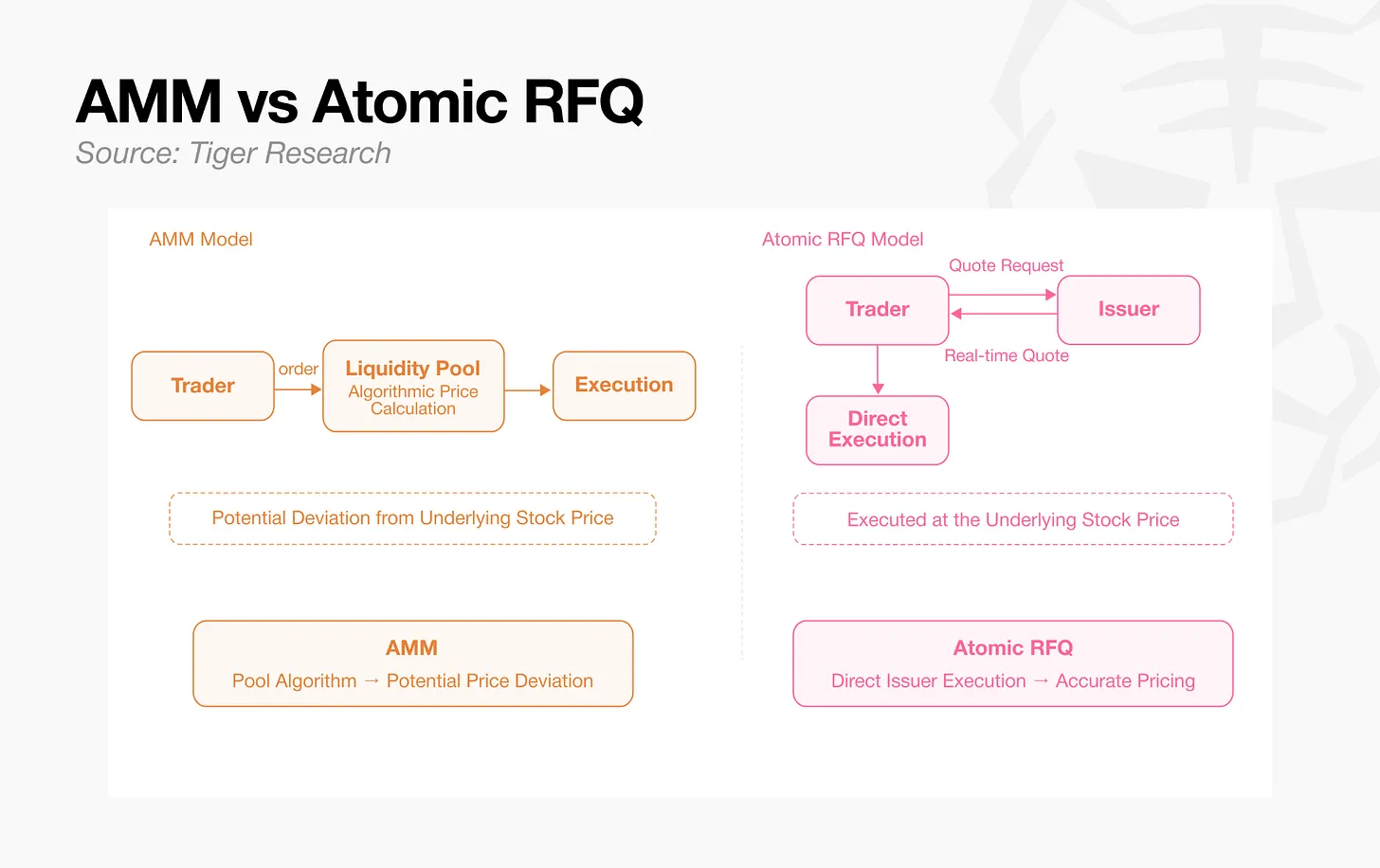

In May 2026, Bybit launched atomic pricing features on the decentralized exchange Fluxion within the Mantle ecosystem. This feature no longer relies on automated market maker order matching, but directly obtains quotes from asset issuers, enabling on-chain trades to meet the execution standards required by traditional financial institutions.

In the centralized business sector, Bybit is also making frequent moves. Affected by industry pressures similar to those faced by Binance, the platform introduced perpetual contracts for traditional financial products in April 2026, and subsequently added new products weekly. Currently, major U.S. stocks like Tesla (TSLA), NVIDIA (NVDA), Apple (AAPL), along with commodities like gold, silver, and crude oil, all support around-the-clock trading settled in USDT. On June 4, perpetual contracts for Samsung Electronics, SK Hynix, and Hyundai Motors were officially launched, and the platform also opened up pre-IPO share trading for Space Exploration Technologies Corp.

The ultimate goal of both business lines is to build a complete infrastructure that connects on-chain and off-chain scenarios, achieving refined trading of traditional financial assets. Unlike Binance, Bybit has not focused solely on its centralized platform but continues to deepen its on-chain ecosystem through Fluxion and the Mantle public chain.

Coinbase: The most reputable exchange in the U.S. market

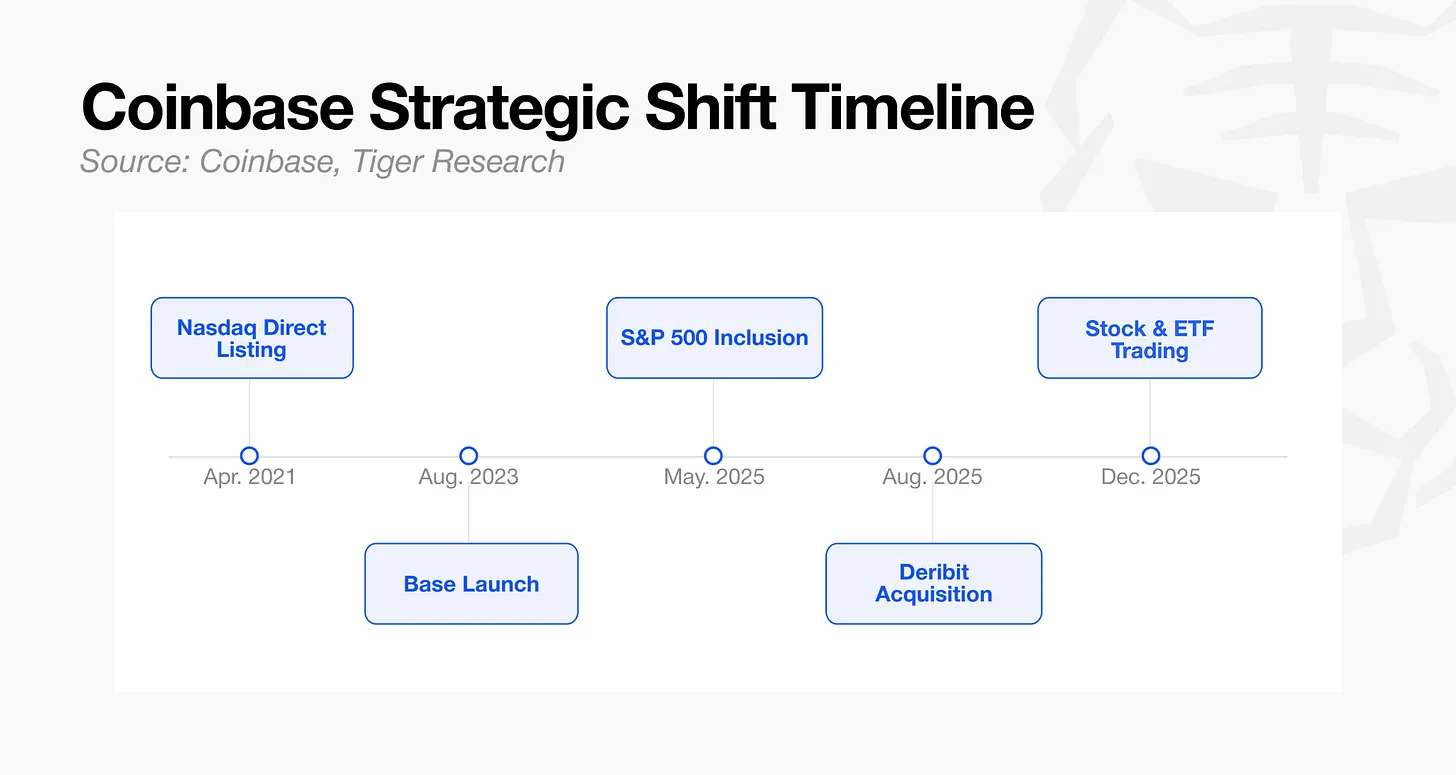

Coinbase went public on NASDAQ in 2021 and was included in the S&P 500 index in May 2025. Backed by Wall Street capital, it is currently the most recognized centralized cryptocurrency exchange globally among institutions.

Coinbase also maintains a focus on on-chain business. In 2023, it launched the Ethereum layer-2 network Base, which has grown rapidly, with its layer-2 network's total locked value at one point close to half of the total. However, entering 2026, the growth of Base stagnated and is no longer the company's core development direction.

At this stage, Coinbase's focus has shifted entirely toward institutional clients. In August 2025, the company completed the acquisition of Deribit for $2.9 billion, capturing roughly 85% of the global cryptocurrency options market. Subsequently, the platform obtained futures broker qualifications issued by the U.S. Commodity Futures Trading Commission and launched a cross-margin trading feature that consolidates spot, futures, and perpetual contract positions into a single margin account, further expanding its institutional client base. That year, the borrowing balance of hedge funds and asset management institutions on the platform reached a quarterly record high.

In December 2025, Coinbase launched zero-commission stock and exchange-traded fund trading services within its app. While Binance uses the indirect operating model of external brokers, Coinbase leverages its years of accumulated compliance qualifications to directly conduct stock trading business. On June 4, the platform announced support for pre-IPO share trading for SpaceX.

While Hyperliquid enriches its product offerings and accumulates liquidity in the regulatory gray zone, Coinbase's early investment in stock trading has also allowed it to maintain greater proactive control amid industry changes.

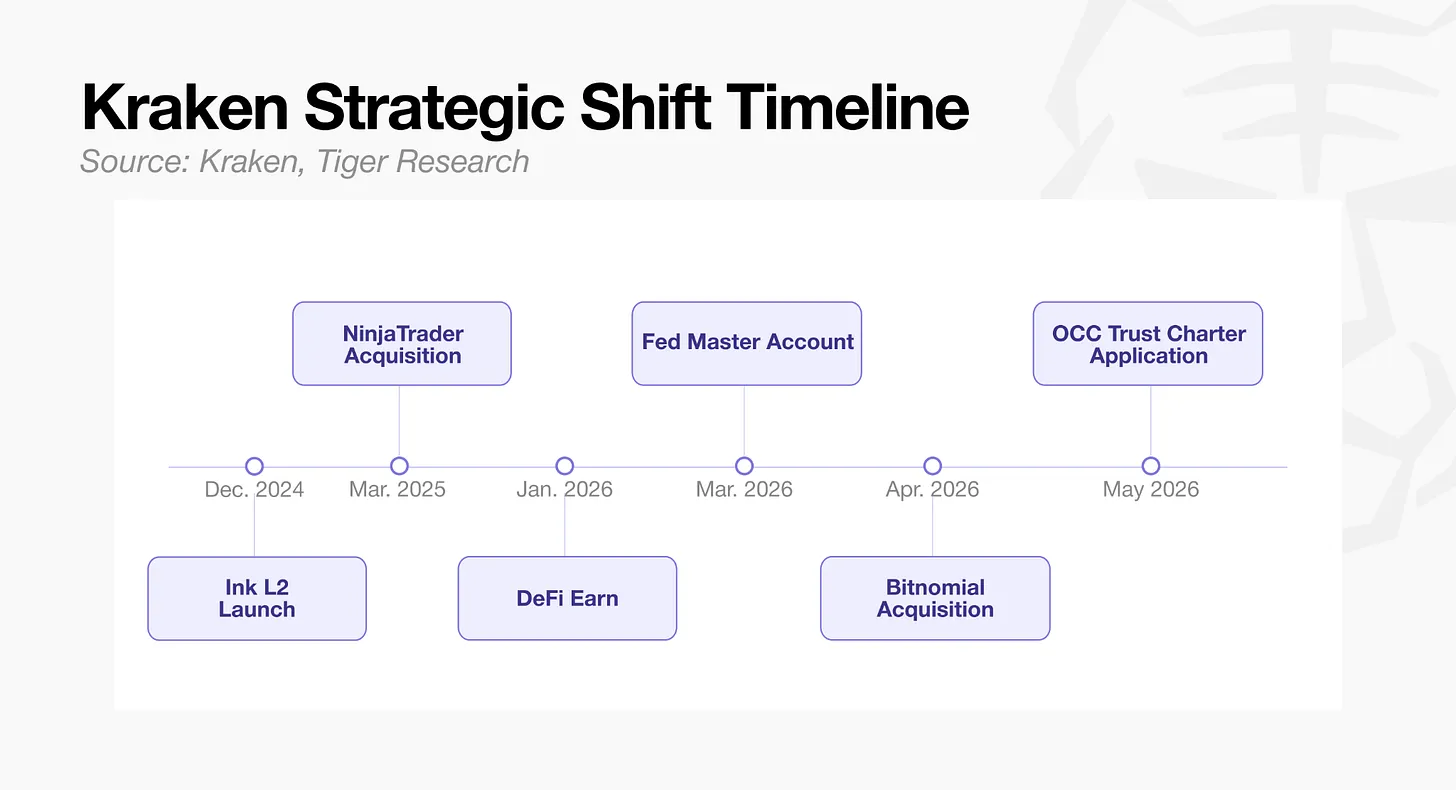

Kraken: Aiming for a federal crypto bank

Kraken was established in 2011 and is one of the longest-established exchanges in the cryptocurrency industry. Its core strategy is to continually secure various financial licenses and build its own infrastructure, ultimately aiming to create a crypto asset custody bank under U.S. federal regulation.

Acquiring compliance qualifications is Kraken's top priority. In March 2025, the company invested $1.5 billion to acquire the trading platform NinjaTrader, successfully obtaining a futures broker license from the U.S. Commodity Futures Trading Commission while also taking over the platform's 20,000 retail trader users. In April 2026, it acquired Bitnomial for $550 million. This platform, after ten years of operation, is the only native crypto platform that holds all three core licenses from the U.S. Commodity Futures Trading Commission: designated contract market license, derivatives clearing organization license, and futures broker license. In March 2026, Kraken successfully obtained a main account from the Federal Reserve; in May of the same year, it applied to the Office of the Comptroller of the Currency for a national trust company license.

While vigorously promoting its compliant layout, Kraken has not neglected the on-chain ecosystem. In December 2024, the platform launched its self-developed layer-two network Ink, then built the lending protocol Tydro and the decentralized perpetual contract exchange Nado on it. In January 2026, it launched the on-chain financial product DeFi Earn, and in May, it launched Bitcoin custody services with Bitcoin Vault. The design logic behind all on-chain products revolves around assets that can clearly articulate value to institutional clients, and altcoins are also not included in its on-chain business plans.

While other exchanges rush to launch stock trading to retain users, Kraken has chosen a different avenue, aspiring to become a trusted native crypto bank for institutional clients.

Although the specific strategies of each centralized exchange vary, there is one common point: altcoins no longer occupy an important position in the future plans of all platforms.

Where will the cryptocurrency industry go?

For a long time, centralized exchanges have been the liquidity pillar of the cryptocurrency ecosystem. Exchanges launch tokens, driving trading enthusiasm, and the vast majority of cryptocurrency projects rely on this support to survive.

The deep-seated issue within the industry is that almost no cryptocurrency project can prove its true value through actual business revenue. The support logic for token prices has never stemmed from the fundamentals of the project itself but from early traffic generation methods like exchange listings and liquidity mining. The premise for this operational model to sustain itself is that exchanges and traders maintain enthusiasm for the crypto sector.

Now, with retail trading volumes continuously shrinking, as enthusiasm wanes, exchanges' promotional resources and support will also tighten, making the original ecological model increasingly difficult to sustain over the long term.

The market trend has shifted; funds are starting to flow to projects that can create value through tangible product revenue rather than tokens that solely rely on exchange lifelines. The platform token HYPE from Hyperliquid is a typical example. Despite this platform diverting on-chain liquidity originally belonging to cryptocurrencies towards stock categories, HYPE still stands out as one of the current most notable crypto assets. This phenomenon also indicates that the originally mutually beneficial relationship between centralized exchanges and cryptocurrency projects is gradually disintegrating.

The strategic choices of major exchanges also confirm this trend. Retail trading volume and user base are the foundation of an exchange's survival. If they continue to hold firmly to a pure cryptocurrency trading model, their foundations will continue to be eroded. The market has long lost enthusiasm for newly listed cryptocurrency tokens. Exchanges have no choice but to actively explore new revenue sources while protecting their existing platform structures and user bases.

This is the core reason why various platforms are collectively turning to stock derivatives, wealth management services, and asset custody business. In the comprehensive tilt of resources, exchanges have effectively let go and allowed altcoin projects to face market challenges independently.

In the past, when the market fell into a downturn cycle, centralized exchanges would endure pressure alongside the entire cryptocurrency industry, weathering bear markets together. But now, exchanges are beginning to explore paths to growth that are independent of cryptocurrencies. This foreshadows that this round of industry downturn will be even more challenging for the crypto field than any previous bear market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。