The YBS market is shifting from synthetic yields to RWA real assets.

Written by: Tiger Research

Translated by: AididiaoJP, Foresight News

The decline in the supply share of Ethena’s sUSDe is not a signal of protocol failure, but rather a reflection of structural changes in the market. This article will explore the ongoing changes in the DeFi landscape.

Key Points

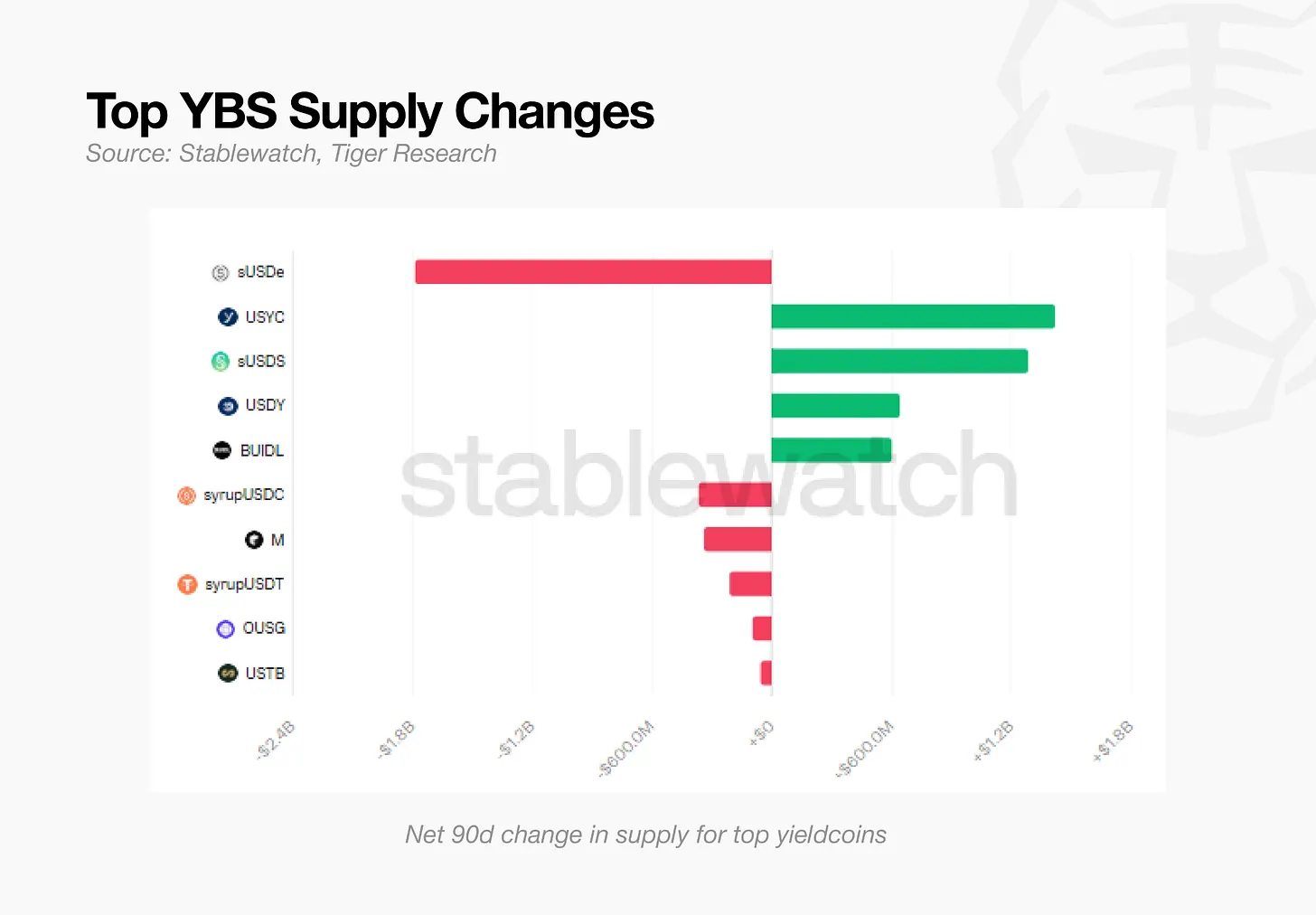

- The supply of sUSDe has halved, while funds have flowed into USYC and sUSDS, both offering lower yields. This is not a capital flight from the market, but a change in the criteria for selection within the market.

- APY is no longer the sole criterion for differentiating assets. More important is whether they can serve as collateral, savings products, or reserve assets.

- S&P has granted its first credit rating to the Sky protocol, marking the first time a DeFi protocol has received a credit rating in history.

- Ethena underwent a comprehensive reform of its collateral structure in April 2026, shifting from a purely synthetic model to a hybrid model. In the YBS market, a single source of yield is no longer sufficient to maintain competitiveness.

- DeFi is transitioning from a market that generates yields to one that imports and distributes yields from traditional finance. The stronger the foundation, the stronger the structure built upon it.

Reasons Behind the Decline of sUSDe

Yield-bearing stablecoins (YBS) are tokens pegged to the dollar that accumulate interest simply by being held. USDC and USDT operate like cash, while YBS operates like a deposit, with its value increasing as interest rates rise.

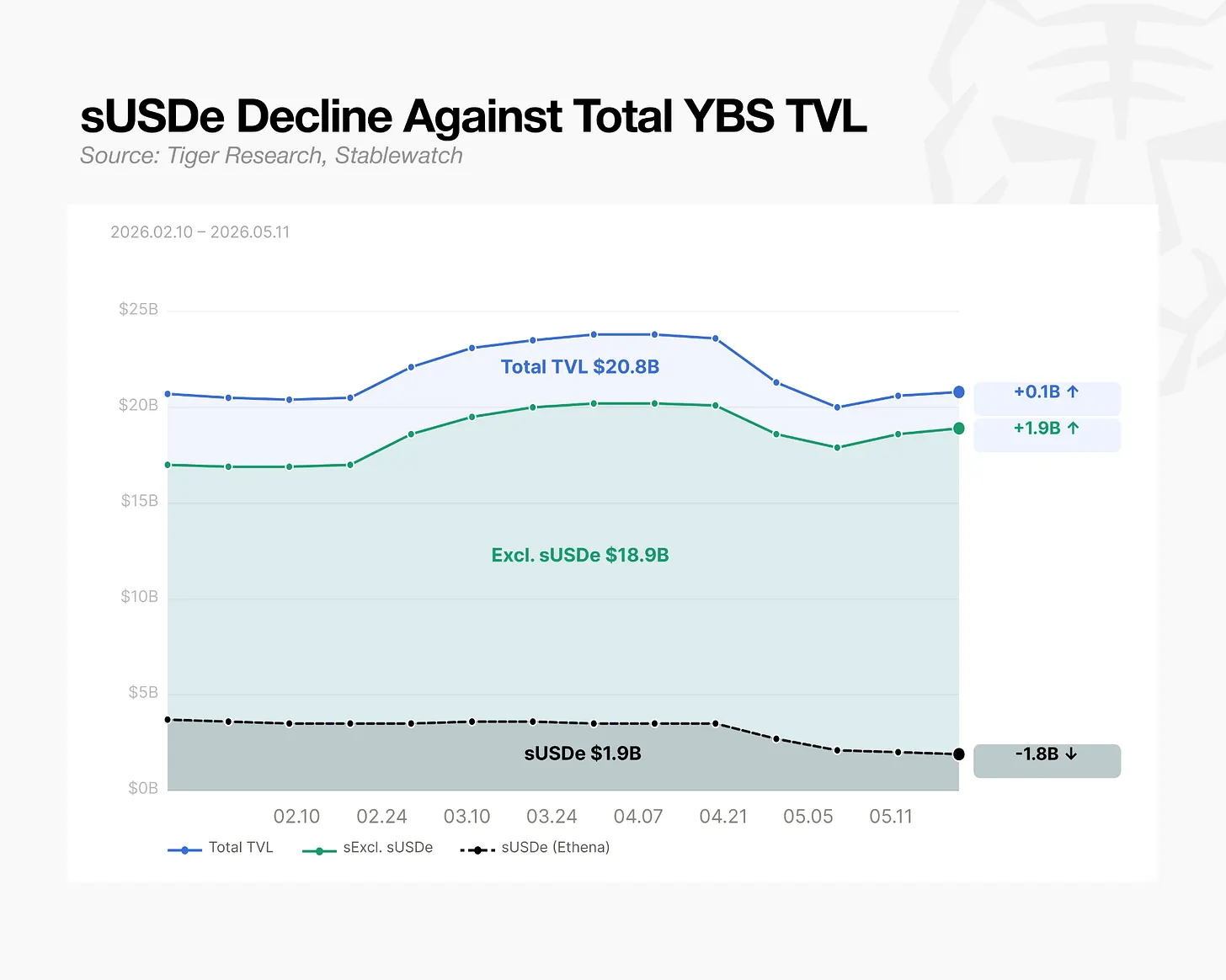

Something unusual is happening in this market. Ethena’s flagship product sUSDe once held over 30% of the YBS market share, but in the past 90 days, its supply has decreased by approximately $1.8 billion, a decline of roughly 49% from its peak. There have been no hacking incidents or protocol issues.

The market itself has not contracted. During this period, the total TVL of YBS has actually been rising. In 90 days, USYC (Circle’s treasury-backed stablecoin) received $1.4 billion, and sUSDS (Sky’s mixed stablecoin) saw $1.2 billion inflow. The combined inflows exceeded the decline of sUSDe.

The movement of funds tells a different story. Capital has not left; it has rotated within the same market.

More Important than APY are the Holder Base and Underlying Assets

Based purely on APY, there is no reason for capital to flow out. Over a 30-day basis, USYC is around 3%, sUSDS is about 3.6%. sUSDe is actually higher, around 4%. If yield were the driving factor, capital should be concentrated in sUSDe. This shift does not seem to stem from yields but rather from two other factors:

(1) Holder Base

(2) Underlying Assets

Retail vs. Institutional

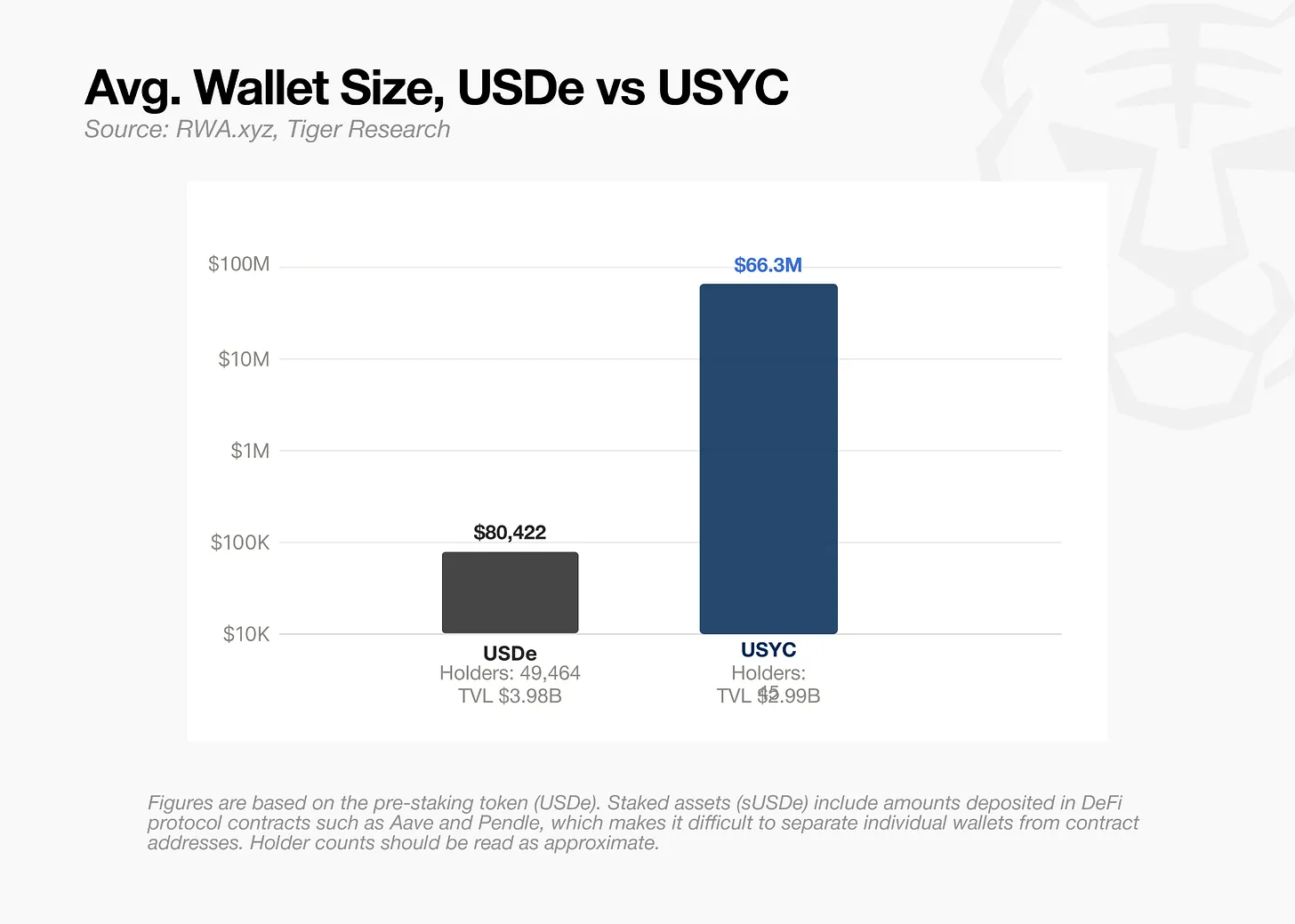

On average, the holding size per wallet for USDe is about 1/800 that of USYC holders. This gap widens further when large bulk purchases are excluded. USYC was designed from the outset to attract only large capital, while USDe heavily relies on retail users.

The differences in the holder bases of USDe and USYC are significant.

For USDe, both retail and institutional holders make investment decisions based around yield. They enter because of APY and exit when yields decline. USYC, however, adopts a different strategy. It lacks retail characteristics, with a core focus on institutional utility.

USYC is open only to accredited investors, with a minimum purchase amount of $100,000. In July 2025, Binance listed it as collateral for institutional derivatives. Once traders can use yield-bearing assets as collateral on the largest exchange, demand arises. A total of $2.54 billion has been issued on the BNB Chain alone.

Delta-Neutral vs. RWA

The differences between USDe and USDS stem from their reserve assets. Institutions seek predictability, including how yields are generated and how they fluctuate.

USDe employs a delta-neutral structure. One side consists of crypto collateral, and the other side is short perpetual contracts to hedge price fluctuations. Yields are tied to the perpetual funding rate. During the bullish market of 2024, sUSDe APY exceeded 47%. As the market shifted to a sideways trend, it gradually fell to the 3% range. In just a few months, the fluctuations surpassed tenfold. Yields fluctuate in tandem with market conditions.

USDS is backed by short-term U.S. Treasury bills and money market funds. Yields are linked to real-world interest rates. By the end of 2024, APY was in the 9% range and took over a year to drop to the 3% range.

This difference is also reflected in S&P's assessment. In August 2025, S&P Global granted a B- credit rating to the Sky protocol, marking the first time a DeFi protocol has received a credit rating. The rating itself is not high, but importantly, a DeFi protocol obtained a credit rating.

For institutions, predictability is as important as yield. sUSDe may offer higher returns based on market conditions, but institutional trading desks may find it more difficult to underwrite.

Direction of the YBS Market

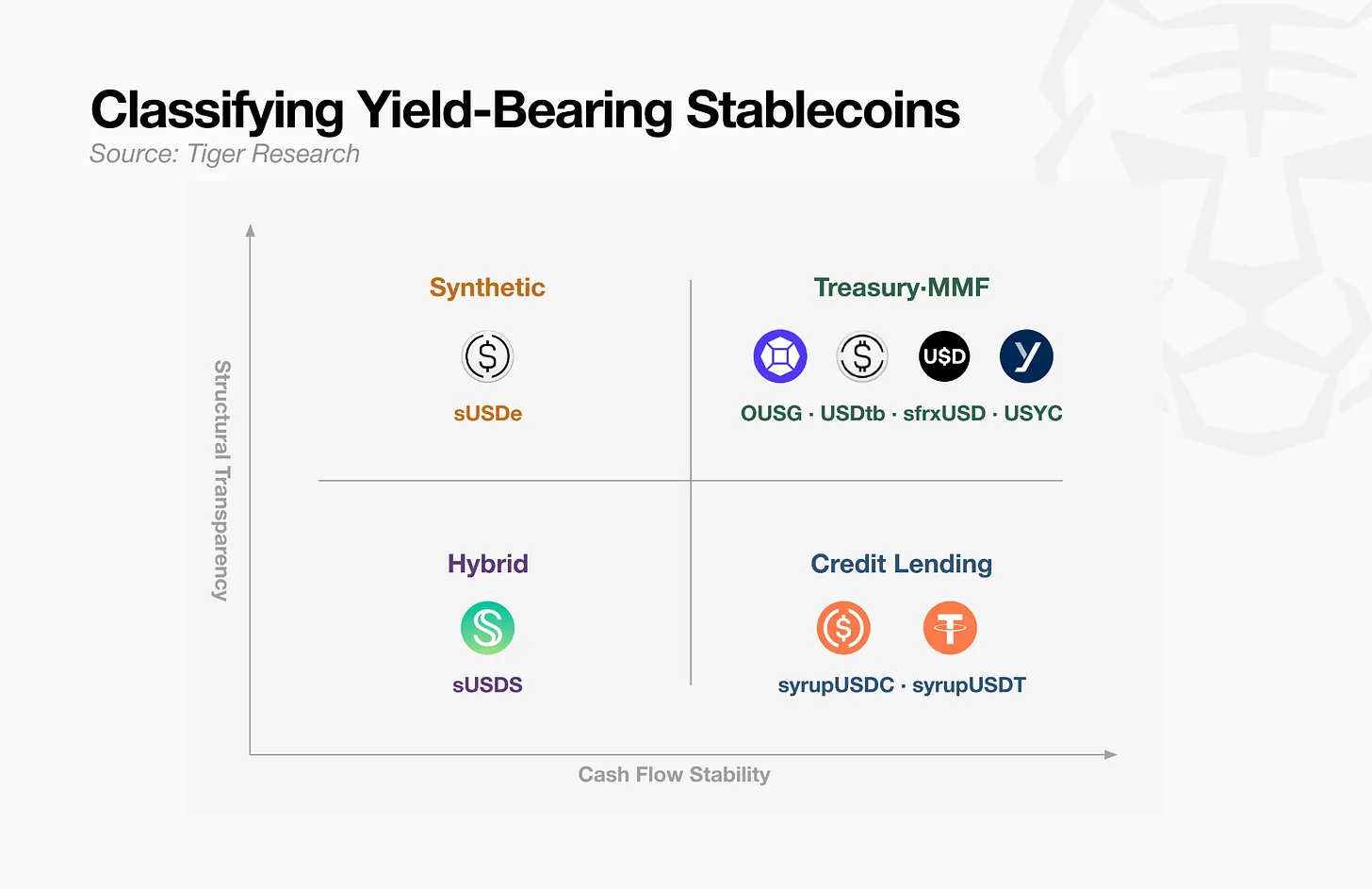

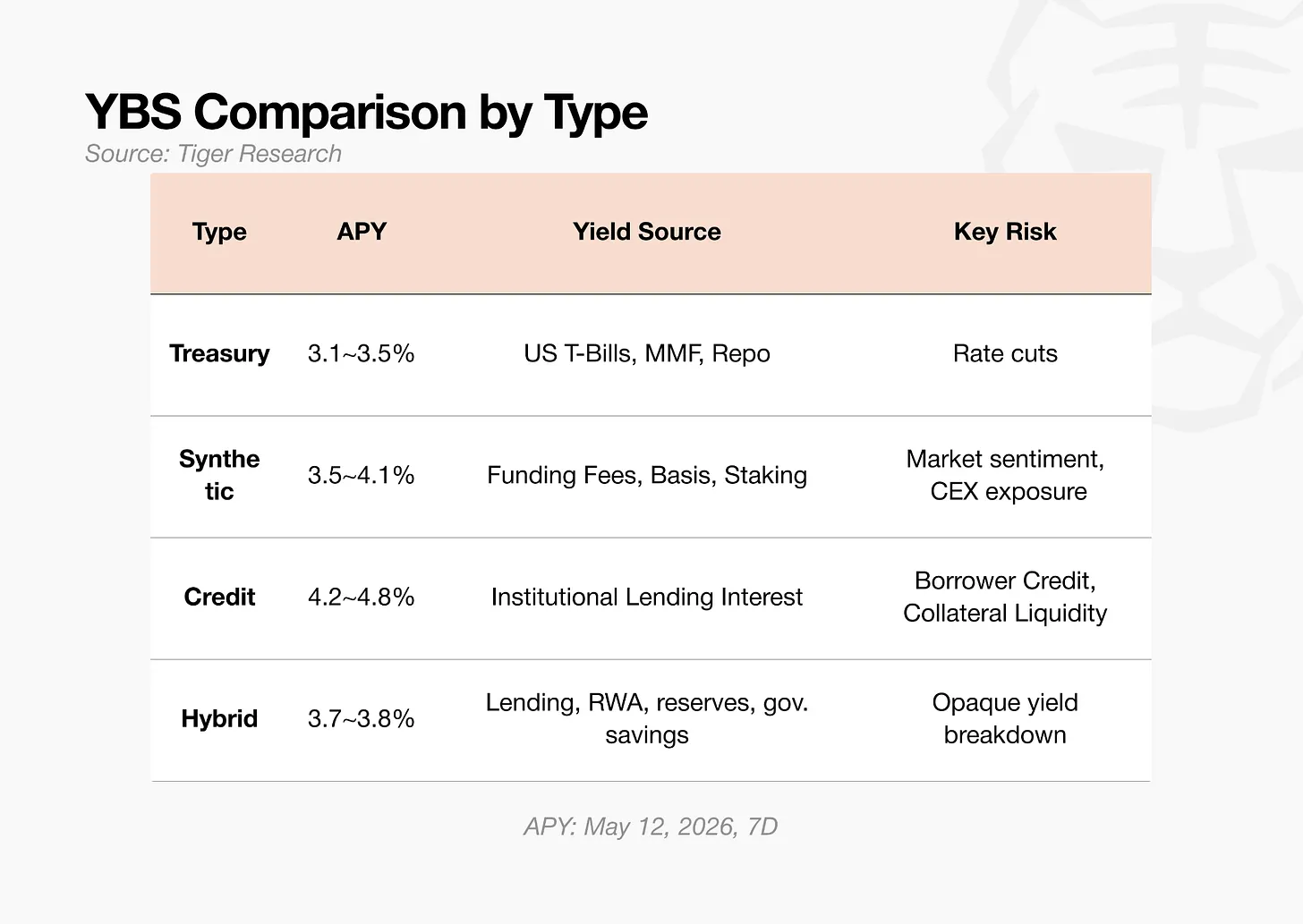

YBS assets can be classified along two axes: "how stable is the yield" and "is the source of yield verifiable." A 4% APY is not always the same 4%. The type of risk depends on who is paying the interest. Most capital is moving toward the more predictable side.

Government bond-backed YBS (OUSG, sfrxUSD, USYC) are the easiest to describe.

Short-term Treasury yield flows to holders through the operational layer from the issuer. As of May 2026, the average APY is between 3.1% and 3.5%. Its limitation is that yields are linked to Treasury rates.

Synthetic YBS (sUSDe) offers a transparent source of yield but is sensitive to market conditions.

The primary income source is perpetual contract funding rates. Yields can be verified on-chain but fluctuate dramatically with market conditions. In September 2025, APY exceeded 15%, but as of May 12, 2026, the 7-day APY is in the 4% range.

Credit-based YBS (syrupUSDC, syrupUSDT) has high yield stability but low verifiability.

Through Maple Finance, interest payments from hedge funds and trading firms flow back to holders. A fixed-rate structure in the 4% range maintains low volatility. However, borrower credit and collateral value are difficult to verify externally.

Mixed YBS (sUSDS) lies between the two extremes.

Its yield combines Spark lending fees, RWA returns, reserve management, and a saving rate set by governance. The 7-day rate is 3.6%, lower than sUSDe. In terms of risk, the absence of a single point of failure helps diversify risk. The trade-off is that the yield structure is difficult to decompose from the outside.

This classification points to a singular model. Excluding Ethena's synthetic model, each category is introducing the sources of yield from traditional finance onto the blockchain.

Ethena’s Layout

Ethena recognized the first signal of its structural limitations with the launch of USDtb. USDtb is a Treasury-backed dollar, using short-term U.S. Treasury bills as reserves. It aims to provide a buffer for USDe during periods when funding rates become negative.

In April 2026, Ethena took it a step further. It completely reformed the collateral structure of USDe. Ethena reduced the proportion of perpetual contracts to 11% of total collateral and introduced new categories: stablecoin reserves, DeFi lending, CLOs, investment-grade corporate bond funds, and short-term credit.

Ethena is also exploring the inclusion of a gold-based perpetual delta-neutral strategy in USDe collateral. This structure will apply the same methods used for BTC and ETH to gold (PAXG, XAUT). The risk committee has completed the formal review.

This is the largest structural change since its launch. In fact, Ethena acknowledges that a delta-neutral strategy based solely on crypto assets is no longer sufficient to sustain itself.

USDe and sUSDe began with a synthetic model but are evolving into a hybrid model. This transition confirms that a single source of yield is no longer adequate to remain competitive in the YBS market.

Foundation First

The idea that DeFi imports yield from traditional finance rather than generating yield natively may contradict the philosophy of decentralized finance. However, this does not mean that DeFi is at an end.

Blockchain was designed to build a decentralized internet but ultimately operates on top of the internet. Without the internet, there is no blockchain. Stablecoins aim to replace the dollar but ultimately operate on top of the dollar, which subsequently drove the rise of DeFi. Traditional underlying foundations have never blocked the innovation that occurs above them.

YBS can also follow the same path. BUIDL has become collateral for USDtb. USDtb has in turn become the reserve for MegaETH's native stablecoin USDm. New monetary legos have stacked on top of Treasury-backed YBS.

As Treasury-backed YBS becomes infrastructure, yields will compress, and the range of underlying assets will narrow. The alpha of any single asset will continue to diminish. Just as the internet became infrastructure and brought access costs close to zero, YBS will follow the same path. Stability and composability will outweigh yield in importance.

As infrastructure matures, the experiments built upon it can operate on a firmer foundation. The early synthetic dollar was unsustainable due to the instability of its underlying assets.

Early DeFi yield structures were built on sand. They relied on the prices of altcoins, token incentives, and leverage demand. Now, verified sources of yield are forming a foundation upon which on-chain financial structures are being built.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。