From $626 billion to $1 trillion: After the collapse of orbital costs, how will space reshape the global economy?

Written by: Piers Kicks (@pierskicks), Founding Partner of Delphi Ventures

Translated by: AididiaoJP, Foresight News

"There are two possibilities: either we are alone in the universe, or we are not. Both are equally terrifying." — Arthur C. Clarke

Every industrial revolution has been catalyzed by a collapse in the price of a critical input. Steam, steel, transistors, bandwidth… today, the cost of leaving Earth is about to undergo the most dramatic compression in history.

Since the dawn of humanity, we have gazed up at the burning starry sky, one of the few truly universal experiences shared with our ancestors from millions of years ago. Amidst the turbulence of the modern world, I believe that mastery over the cosmic environment has the potential to propel us toward abundance, resilience, and unity.

Today, reusable rockets are reducing the cost of reaching orbit by orders of magnitude; yesterday's science fiction is turning into industrial activities in orbit and on the Moon. At the other end of this wave, there will be a world that is utterly unimaginable.

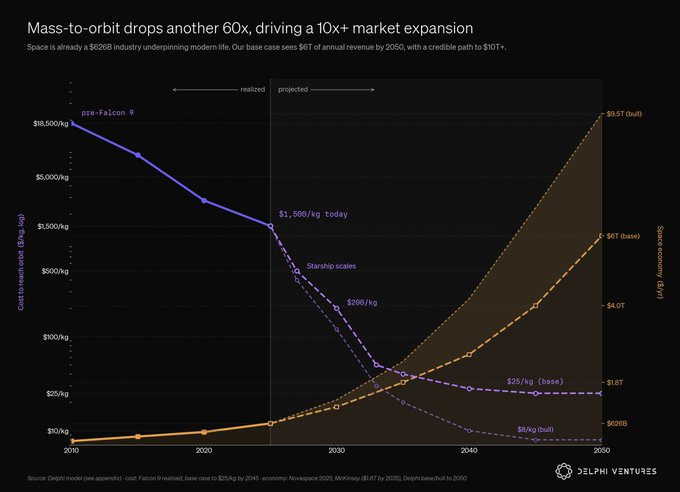

Most people think of space as a niche area, but in reality, it has already become a $626 billion industry. Our models show a credible path to reaching an annual revenue of $1 trillion within the next few decades. It underpins the cutting edge of modern life: a set of atomic clocks synchronizing the global market to the nanosecond, orbital eyes tracking ghost ships on the high seas, and an off-planet network bringing the most remote communities on Earth into the heartbeat of the modern internet. Either way, dear reader, you are heavily reliant on space.

This report explores the forthcoming era of space entrepreneurship through a single mechanism — launch costs. This is the metric around which everything else revolves. Unlike any other input, a tenfold cost reduction not only makes existing businesses cheaper but crucially, makes previously impossible businesses possible.

Just as some of today’s best founders are building on the assumption that AGI is imminent, we start with the status quo of 2026, then examine five price thresholds and the new categories of business enabled by each. Afterward, we discuss how SpaceX might become the most important company in history, what barriers this argument might break, and what it means for our investments.

My hope in writing this article is not only to illuminate the wondrous acceleration of this new landscape but also to evoke some curiosity about the possibilities ahead. The 21st century has set the stage for humanity to take its next step into the cosmos. Driven by an insatiable demand for energy in an increasingly complex civilization, this harsh environment may hold some of the answers we seek. If we are to spread the light of consciousness beyond our pale blue dot, the window seems to be opening. It may not remain open forever.

Summary

The price of leaving Earth is collapsing along a clear curve. Each threshold will change what can be built, who the customers are, and where the value in venture capital accumulates.

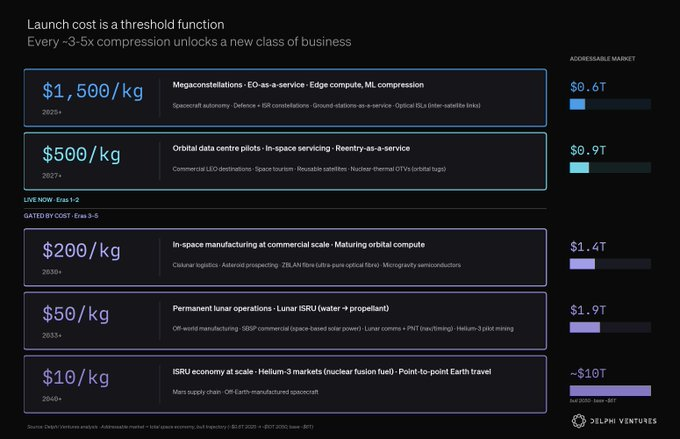

Every era gives birth to entire industries:

- $1500/kg brought about giant constellations (thousands of satellites flying as one network) and Earth observation (selling images and data about the Earth).

- $500/kg opened up orbital computing and commercial space stations.

- $200/kg unlocked large-scale microgravity manufacturing.

- $50/kg unlocked the lunar economy.

- $10/kg supported the Martian supply chain.

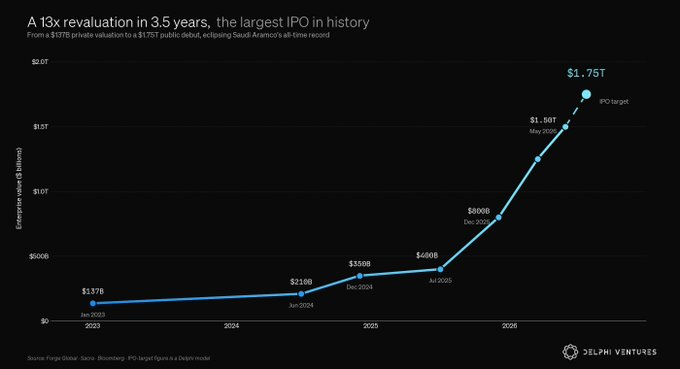

SpaceX's IPO is a macro verification event. This may be the most important company of the 21st century and will continue to capture humanity’s attention for decades after a series of price fluctuations in the near term.

A group of founders is about to emerge. Such a liquidity event will release over 500 senior SpaceX employees, who have the capital and world-class qualifications of the founding team, and we expect astonishing opportunities in the next decade.

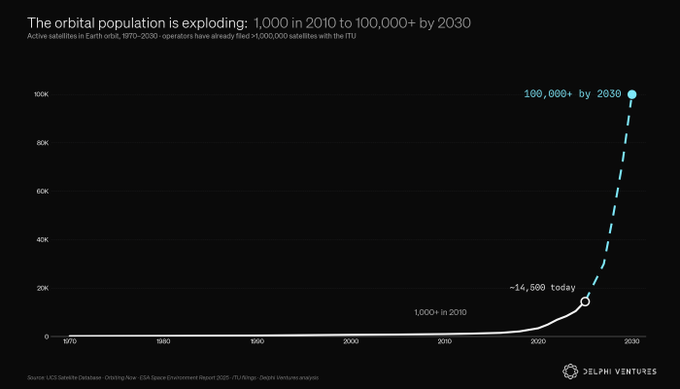

The number of satellites is exploding. From the current 14,500, we expect it to exceed over 100,000 by 2030 and reach millions by the end of the next decade. The range of applications is dizzying.

Alpha exists in a bottleneck. Cheaper launches will not make every space business successful; it merely shifts the constraints. For us, the most interesting founders in 2026 are those who are building for tomorrow's market and thinking creatively about downstream problems. The best entrepreneurs are already building for a cost reality that does not yet exist.

What could change our perspective: the Kessler syndrome (orbital collisions snowballing to destroy infrastructure), cost curves plateauing at anticipated higher levels, regulatory freezes, or unfulfilled demand. None of these will completely kill the argument, but each may push the timeline far enough to impact venture capital returns.

In hindsight, the price of reaching orbit per kilogram will be one of the most important numbers of this century: the input that allows the final frontier to achieve escape velocity.

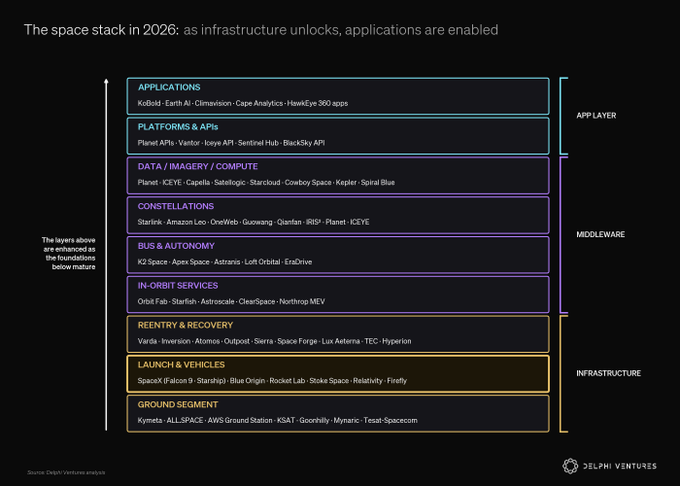

Where We Stand in 2026

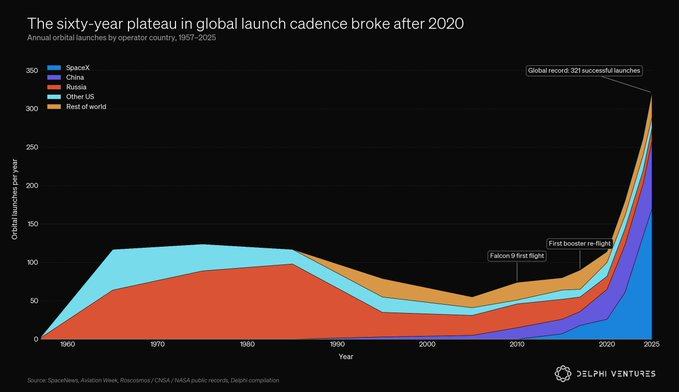

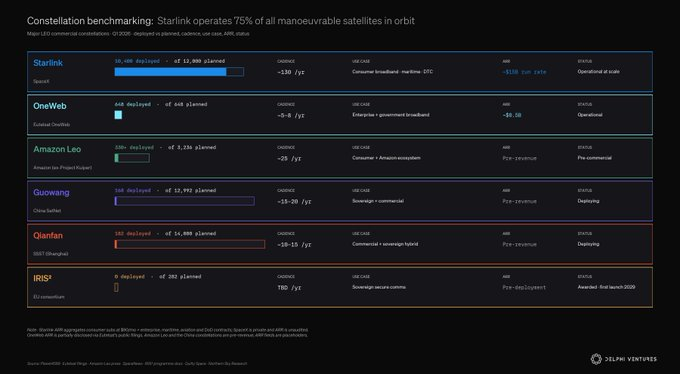

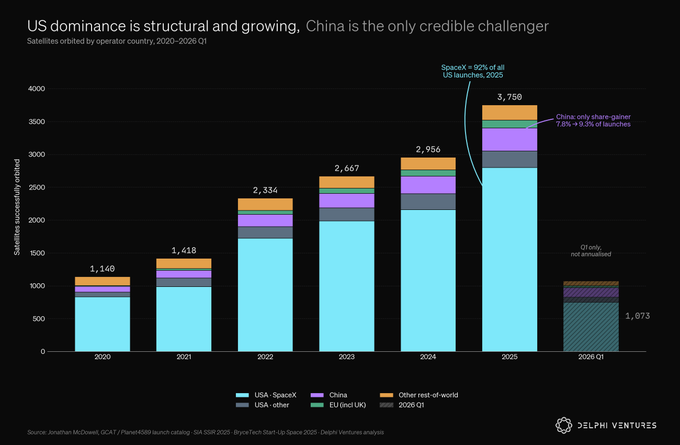

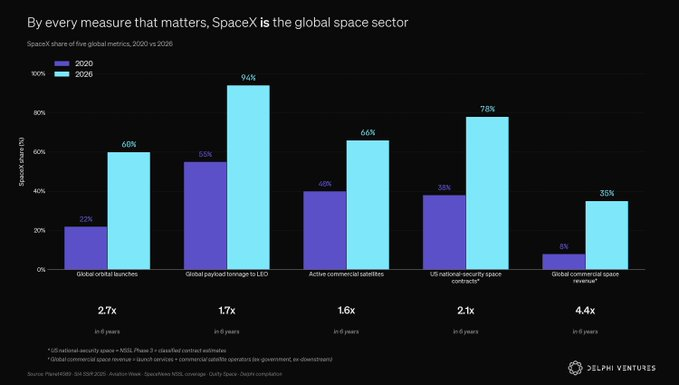

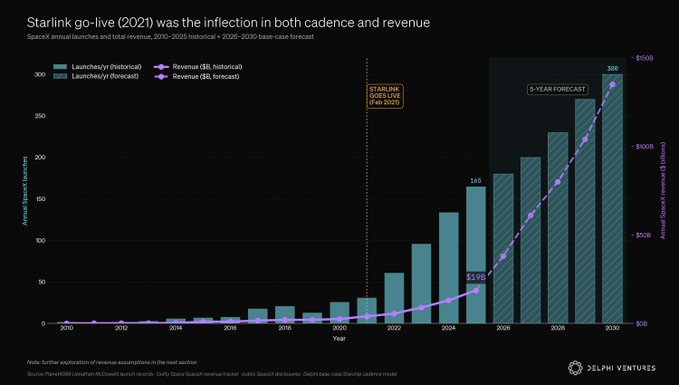

One company has distorted reality. In 2016, SpaceX conducted 8 orbital missions. By 2025, it will conduct 165: a twentyfold increase in less than ten years, surpassing the total of the rest of the world combined. In terms of payload mass, it has surpassed the total of Earth’s rest for six consecutive years. Through Starlink, it now operates nearly 75% of all maneuverable satellites in orbit — the largest constellation ever.

The cost of reaching orbit has remained nearly unchanged in the first sixty years of the space age, dropping more than tenfold in the past 15 years, and in our baseline scenario, it will be compressed another 60 times by 2045.

What makes the next decade categorically different from the past is not any one breakthrough but the confluence of forces, each pushing the others forward:

- Reusability has become the norm. The Falcon 9 booster is certified to fly 40 times, with one having already exceeded 33 flights. Starship has demonstrated nearly all crucial components for full reusability and is striving for fleet turnaround in the same day.

- The manufacturing machine is awakening. At Starfactory and Gigabay, SpaceX is not just manufacturing rockets; they are making machines that make machines, targeting an annual production of up to 1,000 Starships. They are turning rocket science into assembly line.

- Demand is meeting supply. Placing data centers in orbit sounded like science fiction in 2019, but it is now getting funded. @Starcloud_ ($2.2 billion), @CowboySpaceCorp ($2 billion), and SpaceX itself are exploring construction in response to ground power constraints.

- Capital has followed. 2025 is projected to be a record year for space tech venture capital with about $12.4 billion, up 48%, while Q1 2026 is the strongest quarter to date with about $8 billion.

- The Moon is reopening. The U.S. @NASAArtemis received $9 billion in funding with goals for a human Moon landing by 2028, a lunar nuclear reactor by 2030, and a record number of private landers reaching and landing on the Moon by 2025, while China’s ILRS aims for a manned lunar presence in the 2030s. The Moon is no longer the sole domain of NASA.

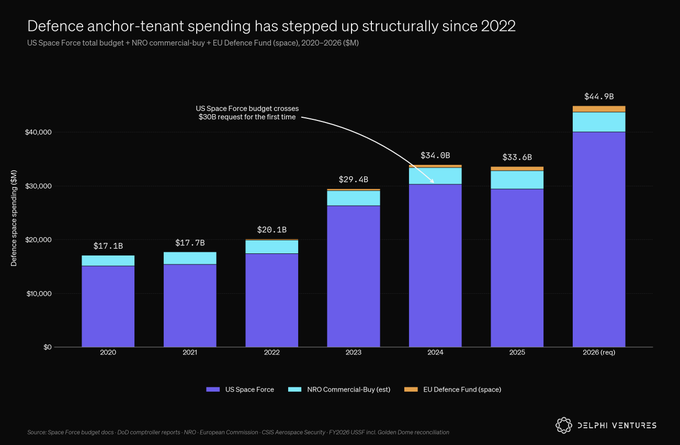

The global space economy reached a record approximately $626 billion in 2025 and is expected to exceed $1.8 trillion by 2035 (McKinsey). Roughly 78% of this is now commercial and rising. Space has transitioned from a government-led industry with commercial participation to a commercial-led industry with government as a backstop. One-third of the industry's commercial revenue is national security work — the anchor tenant of this industry. The SPAC winter from 2022 to 2024 cleared out the weakest players; what remains is a credible group of operators backed by capital that looks much like the cloud infrastructure of 2014 — a category proven but not yet commoditized.

With the James Webb Space Telescope peering back at the dawn of the universe, and the Artemis program bringing humanity's attention back to the Moon, the curious among us are once again drawn into the mysteries of space. The next decade will unleash a wonder about our place among the stars that has not been witnessed since Apollo. As Carl Sagan said:

"Our distant descendants, safely nestled on many worlds within the solar system and beyond, will gather together for their common heritage, reverence for their home planet, and the knowledge that, no matter what other life may be, we are the only humans to have come from Earth."

$1500/kg Era (2025–2027): Industrial Rocket Capacity

We are now in the $1500/kg era. This is the internal cost for the Falcon 9 to send 1 kg of payload into low Earth orbit. The published rideshare price is $350,000 for 50,000 kg, with the company retaining about 80% of profits to fund the next generation of launch vehicles. With new competitors (Blue Origin, Rocket Lab) emerging, this price is being compressed.

This is the first time in the industry’s history that the price paid by serious operators is low enough to collateralize orbital business plans based on specific risk profiles. This is an era where generalist VCs can write checks and will only be wrong on specific companies, not on the category.

Giant constellations are no longer a theoretical argument; they are a living infrastructure. @Starlink has over 10,000 active satellites, accounting for 75% of all maneuverable spacecraft in orbit, with over 10 million users.

Its network now handles approximately 600 Tbps of bandwidth. At any second of the day, humanity consumes about 3,000 terabits of data in total. This means Starlink's network capacity mathematically equals carrying 20% of the Earth’s real-time internet traffic simultaneously. The network is expected to grow to capacity measured in PB next year. Amazon's Leo (formerly Kuiper project) is in deployment; China’s State Grid and Qianfan are accelerating.

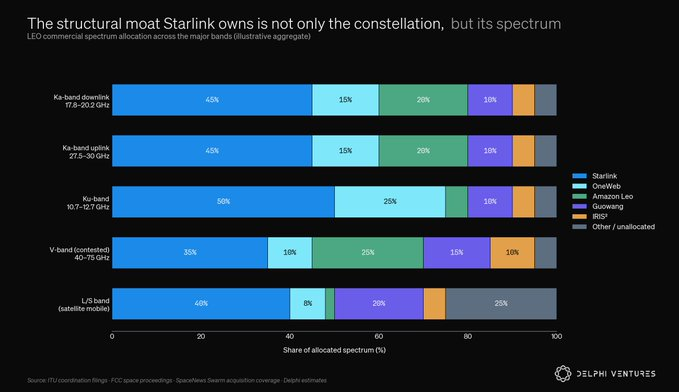

The spectrum itself is an asset class. This refers to the radio frequencies that satellites are licensed to broadcast, a critical aspect of operations. SpaceX's acquisition of Swarm for around $524 million was a game for VHF rights, not operational business. A constellation with 10,000 satellites but insufficient downlink spectrum will have total throughput lower than one with 2,000 satellites but with inherited Ka-band rights. New spectrum allocations are tightening, so these dominant players are likely to become rigid. Regulators are increasingly strictly enforcing "use it or lose it" milestone deadlines to prevent spectrum hoarding, leaving new entrants with little margin for operational error. Amazon Leo is an example, likely to face spectrum priority downgrades for failing to meet the FCC’s strict July 2026 constellation deployment deadline. They were supposed to deploy 50% of their planned 3,236 satellites by that date, but significant setbacks mean only 330 are active currently.

Earth observation as a service has taught companies that fresh imagery has API value. Planet Labs has achieved this for optical layers; ICEYE leads in synthetic aperture radar. Differentiation has shifted from pixels to inference: orbit edge ML now compresses 10 billion bytes of downlink daily into 1 billion bytes of signals before it reaches the ground, changing both unit economics and customer compositions.

A growing application layer builds on this, taking images as raw material and producing decisions. @KoBold_Metals (backed by Gates, Bezos, Altman with a last funding round valuation around $3 billion) uses satellite imagery combined with geophysical data to identify mineral deposits, having discovered the Mingomba Copper Mine in Zambia, expected to yield 300,000 tons annually by 2030. Teams like Hubble unlock global IoT infrastructure through Bluetooth-connected satellite networks. These are not space companies in the traditional sense; they are application layer companies that couldn't exist without the underlying satellite layer becoming cheap. This model is expected to replicate across mining, energy, insurance, defense intelligence, and in capturing sanction-evading tankers on the ocean.

Spacecraft autonomy as a service is the latest of four, and we anticipate it will be severely underestimated by generalist investors within the next 24 months. A constellation of spacecraft to the scale of Starlink could not be meaningfully flown by any operational team. EraDrive’s oversubscribed seed round of $5.3 million won in December 2025 is a clear example: AI-driven vision allows spacecraft to navigate, operate, and cooperate without ground controllers in the loop. The first to build it will occupy the de facto standard position that ROS holds today in robotics: a factual standard that every downstream operator builds upon, with lasting advantages belonging to the developers of a standardized SDK.

The defense channel is a significant engine. Approximately 30–40% of the industry's commercial veneer revenue is classified or quasi-classified national security work. For regions like the EU, procurement remains a major pain point, as bureaucratic processes are cumbersome, and reforms are needed to remain competitive on the global stage. (Complete spectrum, ground segment and defense details in the appendix).

The sci-fi fringe of 2026 includes @reflectorbital, selling on-demand sunlight by placing orbital mirrors for ground solar farms; Lonestar, hosting disaster recovery data in orbit; AstroForge, which lost its first asteroid probe in space; and Celestis, which is working on space funerals. A small group is still peddling orbital advertising (sigh), but fortunately, these projects have yet to secure funding.

In the $1500/kg era, the money makers are bits transmitted through atoms: images, connectivity, signals, edge computing, and the autonomous stacks that all four rely on. Atomic businesses in space are next to arrive.

$500/kg Era (2027–2030): Maturity of Orbital Infrastructure

The $500/kg era is the first time space physics economics begins to emerge. In the $1500/kg era, the orbital business case was information; below $500/kg, it is also material. Lifespan extension (refueling satellites in orbit to extend flight time), orbital habitation, re-entry as a commercial service, and on-orbit servicing are all reaching customer economics inflection points in this range.

The operational rollout of Starship, with its frequency still rising, is why we have reached this point, with New Glenn (despite some setbacks), Rocket Lab Neutron and Stoke Space Nova playing supporting roles. The competitive structure has shifted from "SpaceX and Others" to "SpaceX, two credible heavy launch entrants, and a layer of medium launch specialists." Profit compression is a predictable outcome, fueling continued cost reductions; frequency growth is a vital point.

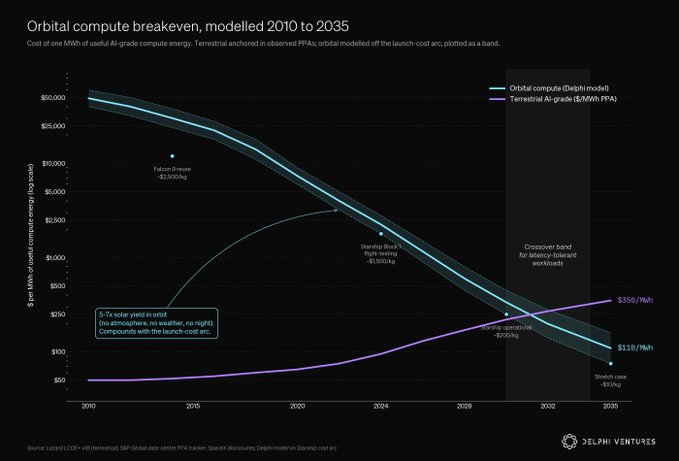

Orbital data centers. This is the largest observed catalyst for industry revenue. We expect at least one major tech company to commit to first-party orbital computing infrastructure rather than buying it as a service, and SpaceX itself will expand efforts to meet xAI's demands. The cost of power in space increasingly favors orbital.

While there are debates surrounding the technological feasibility of scaling this, it is clear that the Sun is the answer. Every few milliseconds, the energy it outputs exceeds what our species has consumed throughout history. If we could fully capture just one second of it, Earth would be powered for 500,000 years. Due to inefficiencies in energy transmission through the atmosphere (losing 70%), transforming it into tokens in orbit and transmitting it as valuable bits seems a logical endgame. Clearly, a truly advanced civilization at some point will require this capability, so I welcome this catalyst. Let the mindset of abundance enter your life.

Between Starcloud and Cowboy Space, the transition from pilot to production between 2027–2030 is a critical moment in establishing a wide ecosystem. I still haven’t heard a good answer as to how to protect billions of dollars of equipment from the next Carrington event. See our interview with Starcloud CEO @PhilipJohnston.

Massive on-orbit servicing and refueling. Orbit Fab has proved the feasibility of this infrastructure; Starfish Space is transitioning from technology demonstration revenues to recurring service contracts. Gatekeeping constraints are standard: fueling port specifications shared among major western contractors are prerequisites for market clearing.

Robotic labor force is the enabler for conducting industrial work in space. GITAI is building robotic arms for on-orbit servicing and construction and has flown demonstration hardware; Rocket Lab has internalized Motiv Space Systems as its robotic arm; seed-stage entrants like Icarus Robotics are betting on embodied AI being able to handle cargo processing and maintenance that consume scarce astronaut time today. The wager is that heavy industry in orbit will be completed by machines overseen by humans. Our fragile organic forms are poorly suited for space.

Commercial LEO destinations. Vast Space will launch Haven-1 in early 2027, a frontier contender in the post-ISS era, followed by Haven-2. The ISS's retirement in 2030 is a driving factor. By 2030, there will be two to four privately operated stations in orbit, with survivors locking in NASA anchor revenues and beginning to attract workloads from pharmaceuticals, semiconductors, and tourism. The appendix lists four serious bidders for NASA's Commercial LEO Destinations (CLD) program, which is the successor framework to the ISS.

Re-entry as a commercial service. This is one of the components Delphi is most concerned with in this era. Without a re-entry argument, there can be no on-orbit manufacturing. Varda Space Industries has demonstrated round trips with its Winnebago module, successfully re-entering its Utah recovery zone multiple times. Inversion Space is preparing its Arc lifter for its first flight in 2026. SpaceX just received FAA approval for Starfall — its base re-entry platform. The important unit economics here are not launch costs; rather, it is the frequency of downmass: how quickly can you bring things back from orbit, not just send them up. By 2030, re-entry as a service will shift the downmass from a singular, one-time task model to a standardized, recurring revenue utility line. More details can be found in the appendix.

Massive space tourism (orbital flights). Axiom private astronaut missions (around $55 million per ticket) are becoming routine, combined with SpaceX's first dedicated free-flyer tourist mission, resulting in over 100 passengers annually by 2030. It represents a small share in revenue but keeps attention focused on the skies above. We expect this to drop to between $1-5 million per seat within the next decade, with suborbital flights ranging from $50,000 to $100,000.

Structural shift: In the $1500/kg era, buyers of launches were almost always operators. In the $500/kg era, the launch and operating layers cleanly separate, just as airlines do not manufacture their own planes. Companies flying payloads no longer need to be the ones launching them. This mirrors the semiconductor industry between 1985 and 2005: TSMC’s fabless model commoditized silicon manufacturing, shifting differentiation to fabless designers who never owned a fab. SpaceX is becoming the TSMC of launches: intentionally overbuilt manufacturing capacity, deliberately commoditized pricing for external customers, and value capture moving up to operators who design payloads and own customer relationships.

The $500/kg era is when our orbital infrastructure begins to mature. On-orbit servicing becomes robust, and early manufacturing pilots begin to signify that downmass journeys are just as important as upmass ones.

$200/kg Era (2030–2033): Space Starts Producing

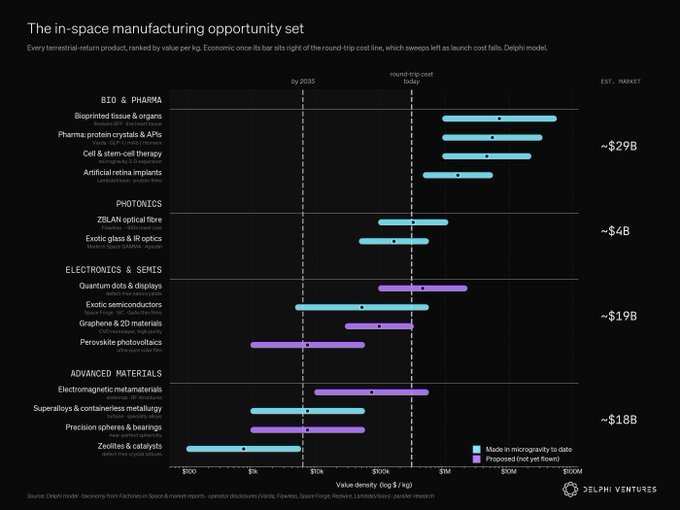

At $200/kg, the calculations flip. This is the era when space manufacturing crosses the breakeven threshold in at least three product categories. The re-entry layer built in the previous era is now core infrastructure. The total accessible market for selling space-manufactured goods back to Earth exceeds $10 billion annually for the first time.

Space manufacturing. Varda is the leader in space pharmaceuticals, sending robotic mini-labs into orbit and returning with its Winnebago fleet, focusing on drugs that are disrupted by Earth’s gravity: complex proteins for cancer treatments, fragile custom chemical combinations, and pills whose molecular shapes can only form perfectly in zero gravity. Mass Balance is building SpaceFold: a new biological model that leverages microgravity behavior to patch AlphaFold’s blind spots (disordered proteins). This allows for rapid prototyping on Earth to maximize the use of scarce space time. For materials, Hyperion as a UK entrant is scaling up to target exotic materials for production. Space Forge is producing the first plasma on ForgeStar-1, a precursor step for semiconductor-grade production in microgravity.

Crucially, all the hardware required for these is tightly coupled with the materials of manufacturing, so there is significant engineering input on form factors here. Market structure resembles early biotech: a few pure-play manufacturers, a larger vertically specific application field, and gross margins that expand because no ground alternatives can replicate the products.

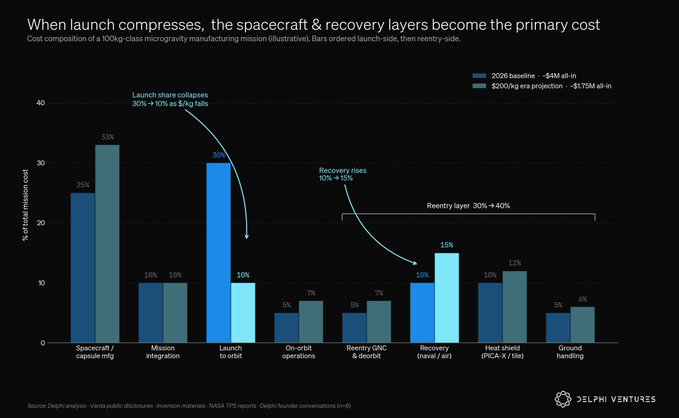

Re-entry as half of the value chain. By 2030, the re-entry layer and orbital manufacturing argument will be equal partners. Returning 1 kg from Earth at $200/kg, once accounted for recovery, heat shields, and ground handling, is about double the launch number, meaning the round-trip cost is about $600/kg. Re-entry operators become the FedEx of the orbital economy, and the spatial concentration of recovery zones becomes a strategic issue.

The lunar economy begins to resemble a continuous logistics route, rather than a series of one-off missions, with Impulse Space conducting regular booster stage missions between LEO and lunar space. It’s a small dedicated propulsion bus that transports payloads from low-cost rideshare launch points to high-energy destination orbits, just like a last-mile delivery truck picking up from a distribution center.

The NASA lunar gateway is operational, and the Artemis mission is gaining significant momentum. Space solar power (SBSP) is witnessing more pilots, though as noted earlier, it is more likely that orbital computing and manufacturing will consume marginal kilowatt-hours in orbit before anyone bothers to transmit them down significantly efficiently. SBSP and early asteroid exploration are both considered in this era and explored in the appendix.

The $200/kg era is one of shifting economic value frameworks. Space is no longer a "cost center" where we launch things that produce data but ultimately expire; rather, it becomes a commercial factory exporting high-margin physical goods to the global economy.

$50/kg Era (2033–2040): Industrial Lunar Infrastructure

The $50/kg era is when real estate on the Moon begins to look less speculative. Operations on the lunar surface shift from sporadic scientific missions to a continuous cadence of logistics akin to the early stages of Antarctic research station infrastructure: government anchored, increasingly commercialized, and with international disputes.

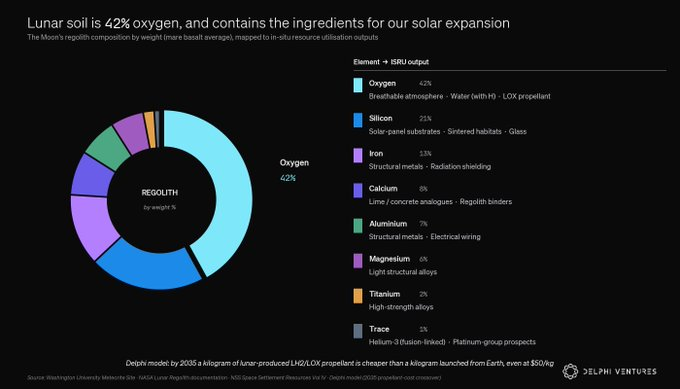

The composition of the lunar regolith offers opportunities for establishing proper industrial bases, with 40–45% oxygen by weight. In-situ resource utilization (ISRU) becomes a major focus. Once we massively process the regolith, a world full of opportunities will emerge: propellant, breathable atmosphere, life support water, sintered habitats, solar array basements, and eventually, structural metals for off-world manufacturing.

Water extraction at the poles, primarily for in-situ propellant, will become the first economically self-sustaining ISRU cycle if frequency, energy, storage, and local demands align simultaneously. By 2035, producing 1 kg of LH2/LOX on the lunar surface (used as propellant) may be cheaper than launching it from Earth at $50/kg. This will mark the first time in human history that any commodity is more economically reasonable to produce off-world than to transport from home.

The latter half of this window does not open new thresholds but is a maturity extension phase. Launches will fine-tune from $50/kg to $25/kg, with industries unlocked by previous thresholds either proving demand beyond government checks and compounding or stagnating. This is an extension phase where a core question of this report is answered: will persistent non-government demand emerge? We expect the first commercial customers to be the LEO stations and orbital factories constructed in the previous era: they are already in space, so propellant and materials lifted from the Moon will be better than towed from Earth. The demand for lunar resources from Earth will come later, if at all. (Complete lunar surface stacks, landers, rovers, communications/PNT, ISRU, hotels: appendix.)

$10/kg Era (2040+): Unlocking the Final Frontier

Most of what comes after this threshold is speculative, though the direction is inevitable. Our baseline model suggests this could appear by 2050 or later. At $10/kg, mass to orbit is no longer the constraint for any space business. Four things become possible.

Large-scale ISRU economy. Infrastructure derived from regolith on the Moon and Mars: landing pads, solar arrays, habitats, radiation shielding, propellant. Space construction is no longer assembled from Earth but built on-site. The first spacecraft wholly manufactured off-Earth will be built and launched on the lunar surface during this era, heralding the rise of the ultimate von Neumann probes.

Helium-3 and fusion connections. If and when fusion achieves commercial scale, He-3 from lunar regolith will become a tradable commodity on an industrial scale, a market several orders of magnitude larger than its current niche. If fusion fails to deliver, He-3 remains small-scale, while water and regolith-derived propellant remain the base game, either way.

Lunar mass drivers. This idea is older than it sounds: Gerard O’Neill and NASA researched lunar mass drivers in the 1970s. Musk is proposing it as the launch backbone for space AI infrastructure. Enabled by the Moon's lack of atmosphere and low gravity, an orbital cannon track would accelerate small AI computing satellites to deep space orbits at approximately 10% of traditional rocket costs. By the mid-2040s, this could transform the Moon into an automated, solar-powered kinetic shipyard extending off-world computing capacity to the ultimate "Russian doll brain" (a hypothetical cluster of computing satellites orbiting a star, gathering all its energy).

Point-to-point Earth travel. Starship Earth to Earth at $10/kg economics produces a 45-minute trip from London to Sydney, price-competitive with first-class air travel. The gatekeeping constraint is regulatory rather than technical: airspace integration, noise near spaceports, and passenger acceptability. By 2045, we expect a few routes to be operational.

Martian supply chain. Musk's true mission. The $10/kg era is the one where "making life multi-planetary" has the physical infrastructure support: regular cargo frequencies to Mars, working ISRU loops for water and propellant, and the first settlements of thousands of people. In this planet's 4 billion-year history of life, we are the first to potentially spread the light of consciousness to an extraterrestrial habitat. Beyond this threshold, humanity becomes meaningful on the Kardashev Scale: a civilization that harvests solar energy at scale from orbit, fuses helium-3 from the Moon, and operates beyond Earth’s atmosphere: several significant steps toward a Type I civilization.

"I want to die on Mars, just not on impact." — @elonmusk

Composition of Frontier Advancements

The U.S. remains dominant, with SpaceX as the anchor, but the underlying architecture is diversifying faster than the headlines suggest. China is significantly growing among over 20 private launch companies, Europe’s collective stack is solidifying, and longer-active nations like Japan, India, and the UAE have developing ecosystems.

Sixty-seven countries have signed the U.S.-led Artemis Accords, while China and Russia have formed a rival ILRS group. The recent historical rhyme is Antarctica: a frontier governed by fragile treaties, contested by flags and field stations. Platforms carry dual-use robots, and the ending resources are worth trillions. (Complete geography covering China, Europe, Japan, India, UAE, as well as sovereign mechanisms, ITAR/EAR/Artemis Accords, in the appendix.)

Key Obstacles that Change Our Perspective

Kessler syndrome cascade. The rate of new debris generation surpasses the rate of re-entry decay, threshold reliably modeled as two to four times the current active satellite population. Beyond that threshold, the rate of collision events producing debris outpaces its removal from orbit, making LEO gradually unusable for commercial operations over multiple decades. As depicted in the film "Gravity," an uncontrolled ablation cascade (arguably my favorite space-related term) could theoretically render space completely unusable. Imagine a storm of metal debris circling Earth at 30,000 miles per hour. The strongest counterargument is not "Kessler is fictional," but rather "responses are faster than bears hypothesized": proactive debris removal could become a real market in the $200/kg era, with every major constellation operator as a bona fide customer. The risk is an event in the late 2020s that showcases the cascade before cleanup economics can scale: with 100,000 satellites entering orbit by 2030, this is the most underestimated single risk in the industry.

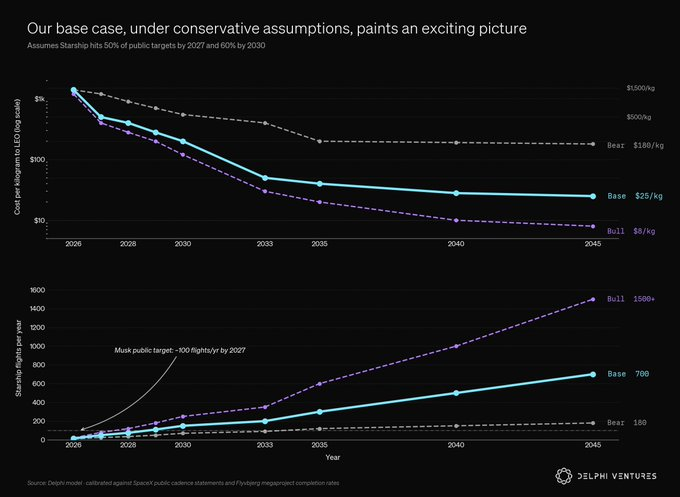

Cost curves stagnating below 10x compression. Starship's frequency target is one every 3–4 days by 2027; some analyses set the experienced baseline rate for achieving this aggressive goal at below 25%. If Starship maximizes to one a week or two weeks, the price trajectory per kilogram will plateau in the $200–500/kg range, pushing lower eras back a decade. Our baseline scenario assumes Starship reaches about half of its publicly stated frequency by 2027, reaching 60% by 2030. Even so, the $500/kg era opens on time, with the $200/kg era postponed by 2–3 years. A bear market would require Starship to fail to achieve even half its public targets, which would represent the largest single SpaceX miss in the company’s history.

It is necessary to specify how this might manifest accurately. Achieving approximately $200/kg is a manufacturing scale problem, not a physics one: it requires about 10 flights of each vehicle to reuse, with no new science from here to there. The real bottleneck is execution, not invention. Raptor engine supply is today’s constraint, so tight that before Flight 12, SpaceX scavenged engines from one booster to rebuild another. Complete upper-stage reusability has yet to be demonstrated at scale, which is a real execution risk remaining. FAA throughput limits U.S. launch volumes to around 146 per year, while the ultimate state requires thousands, which is why SpaceX is already chasing overseas launch pads. The economics beyond $200/kg depend on clearing these. Much of the report does not address this.

The demand side is absent and there is a public valuation reset. First, an honest concession: the entire report is supply-side focused. Each threshold is a statement about what cheaper launches make possible rather than depicting a plethora of urgent customers waiting. We find comfort in two areas, although they do not completely cover the field. The first is that the two largest demand pools are far from what was anticipated: AI inference and dual-use defense are today’s paying customers supporting the $1500/kg and $500/kg eras. The second is the analogy of the internet bubble, where overbuilding did not destroy the delivery of internet services, but rather pulled them forward.

We would not be surprised by a meaningful repricing of the $1500/kg paradigm within 36 months: from early 2025 to early June 2026, Planet Labs increased by approximately 1020%, AST SpaceMobile by about 423%, Rocket Lab by around 361%, this run being the market pricing trajectory rather than earnings. The most likely trigger for repricing is the SpaceX IPO itself, which would re-anchor smaller public names on $1.75 trillion+ comparable companies. Deeper questions remain: for the $200/kg and above, particularly ISRU, we are underwriting a customer base we cannot yet pinpoint.

Regulatory and geopolitical freezes. FAA Part 450 throughput lags behind commercial frequency; environmental challenges at Starbase produce months of delay; relations with China fragment spectrum, supply chains, and investment regimes. This is the most likely bear market scenario to emerge as a partial result. The probability-weighted impact is a 1–2 year delay in the post-$500/kg era: meaningful for fund cycle returns, but not for the fundamental argument.

Anchor tenant exits and founder concentration risk. The platform thesis of the $500/kg era relies on yet-to-be-fully-signed super-scale or pharmaceutical anchor commitments; the defense layer relies on politically contentious budget priorities; and the entire cost curve relies on one company executing Starship for a decade straight. No need to say, Elon is the crown jewel of our species, vital to the unlocking of this cosmic opportunity window. As I write this, I learn that Musk travels with up to 20 bodyguards and a private physician, in which he is code-named "Voyager." The details funded by his vast enterprise network, with Tesla’s $4.8 million annual contribution being just "one part of total costs." The team even has rare federal authorization, granting its crew U.S. marshal powers. There’s no way to hedge this. His security is deemed critical infrastructure, but such a high degree of personal dependency is not to be overlooked...

The Undisputed King: SpaceX

Every argument in this report is built on the foundation of one company's delivery. Five pricing eras, frequency models, re-entry layers, orbital computing, lunar logistics: all assume SpaceX. At $1.75 trillion, the listing price values SpaceX at about 93 times trailing revenue. The question is not whether this is expensive. The question is whether this is the cheapest entry fee the public market will offer for a business with no historical precedent. Below, we explore some of its underlying engines and then look at how big it could get.

The launch business is a moat, not a money machine. SpaceX conducted 165 orbital launches in 2025, surpassing the combined total of the rest of the world for the second consecutive year, and for six years in a row in terms of payload mass! With $4.1 billion in revenue, that’s a small line relative to Starlink. It’s not where the profit comes from; it’s where all other streams become possible. No one else can deliver material to orbit at this scale.

Starlink is already a major revenue line. Starlink had zero commercial customers in 2020. By 2025, it generated $11.4 billion in revenue and $7.2 billion in EBITDA, with a gross margin of 63%. Subscription users doubled within a year, exceeding 10 million by February 2026. With direct-to-phone service now opening globally, we estimate significant further upside. If they only capture 100 million global mobile subscription users at $10 per person per month, that represents nearly $12 billion in near-term revenue. Starlink's revenue growth in its first five years is on par with that of Anthropic and OpenAI.

Defense is now a structural pillar. The $5.9 billion DoD award covers 28 national security space launches (NSSL) Phase 3. A standalone Golden Dome contract is now over $6 billion, plus $41.6 billion for missile tracking layers plus a $2.29 billion follow-on in May 2026. Starshield is the fastest-growing line on the income statement. This is recurring, sovereign-grade revenue that did not exist on the income statement just a few years ago.

SpaceX is now the world’s most advanced computing manufacturer. In March 2026, the group announced Terafab, a chip factory being built in Texas in partnership with Tesla, SpaceX, and Intel. County tax filings show Phase One expenditures of $55 billion, scaling to a full scope of $119 billion, aiming for over 1 terawatt of AI computing annually. Musk's rationale is straightforward: "Either we build Terafab, or we have no chips, and we need chips."

Then there’s Colossus, a 200,000 GPU supercluster built by SpaceX in a record 6 months (with half coming online in just 120 days). Underneath it, $1 billion Tesla Megapacks (massive batteries) have buffered its power during grid outages. Industry benchmarks for comparable construction run 18 to 36 months.

In May 2026, SpaceX rented out all of Colossus 1 to its competitor Anthropic for Claude training and inference, at $1.25 billion per month, adding up to about $45 billion from now until May 2029. Three weeks later, Google signed a similar deal, worth $920 million per month for an additional 110,000 GPUs starting October 2026. Two contracts, one quarter, unlock $26 billion/year in high-margin computing revenue on a cluster with construction costs of $3 to $4 billion. Notably, Google is one of the largest data center operators on Earth, renting computing from SpaceX. This is a clear signal of excess demand and inspires confidence in the bottom line of this revenue line. Meanwhile, SpaceX shifts its own frontier work to a larger Colossus 2.

So, how much might SpaceX be worth?

Elon has openly spoken about the endgame: a single entity uniting SpaceX, xAI, and Tesla under one roof. While there may be insurmountable governance hurdles, deep collaboration is already underway. When SpaceX absorbed xAI in February 2026, he referred to it as "the most ambitious vertical integration innovation engine on and off the planet." While this may sound like marketing, it’s the most literal description of what is being built:

- Chip manufacturing

- AI that maximizes truth-seeking

- Macrohard: software user simulation

- Monetizing excess computing to competitor labs

- Social media platform with currency orbits

- High-throughput global data networks

- Orbital data centers (and AI satellites)

- Permanent bases on the Moon

- Lunar satellite mass drivers

- Colonizing Mars

What makes this more than just a conglomerate is that each pillar lowers the costs for the next. Terafab's silicon eliminates dependence on NVIDIA allocations and profits, thus computing scales on SpaceX’s own supply. The computing trains models; the models run on the same AI5 silicon inside Optimus; while the robots are the things that build the next factories, one day becoming new planetary infrastructure. Tesla’s Megapacks provide power continuity, and every competitor's AI builder gets constrained by grid dependencies. Under all this is launch: cheap reusable lift is the input cost for Starlink (the most advanced mega constellation ever), orbital computing, defense, and Mars. Meanwhile, scaling Starlink and AI produces cash to fund further R&D, thus further lowering costs.

No traditional multiple is suitable for a self-reinforcing engine spanning launches, orbital infrastructure, energy, computing, and frontier models that are at the center of all this, as well as digital (X, 500 million+ users) and physical (Tesla, 10 million cars, soon humanoid robots) networks for distributing it. This is the true Elon premium. It’s not personal worship but compounded selectivity of operators who control the value chain more than anyone else before.

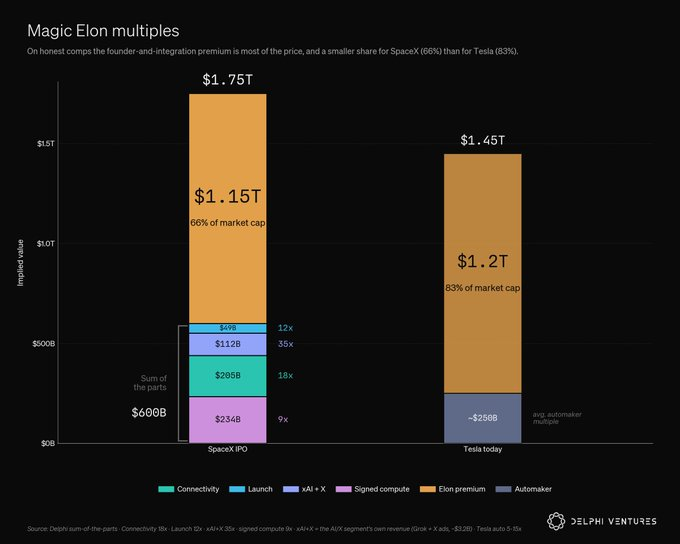

If we break that down by revenue buckets and assign fair multiples for each, we arrive at the following numbers. Starlink at 18x, slightly above NVIDIA due to space connectivity monopoly growing at 40%, with a gross margin of 63%; launches at 12x (not glamorous, but with massive demand); their in-house AI line at 35x, on par with OpenAI; signed computing contracts at 9x (similar in scope to new cloud, growing rapidly). These parts add up to $600 billion. The listing requires $1.75 trillion. About $1.15 trillion is what skeptics call the Elon premium and view it as a vote of market pure belief. With Tesla, the same premium reaches 83%. This is not all hype, as it also embeds selectively for humanoid robots (Optimus) where private leaders like Figure ($39 billion), Apptronik ($5.3 billion), and Robostrategy (BOT, public market index) are seeing valuation growth.

The SpaceX analogy is not a traditional tech company. These are companies that own planetary-scale infrastructure once in a century. The East India Company had a private army of 250,000, double that of the British, minted its own currency, collected taxes, and ran its own courts: a company that became a sovereign power, responsible only to its shareholders. I urge you to consider what SpaceX may look like by the end of this century.

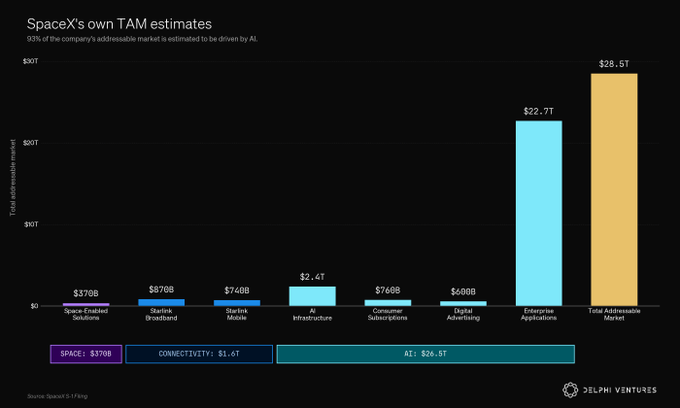

SpaceX disclosed some quite bold TAM estimates in its S-1 filing. Historically, no company has ever reached $1 trillion in annual revenue. Amazon is currently at $740 billion, and is likely to be the first to achieve this within this decade. SpaceX needs to grow 50-fold from its current $18.7 billion to reach this scale, which has no historical precedent — akin to the revenue levels of a mid-sized economy.

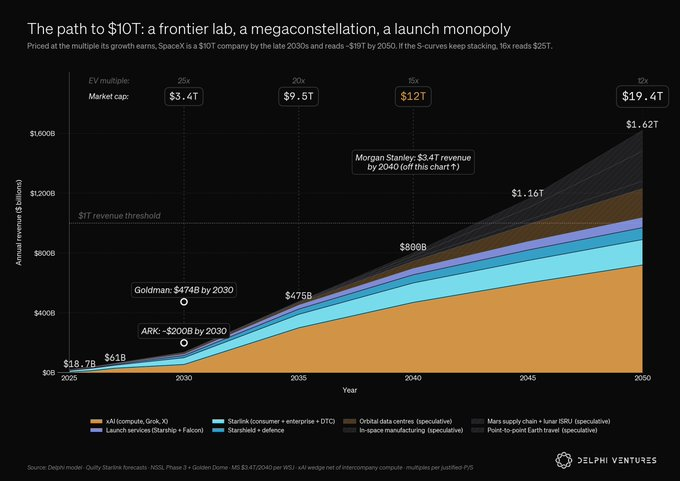

Underwriters have mentally positioned themselves at this point: Goldman Sachs’ model predicts SpaceX’s revenues will be $474 billion by 2030; Morgan Stanley predicts $3.4 trillion by 2040. Both institutions agree that AI is the primary driver.

Our Expectations

We have taken a more conservative revenue forecast. Our baseline scenario is approximately $135 billion by 2030 and about $800 billion by 2040, below the two underwriters, as these numbers are what we can verify item by item. Signed computing contracts will expire in 2029, while large-scale orbital computing will likely not materialize until the mid-2030s.

We use this relatively conservative revenue line, combining it with the multiples the market may actually be willing to pay for the monopoly position, growth potential, and optionality value we have described above.

Based on this model, a 25x multiple in 2030 corresponds to a $3.4 trillion market cap, reaching a $10 trillion company in the later 2030s, and around $19 trillion by 2050. During major cost collapse eras, multiples will remain high, only gradually retreating as the business matures.

The multiple framework can be separated from the revenue model. If we input the underwriters' own revenue forecasts into our multiple framework, we get a completely different picture: Goldman’s 2030 target corresponds to an $11.9 trillion market cap, while Morgan Stanley’s 2040 revenue implies around a $51 trillion market cap.

All assumptions around cost compression suggest that as the base grows, growth will naturally slow down, just as ordinary companies age. But the core idea around SpaceX’s fully vertically integrated stack is that it has more significant catalysts ahead than any company in history. If the new wave of opportunities matures as the previous wave peaks, growth can continue. If that indeed occurs, its long-term steady-state multiple may be higher than we are currently assuming.

The most counterintuitive point of SpaceX's strategic positioning is that it benefits far more from a thriving competitive ecosystem than from a monopoly.

- Launch frequency requires demand support. Every Vast space station, every Varda return vessel, every Anduril tranche order will pull down the marginal costs for Starship, benefiting Starlink.

- Defense revenues depend on a healthy commercial sector. The Department of Defense’s "commercial procurement" model only works effectively when there is an active commercial market; if the entire commercial sector declines, NSSL projects become single-source contracts, leading to price caps, audits, and political scrutiny. A healthy commercial flywheel is the key for SpaceX’s defense margins to be politically sustainable.

- Colonizing Mars requires planet-scale capital. Even if SpaceX's market value reaches $10 trillion, it cannot independently finance Mars colonization; it needs all adjacent industries to mature in sync.

Assuming the key risks we’ve discussed do not materialize, how large could the space economy ultimately be?

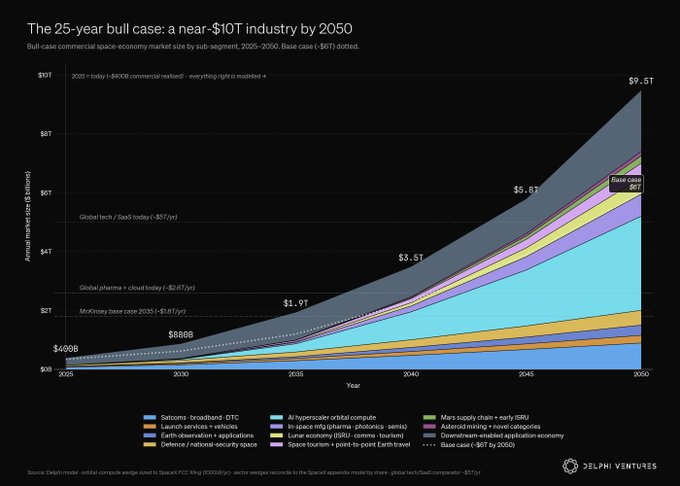

The current scale of the space economy is approximately $626 billion. Mainstream forecasts (McKinsey + World Economic Forum) expect it to reach $1.8 trillion by 2035 (11% CAGR); Morgan Stanley and PwC predict $1-2 trillion by 2040. Continuing this trajectory to 2050 yields a baseline scenario of about $6 trillion.

Our view leans more towards a bull market scenario: reaching $10 trillion in annual revenue by 2050. This requires large-scale implementation of orbital computing, along with at least one of material sciences or microgravity drug manufacturing as accelerators. We estimate the joint probability to be around 15-20%.

In pharmaceuticals, Eli Lilly's single drug tersotide reached $36.5 billion in revenue in 2025, expected to approach $70 billion by 2030. If microgravity manufacturing births 2-3 equivalent GLP-1 molecules over the next 25 years, then this single class could rival the scale of the entire upstream space economy today.

By 2050, the scale of the space economy in bull market scenarios will approach twice the total sum of today’s global tech/SaaS industries. Notably, as of 2026, approximately $5-7 trillion of economic activity will depend on space services.

Conclusion

Space is the hardest hardware domain humanity has ever attempted, where 99% correctness is often not good enough. The venture capital picture is extremely brutal: it takes companies 8-12 years to exit, with extremely high capital intensity; engineers must build in vacuum-grade clean rooms, test in harsh physical environments, and then wait months for launch windows to see if their hypotheses withstand reality. The graduation rate from Pre-seed to Series A is less than half that of the software industry. Most space-themed funds established between 2019-2023 are unlikely to return capital.

We have no illusions about this. We believe this asymmetry is worth bearing when the right founders are chosen, and cost assumptions are made well. We primarily invest our own capital, so we will not optimize for quarterly valuations or 24-month story arcs. We can remain patient.

Before the market believes, first trust the cost curve and build toward the economic realities that do not yet exist.

SpaceX's $1.75 trillion valuation is the beta of this bet, while alpha exists in earlier seed rounds — those projects that forecast new constraints early. We are supporting founders constructing new applications of space-derived data; those transforming off-world conditions into pharmaceuticals and exotic material factories that cannot be produced on Earth; those building the autonomous coordination layer for the "Sky Net"; and those whose ideas still seem like science fiction to most.

History shows that capability does not necessarily accumulate. The roads built by the Romans, replicated by none in the Middle Ages; Polynesian navigators traversed oceans by stars and waves, yet their descendants lost the routes. The last time we walked on the Moon was in 1972, over 50 years ago.

We stand at a critical point in humanity's ambition to become an interstellar species. The ability to leave the cradle of Earth does not inexorably move forward. It is a fragile flame, and the next decade will determine whether this new space age can ignite.

"When we leave the lunar Taurus-Littrow, we come in peace and with the hope of all mankind, and God willing, we shall return."

— Eugene Cernan, Apollo 17 Commander, December 14, 1972

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。