The market is pricing in about a 50% chance of a rate hike within 2026.

Written by: Zhang Yaqi

Source: Wall Street Vision

Driven by the Middle Eastern conflict, energy prices have surged sharply, and the Producer Price Index (PPI) for April in the United States far exceeded expectations, marking the largest increase in over three years. U.S. Treasury yields jumped accordingly, and bets on a rate hike by the Federal Reserve have significantly intensified.

On the 13th, data released by the U.S. Bureau of Labor Statistics showed:

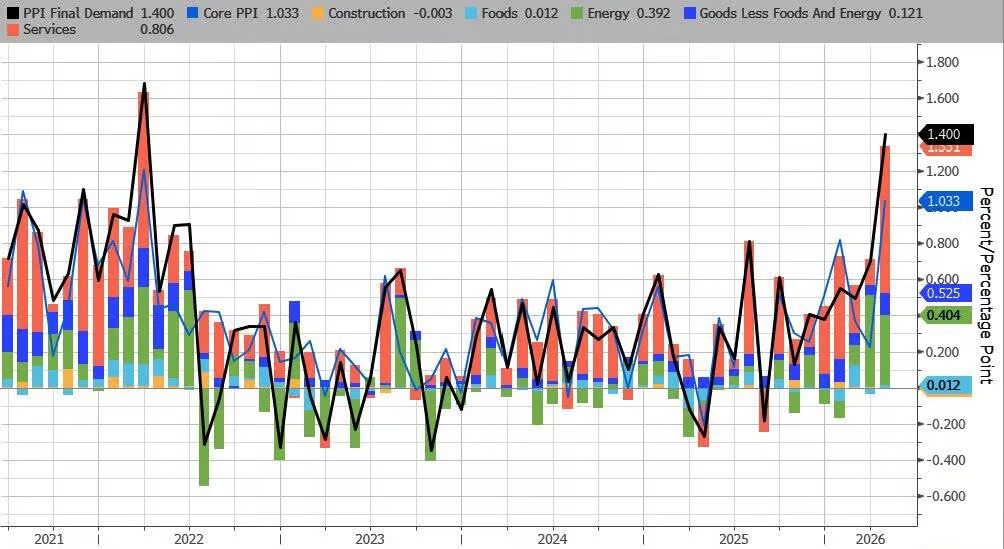

- The U.S. April PPI rose 6% year-on-year, the highest level since December 2022. The expectation was 4.8%, with a previous value of 4%.

- The U.S. April PPI increased 1.4% month-on-month, the largest single-month increase since March 2022, while the expectation was 0.5% with a previous value of 0.5%.

- The U.S. April core PPI rose 5.2% year-on-year, with an expectation of 4.3% and a previous value of 3.8%.

- The U.S. April core PPI increased 1% month-on-month, with an expectation of 0.3% and a previous value of 0.1%.

After the data was released, the 10-year U.S. Treasury yield rose about 2 basis points, reaching approximately 4.49%, the highest level since July; the 2-year yield returned to above 4.00%, a new high since March. The money market is currently pricing in about a 24-basis point rate hike by the Fed before the June 2027 policy meeting, up from 21 basis points at Tuesday's close, as the market prices in about a 50% chance of a rate hike within 2026.

Stifel's Chief Economist Lindsey Piegza stated on Bloomberg TV, "The discussion of a rate hike may be reopening, but the Fed's primary task is to remove dovish language from its statements and reiterate a wait-and-see stance." She also warned, "What's more concerning is that today's report shows that the impact of inflation pressures has not yet fully materialized." The aforementioned PPI data follows the release of the April CPI report on Tuesday, which also showed that inflation on the consumer side accelerated significantly due to soaring energy prices.

Energy and transportation costs both surged, with service industry inflation reaching a four-year high.

The sharp rise in the April PPI was mainly driven by the dual increase in energy and service prices. Data showed that energy costs rose 7.8% year-on-year in April, with even larger increases the previous month; the overall increase in commodity prices was also the highest since 2022.

Service prices rose 1.2% month-on-month, marking the largest increase in four years. Among them, transportation and warehousing service prices jumped 5%, driven mainly by rising road freight prices and expanding profit margins for fuel retailers. Analysts had previously identified this category as one of the most sensitive fields to energy price hikes driven by the Middle Eastern conflict. Amid a fragile ceasefire, with no end in sight for the Middle Eastern conflict, the rise in energy and transportation costs is gradually spilling over into a broader range of goods and services, with the pressure for businesses to pass on costs continuing to accumulate.

Notably, construction costs experienced a slight month-on-month decline this month, forming one of the few weak components in the report.

PCE-related components are relatively mild, providing some buffer

Excluding food and energy, the core PPI rose 5.2% year-on-year, exceeding market expectations and reaching the highest level in over three years; the month-on-month increase was 1.0%, about three times the expected value of 0.3%.

Although the overall data is striking, some components linked directly to the Fed's key inflation measure—the Personal Consumption Expenditures Price Index (PCE)—showed relatively stable performance, providing some buffer for market sentiment.

Specifically, portfolio management fees fell 2.4% month-on-month, and increases in various healthcare subcomponents did not exceed 0.3%. Although ticket prices rose 3% month-on-month, overall, the subcomponents that directly affect the PCE showed limited increases.

This suggests that the direct impact of the April PPI on the PCE may not be as severe as the surface data indicates, but analysts warn that this is not enough to completely alleviate concerns about inflation risks.

Treasury yields soared, rate hike discussion reopened

Two consecutive days of unexpectedly high inflation data have led to a significant shift in market expectations regarding the direction of Fed policy. Lindsey Piegza stated that the Fed's more likely actions in the near term are to remove dovish language from policy statements and reiterate a wait-and-see stance, rather than to immediately initiate a rate hike. However, she stressed that the inflation pressures revealed by the current data have not yet fully transmitted to the broader economic system, and subsequent risks should not be ignored.

Previously, there was widespread expectation that the Fed would maintain a wait-and-see approach or even shift towards rate cuts; however, after the release of the latest data, the market has begun to price in the possibility of a rate hike, with the 2-year yield returned above 4.00%. The market's estimate of a rate hike within 2026 is about 50%.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。