Key Takeaways:

The Federal Deposit Insurance Corporation (FDIC) said total unrealized losses climbed $19.0 billion, or 6.2%, from the prior quarter, according to its quarterly banking profile for the first quarter of 2026. The agency tied much of the increase to a rise in the 30-year mortgage rate in March, which lowered the value of the mortgage-backed securities that banks hold in size.

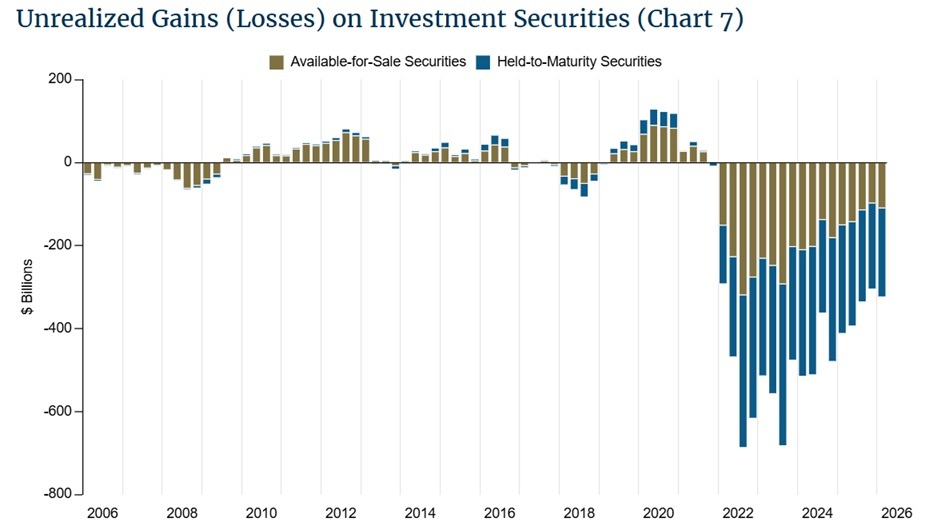

Unrealized losses on held-to-maturity and available-for-sale securities portfolios, per FDIC

Unrealized losses are paper losses on bonds and other securities whose market value has fallen below the price a bank paid. They split into two buckets, i.e. available-for-sale (AFS) securities, which carried $110.6 billion in losses, and held-to-maturity (HTM) securities, which accounted for $214.5 billion. The losses only become real if a bank is forced to sell the underlying bonds before they mature.

On the surface, the industry looks healthy as banks earned $80.5 billion in net income in the quarter, up 3.6% from the prior period, with return on assets reaching 1.26%. Domestic deposits also grew $389.7 billion, a seventh consecutive quarter of growth, suggesting depositors are not fleeing en masse.

Yet the unrealized-loss figure is the same kind of stress that helped topple several regional lenders in 2023, when institutions including Silicon Valley Bank were forced to sell underwater bonds to meet withdrawals and crystallized losses they had hoped to ride out. As long as rates stay elevated, the gap between what banks paid for their securities and what those holdings are worth today remains a latent risk on balance sheets.

Bitcoin.com News has tracked the aforementioned banking-sector strain for years, with the Federal Reserve previously revealing that 722 banks reported unrealized losses topping 50% of their capital, while separate reporting flagged some $517 billion in unrealized losses and dozens of troubled institutions across the system.

For proponents of bitcoin, an asset held in self-custody carries no counterparty and no maturity mismatch, the very mechanics behind the unrealized losses now piling up on bank books. For the time being, the $325.1 billion figure sits firmly in paper-loss territory and does not threaten the system on its own, turning real only if higher-for-longer interest rates or a sudden deposit exodus force banks to sell.

The next reading, due in the FDIC’s second-quarter profile, will be one to watch out for as it will reveal whether the trend is easing or deepening, and whether the gap between record profits and growing securities losses can keep widening without tangible consequences.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。