Article Compiler: Block unicorn

Markets constantly evolve; this is their inherent law. They eventually surpass the products originally designed. The Chicago Mercantile Exchange (CME), established in 1898, started as an exchange primarily trading butter and eggs, later developing into the world's largest derivatives market. Amazon initially sold paperback books by building warehouses and payment systems. Today, the same system does not care what it sells. Books may now represent just a trivial part of Amazon's revenue.

This model still applies today. You initially build infrastructure for something, then discover it can also be used for many other things, and then you constantly expand your business to accommodate everything the infrastructure can support.

Cryptocurrency exchanges are experiencing this moment.

The infrastructure they built for token trading is also applicable for trading crude oil, silver, stock indices, pre-IPO stocks, or event contracts. In the past seven months, non-cryptocurrency perpetual contracts have accounted for 99% of all trading volume, and this unlicensed trading market did not exist two years ago.

This market model is everywhere. Every exchange is competing to transform into a multi-asset brokerage, and blockchain technology provides the most economical means to achieve this.

The Cheapest Path

Perpetual futures contracts or prediction market contracts do not care whether the underlying asset is Bitcoin or crude oil. All you need is a wallet funded with stablecoins to purchase a futures contract for some meme coin or to bet on Apple's quarterly earnings results. The trading platform itself does not care about the underlying asset, just as the internet and logistics networks do not care about what products are traded on Amazon's marketplace.

But why are traders willing to abandon existing trading venues and instead trade silver and stocks on an exchange established only a few years ago? The reasons are the same as why people choose to trade online: convenience and cost savings.

Amazon cut out the middleman, allowing distant sellers to ship directly to buyers. This enables sellers to beat competitors by offering subsidized prices. Meanwhile, buyers can easily browse a vast selection of goods from home (or anywhere else), add items to their cart, and complete payment.

While the cost advantages provided by blockchain were initially built for cryptocurrency trading, they also apply to stock settlement, commodity clearing, and cross-border stock trading.

The 24/7 real-time market made possible by blockchain also allows global traders to price events at any time. In the past few months, we have repeatedly witnessed their impact on non-cryptocurrency assets.

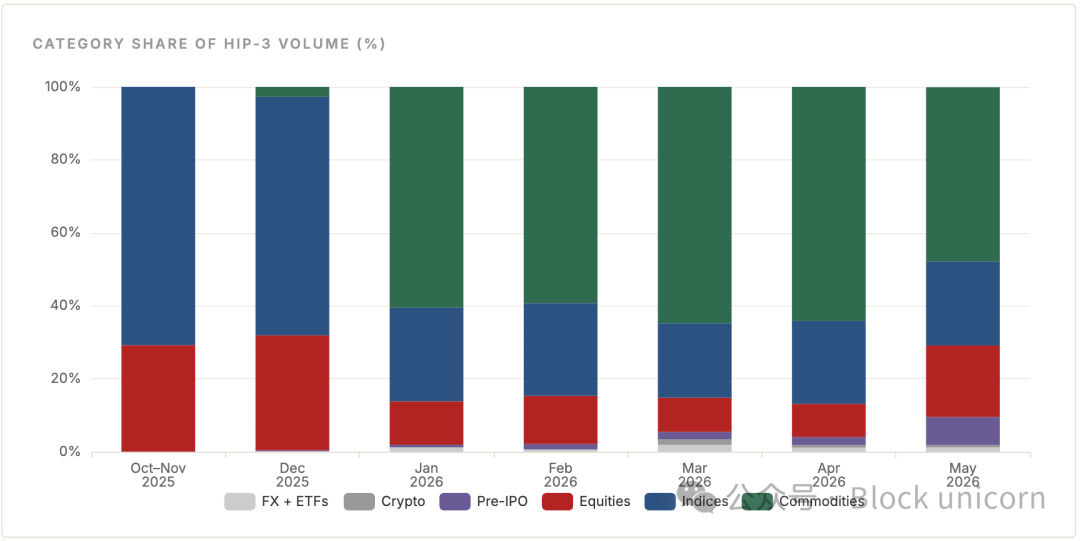

Since October 2025, Hyperliquid’s unlicensed market (HIP-3) has processed approximately $270 billion in transactions across seven trading venues deployed by developers. 99% of these transactions come from commodities, stocks, forex, indices, and pre-IPO contracts. Cryptocurrency trading volume has always remained below 1%. Moreover, the asset mix continues to diversify every month.

On the last weekend of February this year, the conflict between the U.S. and Iran escalated, causing the world’s largest commodity exchange, the Chicago Mercantile Exchange (CME), to close. However, Hyperliquid’s WTI crude oil perpetual contract did not shut down. In just three weekends, the trading volume on the platform soared from $25 million to over $550 million. According to a recent report by TD Securities, before the CME reopened on Monday, Hyperliquid had already absorbed about 80% of the subsequent volatility in WTI crude oil prices.

Earlier this year, during the rise in precious metal prices, the daily trading volume of silver perpetual contracts even approached $1 billion. Even when traditional markets shut down, blockchain-based trading platforms continued to trade.

This phenomenon is not exclusive to criminals; the same could be observed in stock trading.

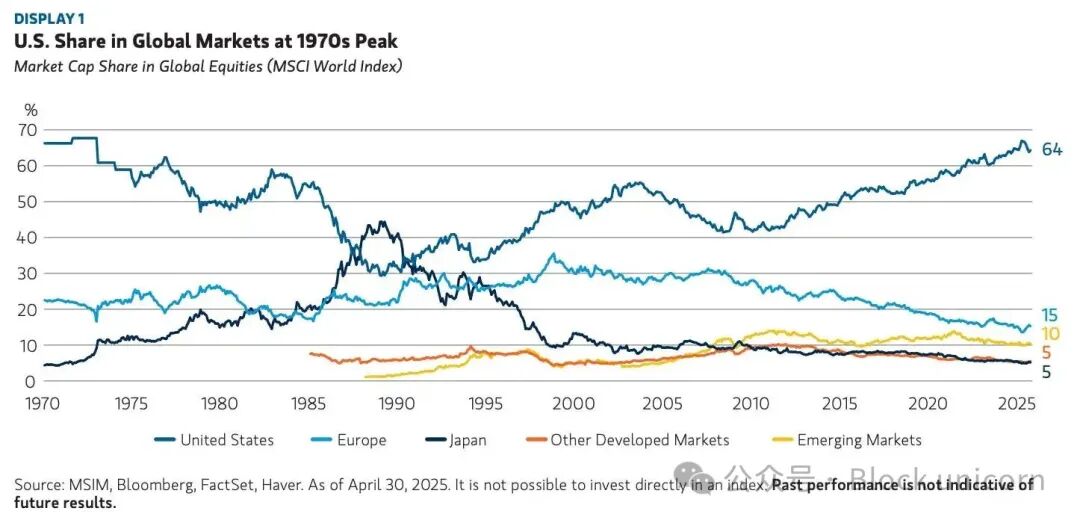

U.S. stocks account for over 60% of the global stock market value. For most investors in the world, buying U.S. stocks requires going through intermediaries, exchanging currencies, and meeting minimum account balance requirements, with account types also being restricted.

Everyone wants a piece of the pie and to be part of the growth story of the world’s largest economy. This explains why almost all cryptocurrency exchanges wish to allow traders to buy and sell U.S. stocks or derivatives based on U.S. stocks.

On June 1, Binance announced the launch of commission-free trading for 7,000 U.S.-listed stocks for its 300 million registered users, offering fractional shares starting from $5. The vast majority of users reside outside the United States and can now invest in U.S. stocks through their stablecoin wallets.

Kraken's xStocks has demonstrated how tokenization impacts investors' access to public stocks. The platform has tokenized over 100 publicly traded stocks, with a trading volume of $25 billion and 80,000 on-chain holders.

Blockchain can also unlock a pre-IPO price discovery mechanism. SpaceX is preparing for the largest IPO ever, expected to raise about $75 billion. On June 1, Anthropic secretly submitted IPO application documents. OpenAI may follow closely. Before these companies go public, the price discovery process has been opaque and limited to qualified investors only.

In the book "Pricing Private Assets," I explain how markets price assets that behave like publicly traded companies.

Companies like OpenAI and Anthropic have brand recognition, scalable revenues, and hundreds of millions of users. They possess everything a public company has, except for public shareholders. Their marketing strategies ensure that everyone has their own opinion about them. In fact, SpaceX's success rate is unprecedented, and almost everyone has their view on it, yet very few can truly assess its value.

Blockchain provides various tools that allow the market to price these private companies.

For example, many platforms that were initially cryptocurrency exchanges now offer pre-IPO perpetual contracts, prediction market contracts, and tokenized IPO access for companies yet to be listed.

Several market makers provide perpetual contracts for companies like SpaceX, Cerebra, and Anthropic on the Hyperliquid platform. Over the past six months, trading volume for these contracts has increased by about 300 times, from $16 million to $4.7 billion. In May, the total trading volume for these IPO pre-stock perpetual contracts, HIP-3, was 7.7%, while this ratio was only 0.2% in December 2025.

These trading venues are not only always open and cheaper, but they also provide ample liquidity that traders can trust.

During the escalation of tensions in Iran, Hyperliquid's WTI crude oil futures contracts had an average daily trading volume of hundreds of millions of dollars, with very small spreads. Between January and April 2026, the open interest for WTI crude oil futures contracts surged from $1.8 million to $560 million.

Traditional exchanges can also leverage user deposits to offer cross-margin trading and deep liquidity. Binance, through its integration with PreStocks, allows users to participate in pre-IPO stock trading; while Payward (the parent company of Kraken) allows users to invest in tokenized IPOs.

Less than 24 hours ago, Coinbase also joined Kraken and Binance in launching malicious contracts for pre-IPO stocks, with the first stock being SpaceX.

Building a Full-Stack Financial Technology

The two-way integration of traditional finance and cryptocurrency is creating a full-stack financial technology platform for numerous companies. On one hand, cryptocurrency-native platforms are expanding traditional asset categories; on the other hand, traditional exchanges are quickly adopting blockchain infrastructure.

In the cryptocurrency space, Kraken has spent over $2.7 billion on acquisitions in the past 12 months, transforming into a multi-asset brokerage. In March 2025, the company acquired injaTrader for $1.5 billion, the largest acquisition of a futures commission merchant registered with the U.S. Commodity Futures Trading Commission (CFTC) to date.

Subsequently, the company acquired Backed Finance, achieving self-control over the issuance, trading, and settlement of xStocks. By early 2026, its product range grew from 60 tokenized stocks to 100. After that, the company made five acquisitions in the fields of payment, clearing, and automated trading infrastructure.

Eventually, the company launched Krak, a payment application supporting over 300 assets in 160 countries, helping users spend, send, and earn profits using cryptocurrency.

Coinbase has also launched a similar product portfolio.

At a product launch in December 2025, Coinbase introduced commission-free stock trading covering all 50 states and launched a prediction market through Kalshi.

In August 2025, Coinbase acquired Deribit for $2.9 billion, gaining control of the world’s largest cryptocurrency options market. Today, Coinbase is positioning USDC and its Layer-2 chain Base as a settlement platform for various trades, from agency payments to stock trading.

These platforms have entered the financial sector through cryptocurrency and now possess distribution networks that traditional financial giants have spent decades building. Binance boasts 300 million registered users, while Kraken serves 15 million customers spread across 190 countries. Such a massive user base is their greatest moat in expanding multi-asset brokerage services.

When Binance launched 7,000 U.S. stocks, it did not need to build demand from scratch. The purchasing channels for these stocks and pre-IPO stocks are open to users who have already recharged stablecoins multiple times and completed identity verification. For an existing cryptocurrency brokerage, the marginal cost of adding stock trading is far lower than the cost for traditional brokers to acquire a new client.

Traditional firms are also actively adjusting themselves to stay competitive.

On the same day Binance launched U.S. stock trading, the Chicago Mercantile Exchange Group, the world's largest derivatives exchange, announced that all of its cryptocurrency futures and options would be traded 24/7.

Managing $114 trillion in assets, DTCC will trial tokenized securities in July this year and will fully operate in October. This pilot will cover Russell 1000 index components, major index ETFs, and U.S. Treasuries. More than 50 companies, including BlackRock, JPMorgan, and Circle, are participating in the project.

The New York Stock Exchange has partnered with Securitize to build a round-the-clock tokenized stock trading platform. Nasdaq received approval from the U.S. Securities and Exchange Commission in March to trade tokenized stocks within its existing trading system.

This is an interesting phenomenon of convergence. The Chicago Mercantile Exchange (CME) and other traditional financial institutions are implementing 24/7 operations because cryptocurrencies have proven that markets do not need to close. Cryptocurrency exchanges are also beginning to offer traditional assets—oil, silver, indices—because users have shown that any platform capable of providing ample liquidity and lower-cost information pricing methods will attract their demand.

Blockchain is becoming a bridge between the two.

Cryptocurrency as an Evolution of Financial Technology

Like any other technology, there exists an either-or perspective on the application prospects of cryptocurrencies in online forums. They believe cryptocurrencies will either build a brand new, independent financial system or collapse due to their own development. But in reality, the development of cryptocurrencies is somewhere in between. The history of the internet's evolution is similar.

When people were still ambivalent about the internet or viewed it as the dawn of a new world, the internet gradually commodified and eventually became ubiquitous, with almost the entire world relying on it to operate. Today, there is no longer a debate about the utility of the internet; it has become a common foundation supporting various emerging technologies.

This is precisely the change I believe is occurring in the cryptocurrency space. The technology related to cryptocurrencies may not have achieved the initial expectations of the cypherpunks. I suspect most of them do not even care; at least, I do not care.

While the internal market busies itself discussing Bitcoin cycles and downward trends, a parallel external market is steadily expanding across multiple levels of the financial system. Payment infrastructures, agency commerce, integrated price discovery platforms, and today’s multi-asset brokerage business are thriving, regardless of whether the Bitcoin price is $60,000 or $100,000.

Charlie Booth of Hepworth Iron Capital provided an excellent explanation of the evolution of endogenous-exogenous markets in a guest commentary published last week in Token Dispatch.

What interests me the most is that a technology originally used for trading tokens is now being employed to allow retail investors to acquire $5 worth of Apple stock on Saturdays, settled in stablecoins, with transaction fees under 1 cent, and all built upon infrastructures originally designed for meme coins.

These possibilities arise only when the new infrastructure far surpasses the outdated infrastructure it replaces. We all know that old habits are hard to change. Meanwhile, the world is discovering that blockchain is a panacea for improving financial operations. In some cases, blockchain functions by lubricating the traditional financial system; in others, it serves by completely displacing outdated systems. Changing for the sake of change is not a wise move.

For any human-operated industry, resisting transformative changes that could improve existing system operations is tantamount to suicide. This is because humans inherently crave improvements to inefficient systems. Anything that enhances system efficiency will be adopted, regardless of how novel or radical it may seem. The evolution of blockchain technology is in a realm with significant room for enhancement, able to effectively reduce such inefficiencies. Traditional institutions and markets like Nasdaq, the New York Stock Exchange, and the Chicago Mercantile Exchange are adopting blockchain technology, clearly indicating its growing importance in the future of finance.

Now every exchange is a broker (or will soon become one). Not all exchanges anticipated this, but this is precisely what they aspire to become. What will happen next? When every platform offers stocks, derivatives, prediction markets, and cryptocurrencies in the same application, who will be the ultimate winner? The key lies in how they integrate these assets into their respective platforms, allowing users to perform some of the most basic operations in finance: spend, transfer, receive, and profit.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。